SMM, July 10:

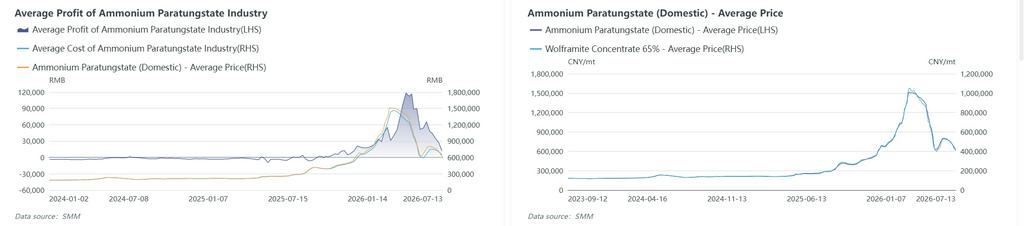

In H1 2026, the tungsten market was largely driven by supply logic, going through a complete cycle of sharp rises and falls and eventually retreating from highs to close out the half-year. In Q1, on expectations of multiple supply tightening factors such as continuous reductions in domestic tungsten ore mining output, tighter export controls on dual-use items, and the upgraded status of tungsten as a strategic mineral, market sentiment was strongly inclined to hold back from selling, with funds flowing in to push up tungsten prices. 65% wolframite concentrates surged past 1 million yuan/standard tonne to hit a record high, the entire upstream and downstream industry chain rose in tandem, and industry profitability surged substantially during the period. In Q2, the extreme high prices quickly exhausted downstream affordability, becoming the key trigger for the market reversal. Traditional manufacturing downstream sectors such as cemented carbide, cutting tools, and molds faced cash flow difficulties, end-users were unable to smoothly pass on costs, small and medium-sized enterprises proactively lowered operating rates and consumed their own inventories, and spot procurement of raw materials shrank significantly. Meanwhile, speculative funds locked in profits and exited en masse, market liquidity cooled rapidly, and tungsten concentrates nearly halved from their peak and entered a continuous pullback. In June, with the supply-demand imbalance easing somewhat, downstream cemented carbide users entered the market for rational restocking, and trading volumes improved. However, overall demand growth was limited, and the market still lacked upward momentum in June. Overall, the price center of the tungsten market in H1 2026 moved significantly higher compared to the same period of 2025, with large price swings. Taking national standard first-grade tungsten ore as an example, as of end-June, SMM 65% wolframite concentrates closed at 501,000 yuan/standard tonne, up 10.5% from the start of the year. The year's high was recorded at 1.05 million yuan/standard tonne, the H1 average price was 688,300 yuan/standard tonne, up 356% YoY, and the overall H1 price amplitude reached approximately 162%.

Looking at the half-year in stages, it can be simply divided into three phases:

Phase 1 (early January–mid-March): Strong surge to a peak. Tight ore supply, surging overseas tungsten prices (European APT price surged 85%), and tungsten's designation as a critical mineral triggering a strategic premium, coupled with restocking for downstream rigid demand, accelerated the market rally. Tungsten concentrates climbed from around 450,000 yuan/standard tonne all the way to 1.05 million yuan/standard tonne in mid-March, a gain of over 130%.

Phase 2 (mid-March–late May): Deep correction. Concentrated release of high-level profit-taking positions, stampede-like flight of speculative inventories, a surge in scrap tungsten supply creating a substitution impact, a 172.5% YoY jump in imported tungsten concentrates to fill the ore supply deficit, continued tightening of export controls, and the end-user "alloy reduction" trend compressing consumption. Scheelite concentrates fell about 62% from their high to 400,000 yuan/standard tonne, and APT dropped from over 1.5 million yuan/mt to around 630,000 yuan/mt.

Phase 3 (Month-end May to Early July): Oversold rebound followed by renewed pressure. After the oversold phase, downstream restocking demand was released, driving a brief market rebound to 526,500 yuan/standard tonne. However, from mid-June, multiple mines launched competitive sales, increasing circulating cargo supply. Coupled with the approaching off-season in July, prices pulled back again to around 436,500 yuan/standard tonne.

In H1 2026, tungsten concentrates supply featured rigid policy-driven reductions, tightened spot circulation, a complete absence of growth, and frequent disruptions, serving as the core fundamental driver of this year’s super bull market since the beginning of the year. The full-year tight supply balance was fully validated in H1.

First, for the tungsten supply side: Rising imported ore and recycling utilization rates offset the reduction in primary ore.

Primary ore production fell significantly YoY: In H1, China’s main tungsten concentrates producing regions persistently cracked down on illegal mining activities such as unauthorized mining, excessive extraction, and grey-market output. The operational space for small and medium-sized compliant mines continued to shrink. Combined with routine inspections by local safety supervision and environmental protection authorities, effective mining days were reduced, limiting production growth. Regarding new capacity, a tungsten ore enterprise in Shaanxi completed construction and commenced production in H1, but incremental provincial quotas were limited, so the actual growth contributed by this enterprise was minimal. In H1, China’s tungsten ore mining industry strictly enforced quota controls, with quotas valid only for the current year, without additional approvals or carryovers. This rigid control mechanism locked out any growth in primary tungsten ore at the policy source. Based on SMM sample data, China’s tungsten concentrates production in H1 2026 fell by around 10.5% YoY, mainly because the previous year’s supply still included a certain degree of excessive extraction and grey-market output.

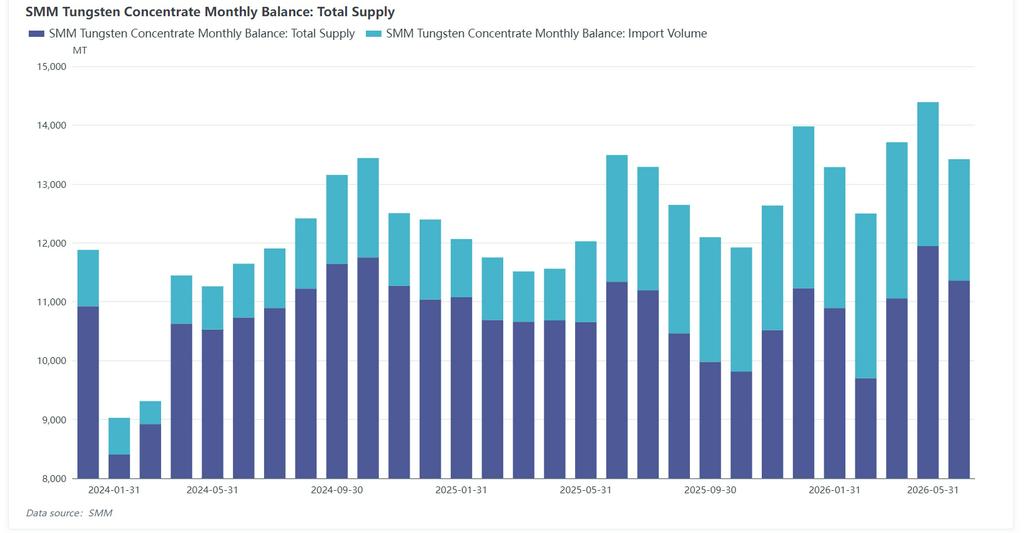

On the import supplement side: China’s tungsten concentrates imports maintained YoY growth in H1 2026, mainly due to stable supply from Kazakhstan’s tungsten mine in H1 and stable import channels from Myanmar and North Korea. According to customs data, China’s tungsten concentrates imports rose 140% YoY to 12,300 mt in January-May 2026, mainly from Kazakhstan, Myanmar, North Korea, and Mongolia. Kazakhstan emerged as the largest supplier, with imports of about 4,295 mt, accounting for 36%; in Q1 2025, this mine had not yet commenced production, so imports were zero. For the full year 2025, imports from Kazakhstan totaled about 6,899 mt, representing 33%. Imports in 2026 are expected to reach around 15,000 mt. The increase in imports partially offset the reduction in domestic tungsten concentrates.

Scrap tungsten supplement: In H1, China’s scrap tungsten market consolidated wildly. In Q1, supported by capital interest in the tungsten market, the scrap tungsten recycling industry—benefiting from advantages such as low entry barriers—was favoured by some capital. A large number of traders entered the market to recycle and trade scrap tungsten, leading to the rapid accumulation of scrap tungsten inventories. In terms of cost-effectiveness, primary tungsten market rose rapidly in Q1, making downstream restocking difficult. Some downstream smelters increased their use of scrap tungsten. Zinc-melt materials and electrolytic carbonised tungsten powder directly produced from scrap tungsten gained favour in the low and mid-end cemented carbide industry chain, resulting in a notable increase in industrial scrap usage. According to SMM estimates, China’s scrap tungsten usage in H1 was about 12,500 mt in metal content, accounting for roughly 29.6% of total tungsten supply in H1, with the industrial scrap usage ratio rising significantly. However, in Q2, due to policy adjustments such as sluggish reverse invoicing for recycled resources, the circulation of tax-exclusive scrap tungsten products was difficult, and the procurement proportion by smelters declined. With the advancement of the domestic "Three Flow Integration" policy in July, the circulation of scrap tungsten into the industry chain may gradually stabilize.

Next, downstream consumption: midstream profit recovery, traditional demand under pressure, and emerging growth providing a floor

In the midstream smelting segment, profit improved but production growth was limited: From the perspective of downstream consumption of tungsten concentrates, operating rates in China's APT and ferrotungsten industries were generally weak in H1. The significant rise in tungsten prices in H1 drove prices of midstream smelting products such as APT, tungsten powder, and ferrotungsten up, substantially recovering overall profitability. Processing profits of smelters increased significantly compared to the same period last year, with leading smelters seeing notable profit growth in Q1. However, constrained by multiple factors, the overall industry operating rate remained weak, and production growth was hard to release. On one hand, spot tungsten concentrates were persistently tight in H1, making raw material procurement difficult and causing wild cost swings. High-position stockpiling carried high risks, so most enterprises adopted a "produce based on demand, low inventory operation" model and did not blindly expand production. On the other hand, the surge in tungsten prices at the start of the year led to losses for downstream end-users and a sharp decline in procurement, pressuring midstream finished product inventories. Combined with the rapid retreat of tungsten prices in Q2, market sentiment on production and stockpiling was cautious. Overall, the midstream smelting segment presented a pattern of "improved profitability, restrained operating rates, and limited production," with profit recovery not translating into effective supply growth. According to SMM data, China's APT production in H1 fell 3% YoY. Coupled with the industry's scrap utilization ratio rising from 30% last year to around 32%, consumption of primary ore in the APT smelting industry in H1 showed a declining trend. According to SMM data, the operating rate of China's ferrotungsten industry in H1 2026 was generally on a downtrend, especially in May, when the operating rate fell to 10%, nearly halting production. As major ferrotungsten smelters in Jiangxi resumed production, the June operating rate rebounded to 28%, with monthly ferrotungsten output clearly recovering MoM. However, the overall H1 operating level was far below the same period in 2025, indicating a significant supply contraction for the industry.

Traditional cemented carbide substitution and alloy reduction coexist: As a traditional core scenario for tungsten consumption, the cemented carbide industry faced sustained demand pressure in H1, with the trends of de-alloying and material substitution becoming increasingly evident. During the period of high tungsten prices, downstream enterprises in cutting tools, molds, and mining machinery generally adopted reduced tungsten formulations to control costs, lowering the proportion of tungsten materials while maintaining basic product performance. At the same time, substitute materials such as ceramic tools, coated hard materials, and new-type alloys accelerated their application, continuously substituting for low- and mid-end tungsten-based alloy products. Compounding the sluggish manufacturing recovery and insufficient end-user orders in H1, traditional cemented carbide enterprises continued to operate at low rates, with weak willingness to actively restock raw materials, further squeezing traditional demand for tungsten. This became the core bearish factor capping tungsten prices in H1 and dragging the market into a pullback.

Emerging sectors boosted market confidence, but sustainability needs verification: The PCB micro-drill and semiconductor tungsten hexafluoride sectors achieved structural high growth, effectively easing pressure from weak traditional demand and lifting industry confidence. However, both sectors face segmented cyclical and policy constraints. On closer analysis, the combined incremental tungsten consumption from these two sectors amounts to around 2,000 mt in metal content, insufficient to support the extreme highs in tungsten prices in H1. Overall demand absorption capacity remains limited. Going forward, attention should be paid to the actual expected growth in tungsten consumption driven by capacity expansion in these emerging sectors.

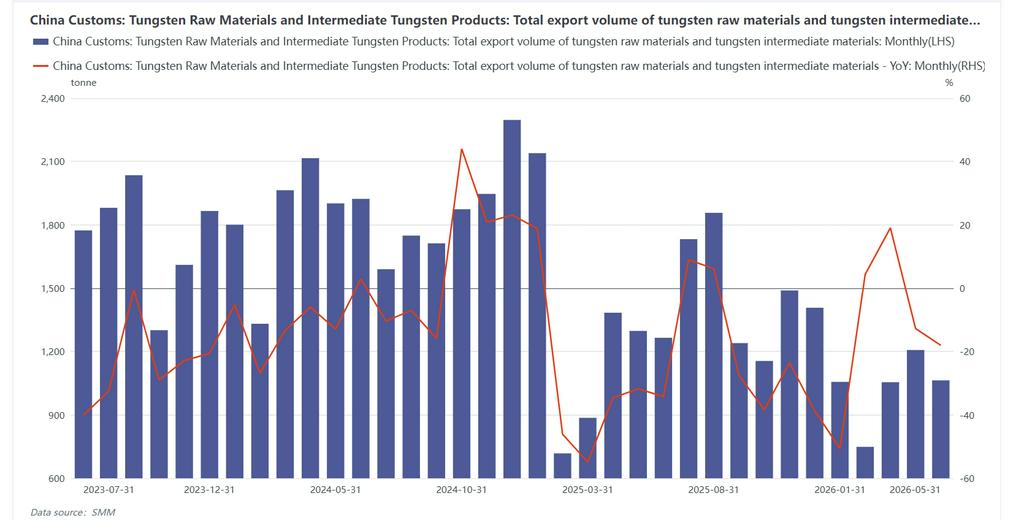

Export controls on tungsten materials and intermediate products are tight, with little room for increase: Since June 2026, the Ministry of Commerce has intensively introduced dual-use item control policies: adding 10 US military-industrial and rare earth enterprises to the embargo list; improving the reporting and supervision mechanism for violations involving strategic minerals such as tungsten, molybdenum, and rare earths; adding 40 Japanese defense-related entities in two tiers, implementing full embargo and strict case-by-case approval respectively; and simultaneously working with customs to tighten customs clearance inspections for precision machine tools, comprehensively strengthening export controls on strategic minerals and military equipment dual-use items to prevent illegal outflow of materials and technology. According to customs data, total exports of tungsten materials and intermediate products from China in January-May amounted to approximately 4,067 mt, down 13.5% YoY. Exports to Japan fell by about 65% YoY.

Overall, the core logic behind all upward price movements in H1 came from the supply side: a resonance of policy-driven production cuts, capacity disruptions, export tightening, and spot scarcity propelled tungsten concentrates past the historical 1-million mark. However, the supply side can only determine the upside elasticity of prices, not their sustainability. Once high prices completely decoupled from downstream demand affordability, passive contraction on the demand side directly ended the bull market, sending the market quickly into a pullback. Looking into H2, the trading logic of the tungsten market will undergo a fundamental shift: marginal supply-side changes will stabilize, no longer generating strong stimulus; instead, demand seasonality, end-user operating rates, and restocking pace will become the sole core variables determining price changes, the center of the trading range, and market sustainability.

Entering H2, annual tungsten ore mining quotas have been fully implemented, and monthly mine output is stabilizing. There is no room for further significant production cuts or additional volume releases in policy. The earlier production stoppage disruptions in the industry have been fully priced in by the market, with no new sudden supply contraction themes. Export controls and recycled tungsten supply remain steady. Marginal variables have largely disappeared. The supply side no longer has the capacity to drive sharp price surges; it will only provide strong support at low price levels through resource scarcity, mine holders holding back from selling, and monthly supply-demand mismatches in tungsten ore. The upward momentum for prices has completely shifted to the demand side. H2 market will be entirely driven by the demand cycle, with a clearly divergent rhythm: July-August is the traditional high-temperature off-season, manufacturing operating rates are low in summer, carbide end-users continue to digest H1 inventory, willingness to actively restock is weak, the market mainly sees small-volume rigid-demand deals, and weak demand will continue to cap tungsten price upside room; the overall market shows a consolidating pattern of “no demand, no market,” with price fluctuations completely following the downstream procurement pace. As the traditional manufacturing peak season enters September-December, machinery manufacturing, machine tools, cutting tools, and auto parts enter the annual stockpiling peak season, traditional rigid demand steadily recovers, PV wafer capacity expansion continues to materialize, the incremental demand for tungsten wire is concentrated in H2, annual defense procurement tasks are intensively delivered, the supply gap of high-purity tungsten products outside China continues to widen, and export orders for high-end tungsten materials steadily increase; the joint recovery of multiple demand forces will become the core driving force for tungsten price rebounds in H2. Meanwhile, after the sharp rises and falls in H1, risk appetite across the industry chain has significantly cooled, and downstream enterprises’ raw material procurement has become more rational and cautious; in H2, if tungsten prices rebound quickly and challenge highs again, end-users will again adopt strategies of reducing procurement and destocking, thus capping the extent of price rises. How high and for how long prices can rise entirely depends on the strength of demand uptake: if demand is strong, the rebound can sustain; if demand is weak, the rebound will quickly halt. The constraint weight of the demand side on the market reaches its peak for the year, the overall market officially moves away from the volatile pattern driven by supply expectations in H1, fully entering a pricing phase based on demand fundamentals.

From a comprehensive supply-demand fundamental perspective, SMM estimates that China’s primary tungsten concentrate supply in full-year 2026 will be down about 1.5% YoY, with the decline mainly narrowing in H2. Meanwhile, the tungsten trade structure for the year shows a clear trend of net import growth, coupled with a 30% YoY increase in scrap tungsten supply. China’s tungsten supply-demand balance shifts from tight supply in 2025 to a tight balance state in 2026. In H2, all strong stimulus variables on the supply side have already materialized, the margin tends to stabilize, and they no longer dominate market pricing; the core market logic fully tilts toward the demand side. However, as a strategic metal, tungsten’s supply scarcity will set the industry floor price. It is expected that tungsten concentrate prices in H2 will consolidate in the range of 300,000-600,000 yuan per standard tonne (65%WO3 basis). In terms of pace, the market will continue to consolidate on a weak note under the pressure of the demand off-season in July-August. From end-Q3 to Q4, as the supply temporarily tightens due to the gap in mining index transition, the “September-October peak season” drives restocking recovery, and the price spread between Chinese and overseas markets continues to catalyze export orders, multiple positives are expected to provide strong support for tungsten prices, and the market may stage a mild and orderly upward trend. The following risks still need to be guarded against: First, if raw material prices surge irrationally and sharply in the short term, it will continuously push up alloy production costs, squeeze profits of downstream product enterprises, and force end-users to cut production, creating negative feedback. Second, the risk of concentrated selling pressure in the scrap tungsten market still exists. Third, the impact of capacity expansion at mines outside China on the long-term supply landscape.