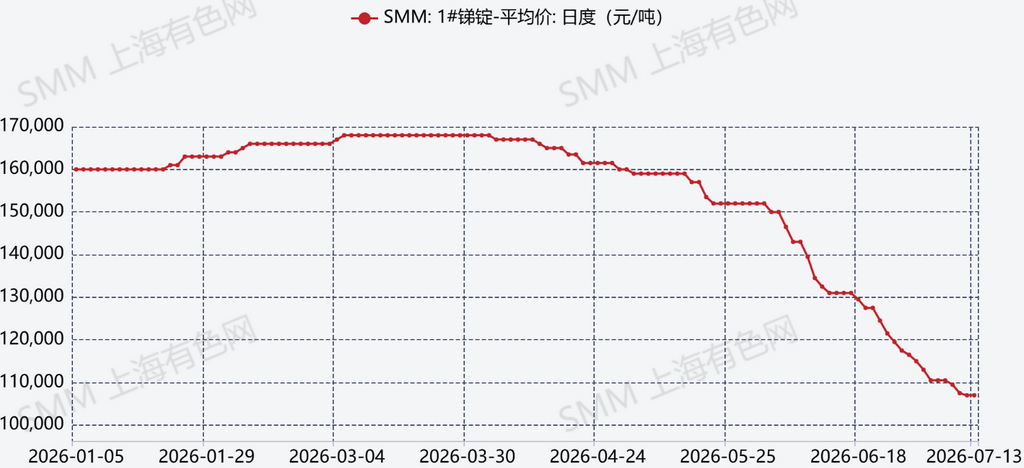

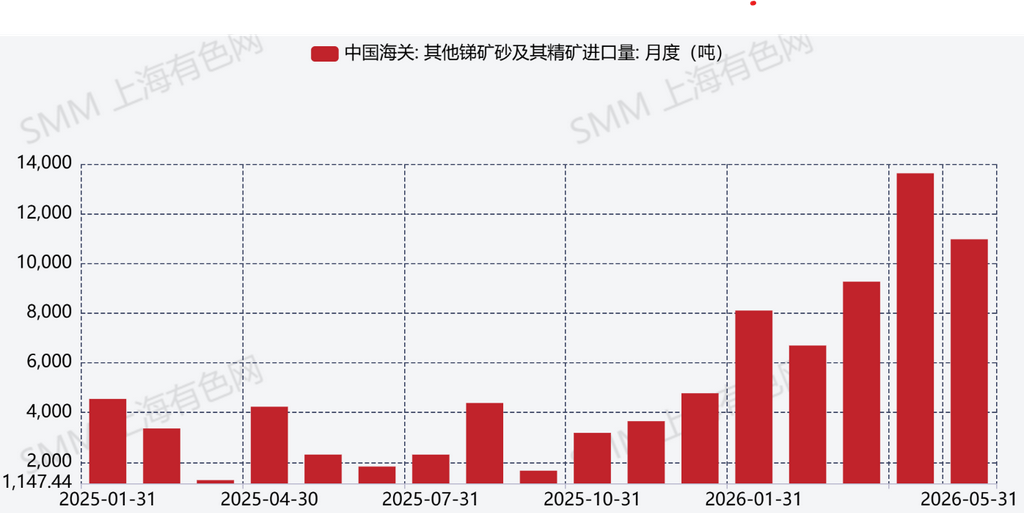

In the first half of 2026, the antimony market exhibited a persistently weak and significantly bearish trend, characterized by sharp price declines. During this period, cumulative production from January to June registered a slight year-on-year decrease of approximately 8%. However, massive imports of antimony ores and concentrates—totaling roughly 48,658 metric tons from January to May, a staggering 209% year-on-year increase—are expected to gradually convert into domestic supply. This influx is likely to amplify the potential for increased domestic production in the coming months. As of now, the spot price for domestic 1# antimony ingot averages approximately CNY 110,000/ton, representing a steep drop of about CNY 50,000/ton from the beginning of the year.

From the supply side, despite limited changes in overall production, the industry operating rate has not shifted significantly. Some enterprises facing tight antimony resources continue to maintain low operating rates or remain in shutdown. Over the past six months, with prices consistently trending downward, the risk of buying high-priced raw materials while selling products at low prices has further dampened these producers' willingness to procure antimony materials, making any meaningful recovery in operating rates increasingly difficult.

On the demand side, downstream sectors—particularly the flame-retardant industry and photovoltaic glass manufacturing—show persistently subdued stocking interest, with buyers remaining generally reluctant to purchase. This weakness stems primarily from two factors: (i) reduced order volumes due to sluggish conditions within these industries, and (ii)—more critically—the prevailing bearish price outlook, under which end-users continue to purchase strictly on an as-needed basis, delaying stockpiling wherever possible. Meanwhile, previously active speculative participants have exhibited waning confidence, temporarily withdrawing from the market and adopting a wait-and-see stance.

Turning to imports and exports, the narrowing price differential between domestic and international markets has encouraged antimony ore imports to flow into China in pursuit of quicker monetization. Key source countries are concentrated in Southeast Asia, notably Myanmar and Thailand.

Looking ahead to the second half of the year, it is projected that annual production will surpass 80,000 metric tons, representing a year-on-year increase of over 5%. Should antimony prices manage to stabilize, rebound, and recover in the latter half of the year, the average annual price is expected to be approximately CNY 140,000/ton.

Key factors to monitor include:

-

Fluctuations in antimony ore import volumes;

-

Downstream demand dynamics;

-

Potential policy shifts in export regulations that may exert market impacts.

Additionally, if prices stabilize and recover—given that current levels are nearing the three-year low—close attention should be paid to speculative stocking purchases, as such buying behavior could further influence antimony market pricing.

![Antimony Prices Continue Downward Trend [SMM Antimony Spot Market Weekly Review]](https://imgqn.smm.cn/usercenter/TdoSs20251217171724.jpeg)