In H1 2026, the core contradiction in the LFP cathode material market went beyond simple supply-demand relationship shifts; it was a deep, top-down game of cost pressure transmission and the redistribution of interests across the industry chain.

The origin of this game was sulfur. As a key raw material for iron phosphate production, the persistently climbing sulfur price triggered a chain reaction. SMM price data showed the average price of iron phosphate rose from around 10,000 yuan/mt at year-end 2025 to 14,500 yuan/mt in June 2026, a surge of over 40%. Iron phosphate is the core component of LFP processing fees, and its price hike directly drove up cathode material production costs. However, the path of upward cost transmission was not smooth; most battery manufacturers were slow to accept price increases, leaving material makers stuck in the passive situation of “costs rise, selling prices barely move.”

This bind played out repeatedly during H1, becoming an almost universal operational challenge for LFP enterprises. The ability to withstand these cost shocks varied markedly, and the key lay in client structure. Companies with deep, binding relationships with top battery producers had stronger bargaining power and more room to maneuver when costs fluctuated. Client quality was becoming the core variable determining short-term profitability or loss.

A turnaround came from April to May, when some leading and mid-size battery cell manufacturers began accepting raw material price-linked settlement mechanisms, signing contracts that all used SMM’s monthly average iron phosphate price as the settlement benchmark. While this change has yet to cover the entire industry, it provided breathing room for some LFP enterprises with certain clients and opened a breakthrough for the eventual comprehensive adjustment of settlement models.

Beyond the cost game, the industry’s overall volume continued to expand rapidly. China’s total LFP cathode material production reached 2.629 million mt in H1, up approximately 67% YoY; outside China, total LFP cathode material production reached 28,000 mt, up roughly 2x YoY. Energy storage demand remained robust, the overseas EV market contributed growth, and China’s commercial vehicle segment performed steadily. The supply-demand gap for high-compaction materials persisted, with fourth-generation materials remaining in a relatively tight pattern and fifth-generation materials achieving small-batch supply. Overseas capacity emerged from scratch, process routes saw advances on some fronts and retreats on others, and the industry maintained its momentum of technological iteration and capacity expansion despite the pressure. This article will use “cost transmission and settlement games” as its main thread to systematically review price changes, the supply-demand pattern, product evolution, and competitive dynamics in the LFP market during H1 2026, and offer a judgment on the market’s direction in H2.

Supply side: Production and capacity

In H1 2026, total LFP cathode material production in China reached approximately 2.629 million mt, up approximately 67% YoY. In terms of monthly trend, except for a slight pullback in February due to the Chinese New Year factor, production increased month by month in the remaining months, with June production alone reaching 502,000 mt, a new record high. Outside China, total LFP cathode material production reached 28,000 mt, up approximately 2 times YoY. In terms of major project progress, the Indonesia base has entered mass production, with some cathode plants in Japan, South Korea, Europe, and America also in commissioning or small-batch production stages. However, cathode plants outside China still lag significantly behind Chinese enterprises in product maturity, cost control, and client validation, making it difficult to form a substantial replacement for China's LFP exports in the short term.

Capacity side, as of end-June, China's total LFP capacity had reached approximately 8 million mt/year, a significant increase from over 6 million mt at year-end 2025. New capacity is primarily concentrated in traditional dominant regions such as Yunnan, Guizhou, and Sichuan. Expansion by top-tier players has been relatively rational, with all reaching full capacity operation.It is expected that by year-end 2026, total industry capacity will reach approximately 11 million mt/year.It should be noted that the capacity statistics include a considerable proportion of "zombie capacity." This capacity cannot operate normally for long due to failing environmental standards, outdated production lines, and technological bottlenecks; actual effective capacity is far below nominal capacity. The challenge facing the industry is not total overcapacity, but the coexistence of insufficient effective high-end capacity and surplus low-efficiency conventional capacity. LFP cathode material production outside China made substantial progress in H1 2026.Outside China, capacity grew from 30,000 mt/year in 2025 to approximately 150,000 mt/year, concentration mainly in Indonesia. In terms of major project progress, the Indonesia base has entered mass production, with some cathode plants in Japan, South Korea, Europe, and America also in commissioning or small-batch production stages. However, cathode plants outside China still lag significantly behind Chinese enterprises in product maturity, cost control, and client validation, making it difficult to form a substantial replacement for China's LFP exports in the short term.

Demand side: End-use market divergence is evident

In H1 2026, China's total LFP battery cell production was approximately 1,031 GWh, up 77% YoY. Global total LFP battery cell production was approximately 1,052 GWh, with LFP battery cells outside China mainly concentrated in countries such as the US and Thailand. From the end-use sector, the growth drivers in H1 2026 came primarily from three areas: energy storage, commercial vehicles, and the overseas EV market.

The energy storage market was the largest source of growth. Power infrastructure-related energy storage demand driven by the expansion of AI computing power needs, intensive implementation of energy storage policies in overseas countries, and ongoing support for energy storage projects from various provinces and cities in China collectively boosted a significant rise in ESS battery cell production. Battery manufacturers also accelerated their layout in large-format battery cell products, with the switch from 314Ah to 587Ah, 588Ah, and even 600Ah+ further increasing cathode material demand per GWh and concurrently driving a marked increase in demand for high-compaction density materials.

The overseas EV market performed well. Unlike the Chinese market, where the NEV penetration rate is already at a high level and growth has slowed, the overseas NEV penetration rate remains low, offering substantial room for growth. Overseas auto sales gradually improved in H1, driving an increase in export demand for LFP power batteries.

Growth in China’s EV market was relatively mild. The domestic passenger vehicle market has entered a stock competition phase, with the penetration rate’s growth slope slowing, meaning power-sector cathode material growth is mainly driven by rising vehicle battery capacity. However, the commercial vehicle sector performed relatively well, with the fitment ratio of LFP in commercial vehicles continuing to rise, and the increase in their vehicle battery capacity further drove industry demand for high-compaction density cathodes.

Products and Technology: High-Compaction Density Remains Tight, Process Routes Shift

In terms of product structure, the divergence among product generations intensified further in H1 2026. Under common cost pressure, the premium commanded by high-compaction density materials over conventional products became more prominent.

Gen 2 and Gen 2.5 product production held a share of approximately 21% ; many producers exist in this space, making competition the most intense, and processing fees have fallen below the cash cost line for most enterprises, resulting in an overall loss-making state. Gen 3 products remained mainstream, with a production share of approximately 43% ; their market share edged down from H1 last year, and profitability was also not optimistic, with only a few enterprises with good cost control able to sustain marginal profits (e.g., integrated enterprises, or those adopting low-priced outsourced toll processing). Gen 3.5 products had a production share of about 21% ; the number of producers is limited, but their share rose significantly YoY. Processing fee levels were notably higher than for conventional products, enabling positive profits. Gen 4 products had a production share of roughly 15% ; although their share also jumped significantly YoY, supply-demand conditions were tight. The number of enterprises capable of stable, mass supply of Gen 4 products remained in the single digits; downstream battery cell manufacturers' rising demand for large cells and high energy density products saw Gen 4 materials' bargaining power steadily strengthen, giving them greater leverage in processing fee negotiations. For Gen 5 products, some enterprises achieved small-scale supply in H1, marking the continued upward movement of the technological ceiling for high-compaction density LFP, and shipments are expected to increase in H2.

Price: Lithium Carbonate Dominates Absolute Material Prices, Processing Fees Surge on Cost Push

Absolute material prices followed lithium carbonate trends:

In H1 2026, the absolute price of LFP cathode materials generally followed the fluctuations of lithium carbonate prices. The price of lithium carbonate at the start of the year was approximately 119,500 yuan/mt, closing at 156,500 yuan/mt at end-June, having peaked at 200,500 yuan/mt over the period, showing an overall rising trend. Affected by these factors, the average price of LFP materials showed a corresponding upward trend, with the price of LFP reaching a low of 45,000 yuan/mt and a high of 66,000 yuan/mt in H1.

Processing fees: notable increases driven by cost:

Unlike the absolute material prices which tracked lithium carbonate fluctuations, processing fees charted an independent upward course in H1, with the core driver being the rise in whole-chain raw material costs triggered by surging sulfur prices. Iron phosphate, the largest cost component in processing fees, saw its price rise from approximately 10,000 yuan/mt at end-2025 to 14,500 yuan/mt in June, a cumulative increase exceeding 40%. The persistent rise in sulfur prices was the fundamental cause of this round of iron phosphate price hikes, with a tight supply-demand relationship providing auxiliary support, and the upward momentum persisted throughout H1, showing no signs of slowing yet.

Driven by these costs, LFP processing fees underwent multiple rounds of upward adjustment. As of end-June: Processing fees for Gen 3 products comprehensively broke through the 19,000 yuan/mt level, a notable increase from the start of the year, with some enterprises quoting even higher prices for high-quality clients. Processing fees for double-fired products (Gen 3.5, Gen 4, and Gen 5) had already reached above 20,000 yuan/mt, demonstrating that the technical premium for high-compaction density products is fully reflected in processing fees.

Viewing it in phases, the rise in processing fees was not accomplished overnight. From end-Q1 to early Q2, material plants initiated price hike negotiations one after another, but due to varying acceptance levels among battery plants, the realized increases exhibited a gradual characteristic of being "phased, client-specific, and product-specific." High-compaction density products, leveraging the structural advantage of a tight supply-demand balance, saw the smoothest price increase implementation; conventional Gen 3 products followed; Gen 2 products faced the greatest difficulty in price hikes, and their increase range was relatively limited.

The Predicament of the Fixed-Price Model and the Breakthrough of Linkage Settlement

The process of processing fee increases during this round also exposed deep-seated problems in traditional pricing models.

For a long time, LFP processing fees have been determined in a "fixed-price" form, that is, a fixed processing fee amount is locked in for an agreed period. Under an environment of stable raw material prices, this model has been simple and efficient. However, when raw material prices such as iron phosphate experience wild swings, the drawbacks of the fixed-price model become fully apparent: material plants cannot promptly pass on cost increases downstream when raw material prices rise, while battery plants struggle to enjoy the benefits of declining costs when raw material prices fall, leading to a lack of flexibility in the distribution of interests between upstream and downstream.

The rapid rise in the sulfur → iron phosphate chain in H1 2026 precisely brought this contradiction to the forefront. On the procurement side for iron phosphate, material plants had to bear continuously rising cash costs, while on the sales side, they were constrained by locked-in fixed processing fees. Price hike negotiations lagged and were difficult, causing losses to widen correspondingly.

This predicament has made the industry more soberly aware that, to ensure the long-term healthy and stable development of the sector, LFP enterprises must establish a settlement mechanism linked to core raw materials such as iron phosphate. This involves splitting the processing fee into two parts: "iron phosphate raw material cost + fixed processing premium," where the iron phosphate component adjusts monthly in linkage with market prices. This would allow material plants to promptly transmit cost pressure when raw material prices rise and pass on benefits downstream when prices fall, thereby achieving a reasonable distribution of risk and profit between upstream and downstream.

In H1, the promotion of this model achieved crucial progress. Some leading battery cell manufacturers took the lead in accepting the settlement method linked to raw material prices, and a group of small and medium-sized battery cell manufacturers subsequently adopted it as well. The proactive stance of these battery cell manufacturers enabled the LFP enterprises bound to them to achieve timely cost transmission for some clients, gaining valuable breathing room. Although the majority of first- and second-tier battery plants have yet to change their traditional fixed-price negotiation model, the breakthrough of linkage settlement from nonexistence to existence has opened a significant entry point for the systematic optimization of the industry's settlement mechanisms going forward.

Enterprise Competitive Landscape:

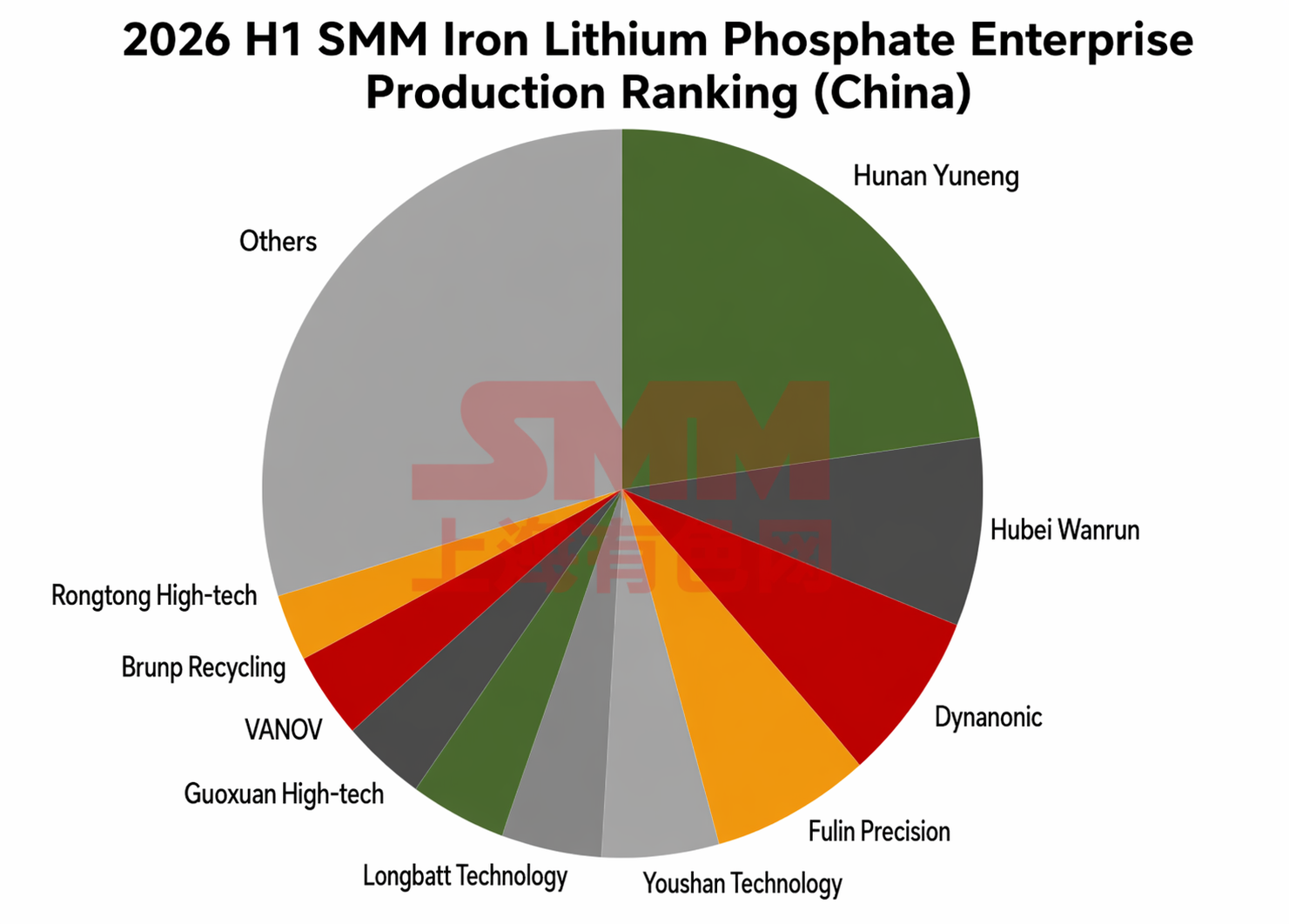

In H1 2026, the production ranking of LFP cathode material enterprises saw some changes compared to 2025. What remained unchanged, however, was that Hunan Yuneng continued to firmly hold the industry's top spot, Hubei Wanrun and Dynanonic maintained their positions in the top three, and Youshan Technology and Fulin ShengHua kept their spots in the top five, representing the industry’s stable leaders. Changes were mainly reflected in rankings after fifth place, as detailed below (Note: based on domestic production scope):

Concerning industry concentration in H1, CR5 stood at about 51%, and CR10 was about 70%, both declining from 2025. Overall, however, head-end concentration remained relatively high, with the advantages of industry leaders in technological reserves, customer relationships, and scale effects still being evident. Additionally, some third- and fourth-tier enterprises gained certain market shares through differentiated product positioning or cultivating regional markets.

However, in the ranking of overseas LFP enterprises, Lopal ranked first by an absolute margin of scale.

On the import and export front, in H1 2026, China's LFP cathode material exports continued to grow. Cumulative exports from January to June stood at about 400,000 mt, a YoY increase of roughly 5.6 times. Export destinations were mainly the US, Thailand, Vietnam, and Europe, and the overseas bases of some battery plants remained highly dependent on China-made LFP materials.

H2 Outlook: Cost Battles Continue, Linkage Promotion Is Key

Looking ahead to H2 2026, the LFP market is expected to see aggregate volume continue growing while deeper contention unfolds around cost transmission and settlement models.

On the demand side, growth in the energy storage sector has the strongest certainty. The traditional September-October peak season, combined with year-end grid connection demand for ESS projects in and outside China, is poised to support a continued MoM increase in ESS battery cell production. The overseas EV market, benefiting from low penetration rates and policy support, is also expected to maintain a growth trend in demand. China’s passenger vehicle market has limited growth potential, but commercial vehicles and increases in vehicle battery capacity will still contribute positive increments. Taken together, total output of LFP cathode materials in China for the full year is projected to reach approximately 6.2 million mt, maintaining a rapid pace of YoY increase.

In terms of costs and prices, sulfur prices are unlikely to pull back in the short term, and additions of new iron phosphate capacity are limited, keeping the overall supply-demand balance relatively tight; iron phosphate prices are highly likely to stay high. The progress in promoting linkage settlement will become the core variable of industry focus in H2. Currently, some leading battery plants and small-to-mid-sized battery cell manufacturers have already accepted this model; if more first- and second-tier battery plants follow suit in H2, it will significantly improve the efficiency of cost transmission across the entire industry. Conversely, if promotion progress falls short of expectations, the profitability pressure on material plants will persist or even intensify. The traditional fixed-price model is increasingly unable to meet the industry's needs against the backdrop of intensifying raw material price volatility. Establishing a settlement mechanism linked to core raw materials like iron phosphate has become an urgent requirement for the industry's long-term, healthy, and stable development.

In terms of product structure, the supply-demand gap for high-compaction density materials is not expected to narrow significantly in H2. Gen 4 products will remain in undersupply, and Gen 5 products are expected to achieve more bulk supply in H2. The production of conventional Gen 2 products is projected to further contract, with some enterprises potentially choosing to proactively cut production to reduce losses, while Gen 3 products will become the mainstream competitive variety in the conventional segment. The premium pricing power and superior cost transmission efficiency of high-compaction density products will continue to serve as the core guarantee of corporate profitability.

In terms of capacity rationalization, the industry already has considerable zombie capacity and outdated capacity, totaling about 650,000 mt. Conventional capacity that lacks technological advantages and has a homogeneous client structure will face greater survival pressure. For enterprises with mature technology and stable clients, the possibility of revitalizing existing "zombie capacity" through M&A or toll processing arrangements is increasing, which may offer better economics than building new capacity.

In summary, the LFP market in H2 2026 will face a parallel dynamic of aggregate growth and cost bargaining. The pace of promoting the linkage settlement model will, to a large extent, dictate the rhythm of the industry's profit recovery. High-compaction density products are expected to continue enjoying relatively strong profitability, whereas price and profit pressure on conventional products will persist. The industry is at a critical juncture transitioning from extensive expansion to refined competition, where cost control capabilities, client quality, and the pace of technological iteration will collectively determine the ultimate direction of enterprises.

SMM New Energy Research Team

SMM New Energy Research Team

Wang Cong 021-51666838

Feng Disheng 021-51666714

Yang Chaoxing 021-20707860

Wang Zihan 021-51666914

Wang Jie 021-51595902

Chen Bolin 021-51666836

Wang Yizhou 021-51595909

Xu Mengqi 021-20707868

Hu Xuejie 021-20707858

Lin Ziya 021-51666902

Yang Le 021-51595898

Li Yisha 021-51666730

Wang Zhaoyu 021-51666827

Xiao Wenhao 021-51666872

Zhang Jing 021-51666878

![[SMM Analysis] In June, the high comprehensive cost of anode materials supported the upward shift of the price center.](https://imgqn.smm.cn/usercenter/jZvMC20251217171729.jpg)

![[SMM Analysis] Raw Material Side Under Pressure and Pulled Back, Graphitisation Costs Rose Sharply, June Anode Material Costs Stayed High](https://imgqn.smm.cn/usercenter/gcOsy20251217171726.jpg)

![[SMM Analysis] Expectations vs Fundamentals: Soft Volatile Co H1 2026, Stock Drawdown Offset by Surging Secondary Cobalt](https://imgqn.smm.cn/usercenter/BmqWy20251217171726.jpg)