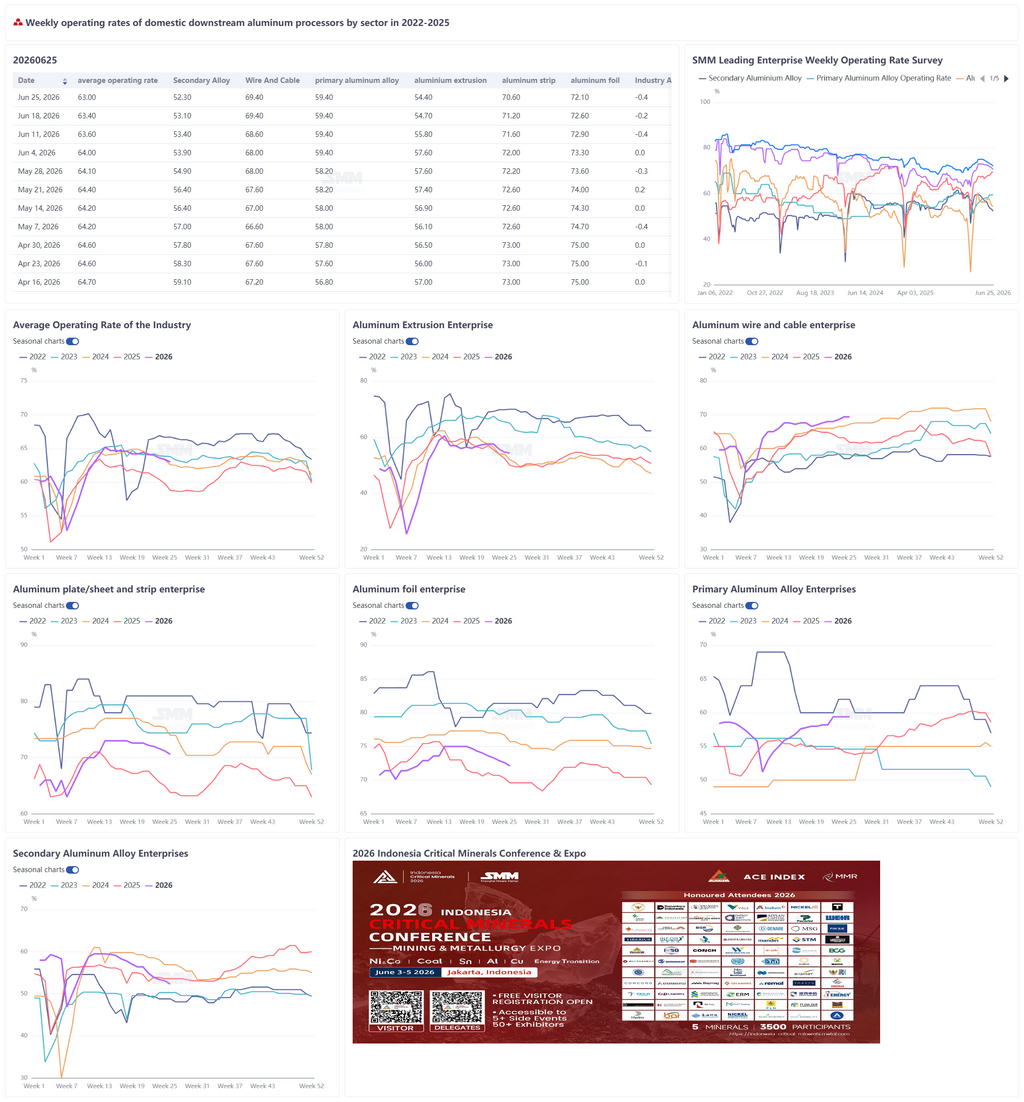

6.25:

This week, the operating rate at China's leading downstream aluminum processing enterprises came in at 63%, down 0.4 percentage points MoM. Weighed down by the deepening seasonal off-season across the sector, downstream purchase willingness was broadly subdued, and operating rates across most segments remained under pressure. Primary aluminum alloy held steady at 59.4%, as enterprises mainly focused on executing existing long-term contracts, with no release of new spot orders. The aluminum plate/sheet and strip operating rate fell 0.6 percentage points to 70.6%, as an abrupt slump in aluminum prices disrupted cargo pick-up pace, forcing some small plants to halt production. While exports showed resilience, weak domestic common plate demand offered limited offsets. The aluminum wire and cable operating rate was flat at 69.4%, supported by the steady delivery of UHV orders. However, export losses and shrinking new orders signaled increasing downward pressure after July. Aluminum extrusion operating rates edged down 0.3 percentage points to 54.4%. Falling aluminum prices marginally improved end-user stockpiling, but sluggish order-taking at small and medium-sized enterprises and the persistent off-season in architectural extrusions meant these positives were insufficient to offset the weakness. Aluminum foil operating rates slipped 0.5 percentage points to 72.1%, with pharmaceutical foil demand halving and pouch foil weakening. Some clients introduced intermittent holidays, intensifying operational pressure. Secondary aluminum operating rates dropped 0.9 percentage points to 52.3%, as tight invoice sourcing, aluminum scrap suppliers holding back from selling, and downstream just-in-time restocking combined to push operating rates lower under dual pressure from raw materials and demand. Overall, the resonance between wild swings in aluminum prices and the off-season effect meant that local resilience in exports was not enough to offset weakening domestic demand and raw material-side pressure. In the short term, aluminum wire and cable is expected to fluctuate at highs, supported by power grid orders, while other segments will likely remain under pressure.

Primary Aluminum Alloy: This week, the operating rate at China's leading primary aluminum alloy enterprises held steady at 59.4%, flat with the previous week, continuing its stable trend. On the supply side, enterprises did not make notable adjustments to their production pace, focusing mainly on executing existing long-term contracts. No large-scale plans to increase or cut production were reported, leaving the operating rate unchanged for two consecutive weeks. On the demand side, the industry is currently in its traditional off-season, with downstream consumption generally weak and new orders relatively limited. Some enterprises still face certain inventory pressure. Although aluminum prices weakened somewhat recently, market reactions were mainly reflected in trader quotes, as downstream actual purchase willingness did not notably release, offering limited boost to operating rates. Furthermore, on the export front, wheel hub exports fell MoM in May, and overall demand in June is expected to show a lackluster performance, suggesting insufficient support from overseas demand. Taken together, the current operating level at industry leaders is sufficient to cover the delivery of existing orders. Constrained by weak off-season demand, not-yet-fully-digested inventory, and lackluster exports, the operating rate lacks upward drivers. The leading primary aluminum alloy enterprises' operating rate is expected to remain near 59.4% next week, continuing its weak but stable trend.

Aluminum Plate/Sheet and Strip: This week, the operating rate at leading aluminum plate/sheet and strip enterprises fell 0.6 percentage points MoM to 70.6%. In terms of corporate operations, aluminum prices plummeted during the week, with spot aluminum closing at 22,850 yuan/mt on June 25, down 1,020 yuan/mt for the week. The wild swings significantly impacted market sentiment, markedly weakening downstream willingness to pick up goods, and some clients, including small sheet/plate plants and workshop-style enterprises, were forced to halt production. Regarding orders, exports remained resilient. Aluminum plate/sheet and strip exports in May were 319,900 mt, edging down 2% MoM but still recording a 15% YoY increase, and the export order books at related enterprises were full. Domestic demand was mediocre, with end-use demand for common civil plate remaining persistently weak. Overall, while exports and energy storage orders provide some support, the arrival of the consumption off-season, weak common plate performance, and wild swings in aluminum prices disrupting downstream procurement pace mean the aluminum plate/sheet and strip operating rate is expected to fall under pressure in July.

Aluminum Wire and Cable: This week, the operating rate in China's aluminum wire and cable industry was 69.4%, flat MoM. Sector operations hovered at highs during the week, with enterprises primarily executing orders on hand, maintaining a stable production schedule pace, and keeping capacity utilization rates at relatively high annual levels. On the order side, the export market showed a clear cooling trend. Influenced by successive drops in overseas LME aluminum, export profits for domestic aluminum stranded wire moved into losses, and new order volumes shrank significantly, leaving only some orders placed in advance by traders aiming to lock in the price spread between Chinese and overseas markets. Although producers' existing production schedules can still cover output for the entire month, and aluminum stranded wire exports are expected to remain stable in June, after July, as previously scheduled orders are gradually delivered and new orders become hard to secure—on the domestic front, long-cycle UHV orders are still being delivered steadily, but a period of concentrated cargo pick-up by the power grid has yet to emerge. However, the sharp drop in raw material prices recently led enterprises to focus on facilitating pending production orders, providing some support for conductor-type orders. Against a backdrop of rising expectations of subsequent pressure on the export front, the sector's short-term operating rate may fluctuate at highs, but after July, as export orders gradually contract, downward pressure on the operating rate will likely increase.

Aluminum Extrusion: This week, the aluminum extrusion operating rate edged down 0.3 percentage points MoM to 54.4%, with the sector's downward pace slowing compared to the prior period. In architectural extrusions, benefiting from the recent pullback in aluminum prices, downstream end-user procurement and stockpiling willingness marginally improved, with new valid orders partially offsetting the off-season characteristics and supporting stable operating rates at architectural extrusion enterprises. In industrial extrusions, improving downstream demand for energy storage-related aluminum extrusions boosted enterprise operations. However, some enterprises reported a short-term shortage of front-line production labor, limiting capacity release and leading to a slight pullback in operating rates. The divergence between large and small enterprises persisted, with some small enterprises reporting a notable decline in recently received new orders and expecting their production to fall MoM in July. Overall, the recent aluminum price decline effectively spurred end-use demand release, providing short-term positive support for the sector’s operations. However, sluggish order-taking at small and medium-sized extrusion enterprises continued to drag on the overall operating level; meanwhile, the traditional off-season effect for architectural extrusions persisted, with weak follow-through of new orders from real estate projects, leaving thin demand support. In conclusion, short-term positive factors were not enough to offset weak off-season demand, and China's aluminum extrusion industry operating rate is expected to continue its downtrend next week.

Aluminum Foil: The operating rate of leading aluminum foil enterprises fell 0.5 percentage points MoM to 72.1% this week. At the enterprise operation level, the traditional July-August off-season effect accelerated, with pharmaceutical foil demand halving and pouch foil demand continuing to weaken. Some aluminum foil clients have started taking intermittent holidays due to insufficient orders, and industry operational pressure clearly intensified. On the export side, customs data show aluminum foil exports in May were 119,400 mt, up 4% MoM, indicating relatively stable overseas demand. Notably, the sharp drop in aluminum prices this week significantly disrupted market mentality. Downstream clients showed markedly insufficient willingness to pick up goods, and processing enterprises began reviewing their order structures and postponing production schedules for stockpiling-type orders. Against the backdrop of a deepening off-season effect in July, persistently weakening packaging foil, insufficient support from air-conditioner foil consumption, and wild swings in aluminum prices are expected to jointly suppress operating performance, causing the aluminum foil operating rate to continue declining.

Secondary Aluminum: This week, the operating rate at leading secondary aluminum enterprises fell 0.9 percentage points MoM to 52.3%, as dual pressure from raw materials and demand continued to constrain capacity release. On the raw material side, accelerating declines in aluminum prices and futures during the week caused aluminum scrap prices to follow suit, easing the way for ADC12 prices to pull back, but overall aluminum scrap still showed relatively strong resistance to declines. Against the backdrop of a strict crackdown on the "invoicing economy," the issue of tight invoice sourcing has yet to ease, keeping procurement costs for compliant raw materials high. Meanwhile, the price decline further squeezed profits for aluminum scrap suppliers, intensifying their willingness to hold back from selling. Market circulation tightened, and enterprises continued to face significant pressure in securing raw material supply. On the demand side, the downstream market sustained its traditional off-season pattern, with procurement dominated by just-in-time restocking. Although aluminum prices fell successively, this failed to boost downstream restocking enthusiasm. A wait-and-see sentiment dominated the market, overall transactions were mediocre, and the demand side provided limited impetus for production. Looking ahead, if the tight invoice sourcing situation persists, compliance supervision remains stringent, and the end-use off-season effect further unfolds, there is still potential for the secondary aluminum industry's operating rate to continue declining.

![US Fed Hawkish Pivot, Macro Headwinds Weigh on Nonferrous Metals Prices [SMM Aluminum Weekly Review]](https://imgqn.smm.cn/usercenter/SBQYr20251217171651.jpg)

![Cost Pressure Continues to Be Transmitted, Support Below Aluminum Fluoride Prices Strengthens [SMM Fluoride Salt Weekly Review]](https://imgqn.smm.cn/usercenter/mcZkL20251217171654.jpg)