SMM Feb 12 News:

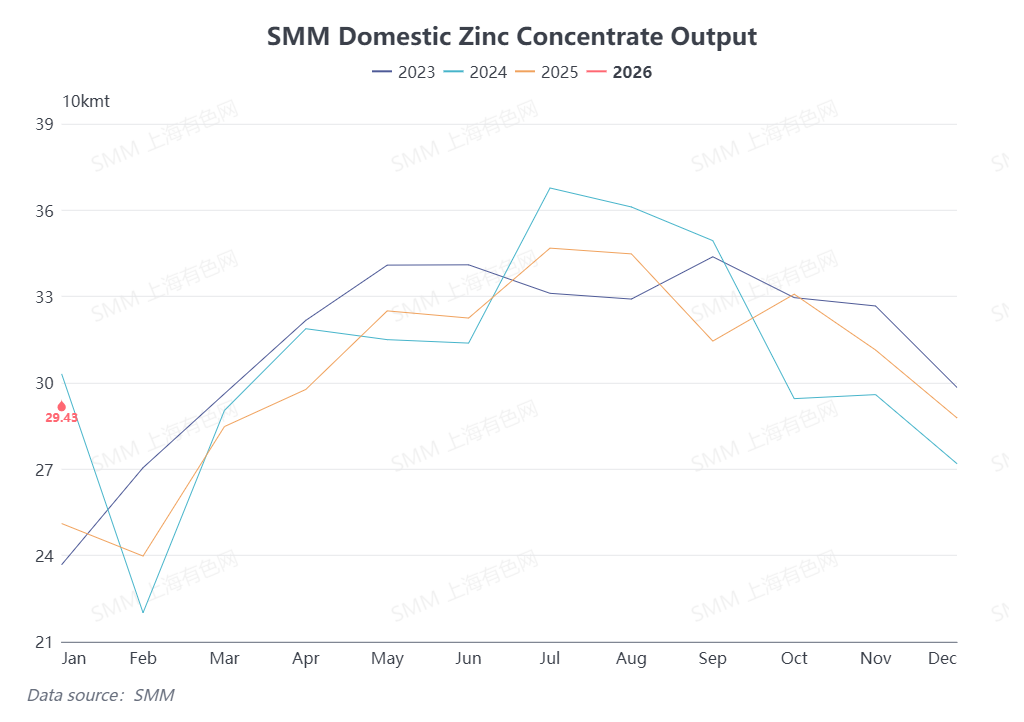

Historically, domestic zinc concentrate production typically declines continuously from December to February each year. There are two main reasons: first, some mines undergo routine shutdowns in winter due to weather conditions; second, the Chinese New Year holiday falls early in the year, during which many mines suspend operations or conduct maintenance. As this year's Chinese New Year holiday approaches, how will these factors specifically affect domestic zinc concentrate supply?

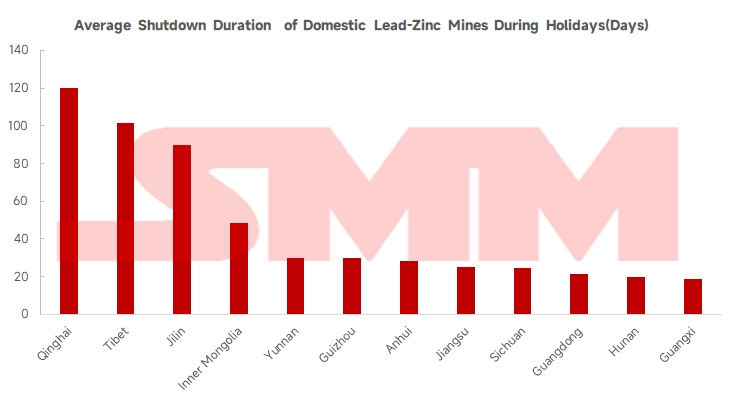

It is understood that seasonal production cuts and shutdowns are mainly concentrated in several northern provinces, such as Inner Mongolia, Qinghai, Tibet, and Xinjiang. These regions generally begin to gradually reduce production in November or December, with production resumptions mainly concentrated from March to May, resulting in a relatively long overall holiday period. Additionally, this year's Chinese New Year holiday falls in mid-February, during which some domestic mines will, as usual, suspend operations or conduct maintenance, with shutdown durations typically ranging from about 7 to 30 days. According to incomplete statistics from SMM, considering both factors, the average shutdown duration for domestic lead-zinc mines observing the holiday this year is approximately 45 days, affecting multiple provinces.

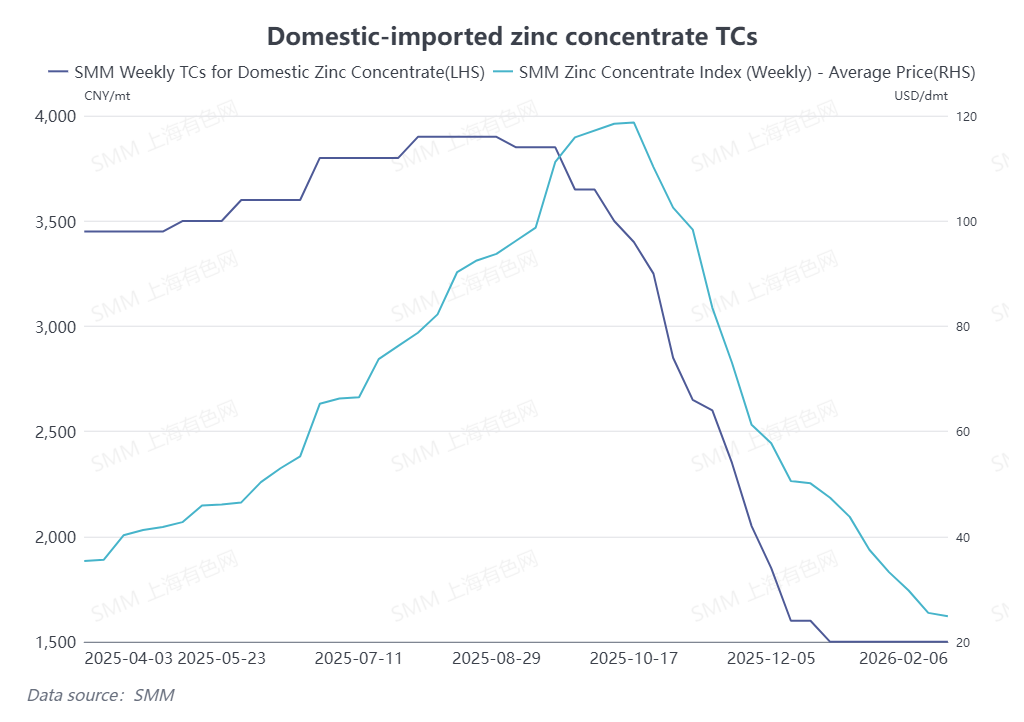

Supply-demand side, from January to February, domestic mines successively cut or halted production. However, due to continuous arrivals of imported zinc concentrates supplementing supply, raw material inventories at domestic smelters rebounded, and Chinese New Year stockpiling was largely completed, leading zinc concentrate TCs to stop falling and stabilize. Nevertheless, as most mines that suspended operations for Chinese New Year maintenance will gradually resume production by month-end February, and routinely winter-idled mines will begin restarting as early as March, with concentrated production resumptions expected in April-May, domestic zinc concentrate supply is projected to gradually recover in Q2. The overall supply-demand pattern is expected to see some improvement, and there are certain expectations for a subsequent rebound in TCs. SMM will continue to monitor and track TC performance.

(The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided in this article is for reference only. This article does not constitute direct advice for investment research and decision-making. Customers should make cautious decisions and should not replace their independent judgment with this information. Any decisions made by customers are not related to SMM.)

![Galvanizing enterprises have mostly gone on holiday, and operating rates have significantly declined [SMM Galvanizing Weekly Review]](https://imgqn.smm.cn/usercenter/PEqzX20251217171755.jpg)