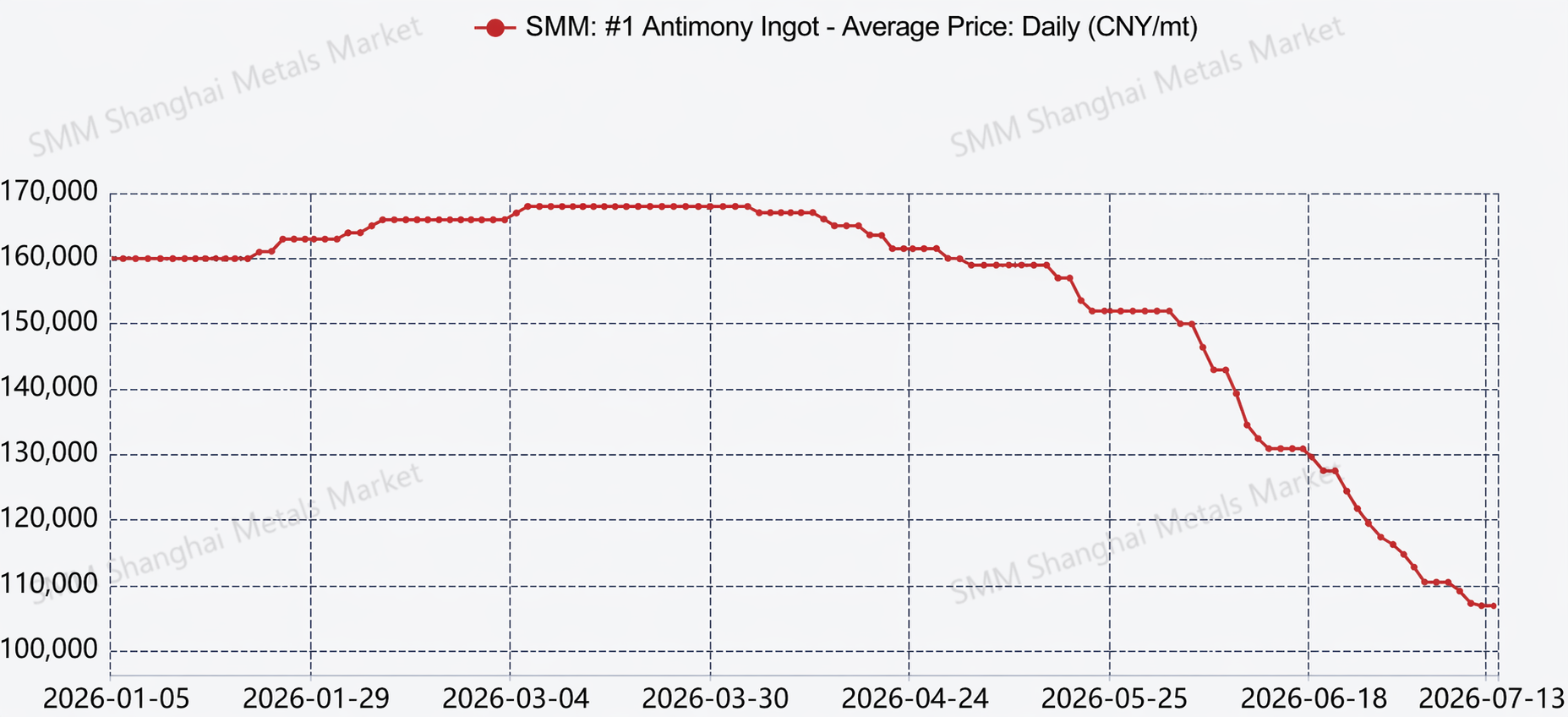

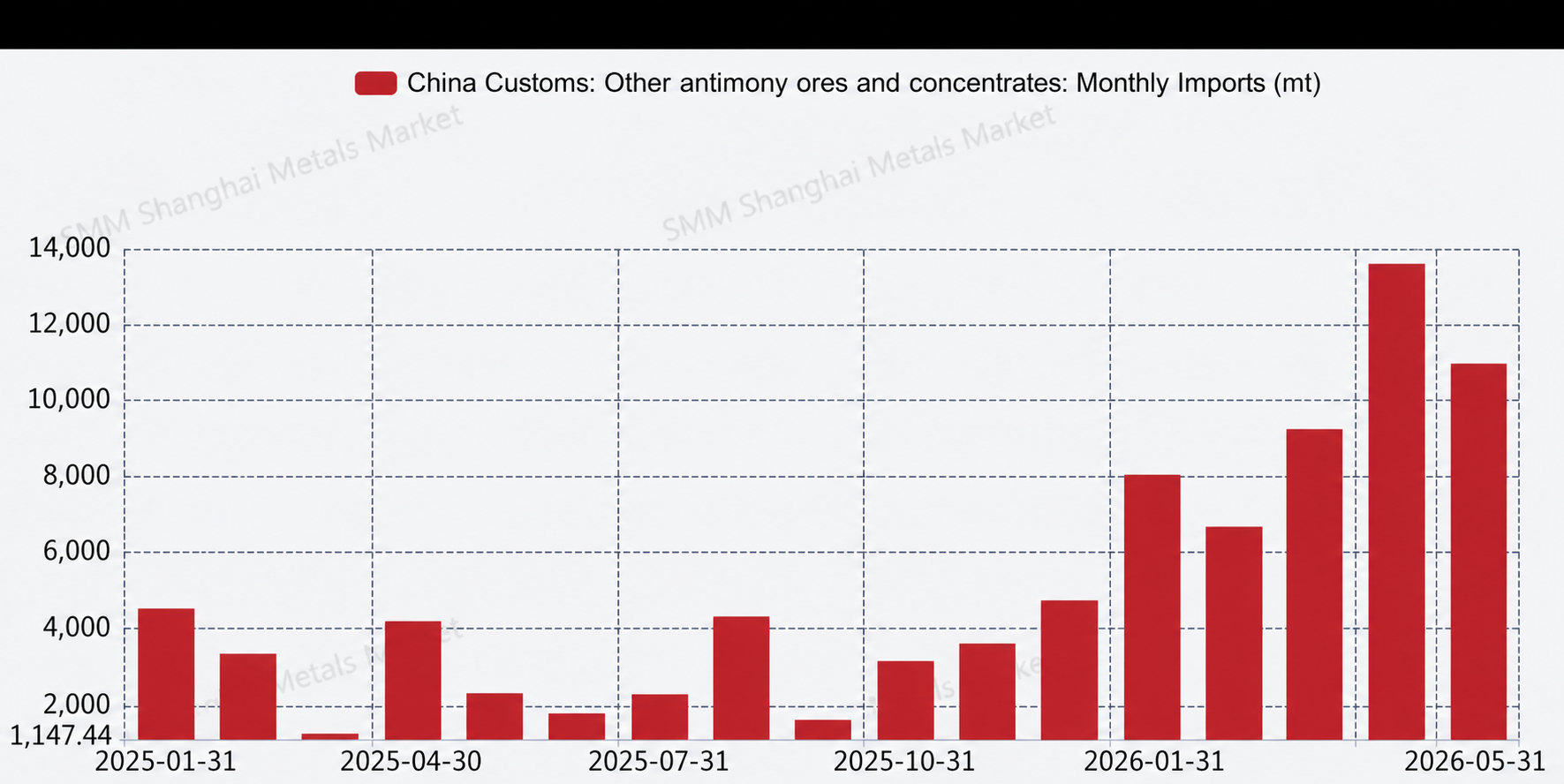

In H1 2026, the antimony market was overall weak and in a persistently sharp decline. During this period, from January to June, cumulative antimony production was slightly lower than the same period last year, down around 8% YoY; however, imports of other antimony ores and concentrates from January to May amounted to about 48,658 mt, surging 209% YoY. The large volume of antimony raw materials entering China will gradually be converted into production supply in the period ahead, and this is therefore expected to increase the likelihood of domestic production rising in the coming months. Taking domestic #1 antimony ingot as an example, the average spot price is currently around 110,000 yuan/mt, a sharp drop of about 50,000 yuan/mt from the spot price at the start of the year.

On the supply side, although production did not change much—the reason being that the industry operating rate did not see much change—some enterprises with tight antimony resources still maintained low operating rates or were shut down. Over the past nearly half year, as prices have continued on a downward trend, the risk of buying raw materials high and selling products low arose, leading these producers to become even less keen on purchasing antimony raw materials and making it difficult for operating rates to pick up. On the demand side, stockpiling sentiment in major downstream consumption sectors such as flame retardants and PV glass remained consistently mediocre, with weak buying interest. One main reason was that the relatively sluggish industries themselves led to a decline in order numbers; most importantly, under expectations of persistently low antimony prices, end-users consistently bought on an as-needed basis, were bearish on the market outlook, and tried to delay stockpiling as long as possible. Meanwhile, speculative forces that were previously active in the market also showed a lack of confidence, temporarily exiting the market and moving to the sidelines. In terms of imports and exports, mainly affected by the narrowing ex-China price spread, imported antimony ore began to flow into the Chinese market for quick monetization. Import sources were mainly Southeast Asian countries such as Myanmar and Thailand.

Looking ahead to H2, full-year production is expected to exceed 80,000 mt, up more than 5% YoY. If antimony prices can stop falling, stabilize and rebound in H2, the full-year average price is expected to be around 140,000 yuan/mt. Close attention should be paid to the trends of increase or decrease in imported antimony ore, demand-side variables, and whether there will be changes in export policies and their potential impact on the market. Furthermore, if antimony market prices stabilize and rebound, given that current antimony prices have returned to near the low-point platform of three years ago, special attention should also be paid to the impact of speculative stockpiling purchases on antimony market prices.

![Antimony Prices Continue Downward Trend [SMM Antimony Spot Market Weekly Review]](https://imgqn.smm.cn/usercenter/TdoSs20251217171724.jpeg)