6.25

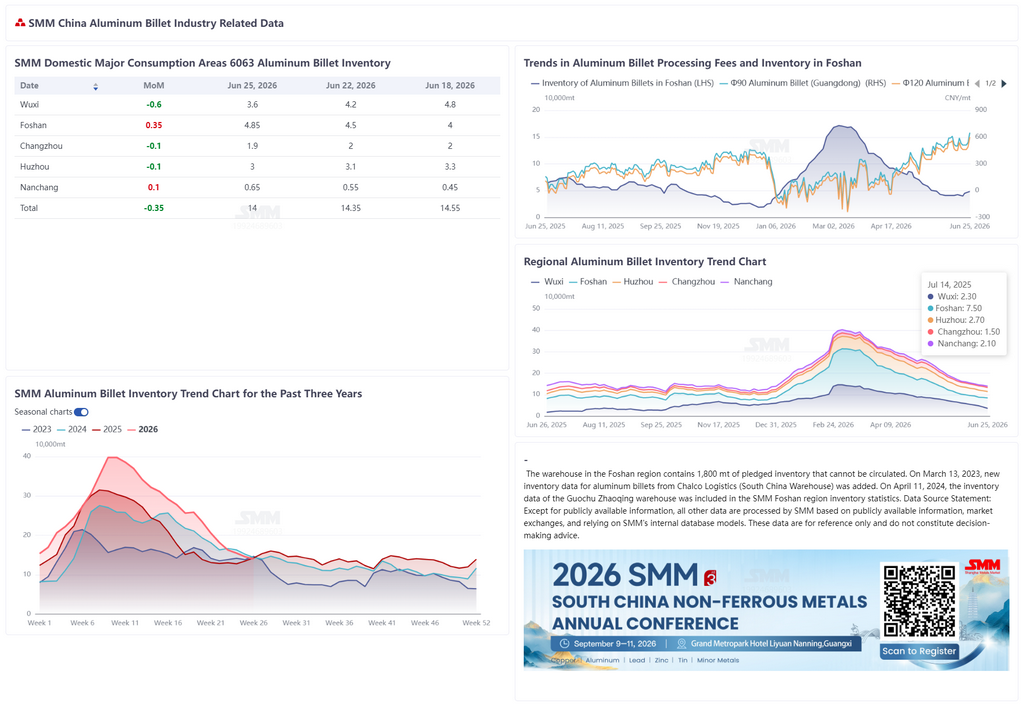

According to SMM statistics, aluminum billet inventory in major domestic consumption areas fell to 140,000 mt on June 25, down 9,000 mt from last Monday and down 3,500 mt from last Thursday. In a year-on-year comparison, it was 2,500 mt lower than the same period in 2025 and 3,500 mt lower than in 2024, with total inventory already dropping to a relatively low level for this period over the past five years. In terms of warehouse withdrawals, aluminum billet withdrawals during June 15–22 were 38,800 mt, down 5,500 mt WoW, marking the fourth consecutive week of decline, with market transactions continuing to shrink. Currently, aluminum billet inventory has dropped to near 140,000 mt. Foshan and Nanchang saw slight inventory buildup, with warehouse inflows recovering, while Wuxi experienced notable destocking, with inventory falling to 36,000 mt. The previous logic of high processing fees suppressing demand and downstream substitution effects persisted, leaving warehouse withdrawals in a downtrend for four straight weeks, reflecting sluggish demand. Based on the current supply-demand pattern and seasonal trends, aluminum billet inventory is expected to move sideways around 140,000 mt next week, with limited destocking room. Future attention should be paid to changes in downstream operating rates and the release of supply-side capacity.

During the week, the aluminum price center plunged sharply. The SMM A00 spot aluminum price dropped from 23,870 yuan/mt last Thursday to 22,850 yuan/mt, a weekly decline of over 1,000 yuan/mt. Supported by costs, processing fees in various regions surged significantly, presenting an overall pattern of volume-price divergence. By region, in Foshan, processing fees for φ90 aluminum billet were 650 yuan/mt and 600 yuan/mt for φ120, each up 140 yuan/mt from last Thursday; in Wuxi, φ90 was 700 yuan/mt and φ120 was 600 yuan/mt, each up 200 yuan/mt; in Nanchang, φ90 was 700 yuan/mt and φ120 was 650 yuan/mt, up 170 yuan/mt each. The sharp rise in processing fees during the week was driven by two main factors: first, the rapid decline in aluminum prices led manufacturers to hold prices firm based on previously high raw material costs, resulting in a passive increase in processing fees; second, inventory remained at relatively low levels, easing supply-side pressure. However, it is worth noting that under the background of high processing fees and falling aluminum prices, downstream purchasing sentiment was relatively weak, with some manufacturers switching to self-made aluminum billets, suppressing transactions through demand substitution effects. Next week, aluminum billet processing fees are expected to stay high, but with limited further upside room. Attention should be paid to the pace of aluminum price stabilization and changes in social inventory.

![US Fed Hawkish Pivot, Macro Headwinds Weigh on Nonferrous Metals Prices [SMM Aluminum Weekly Review]](https://imgqn.smm.cn/usercenter/SBQYr20251217171651.jpg)

![Cost Pressure Continues to Be Transmitted, Support Below Aluminum Fluoride Prices Strengthens [SMM Fluoride Salt Weekly Review]](https://imgqn.smm.cn/usercenter/mcZkL20251217171654.jpg)