In H1 2026, the secondary copper rod market completely broke away from the traditional "copper price–supply and demand" pricing framework. It was primarily hit by the twin policy shocks of "reverse invoicing" moving from transitional review to full implementation and the clearance of local non-compliant fiscal and tax incentives and subsidies (Document No. 770). Coupled with the most-traded SHFE copper contract retreating from a historical high of 113,800 yuan/mt early in the year and holding the 100,000 yuan/mt level through mid-year amid wide fluctuations, the entire industry was mired in a deep stalemate where "policy determined structure, invoices locked transactions, and copper prices set the pace." The operating rate slumped YoY, and enterprises generally walked a tightrope between compliance pressure and weak demand.

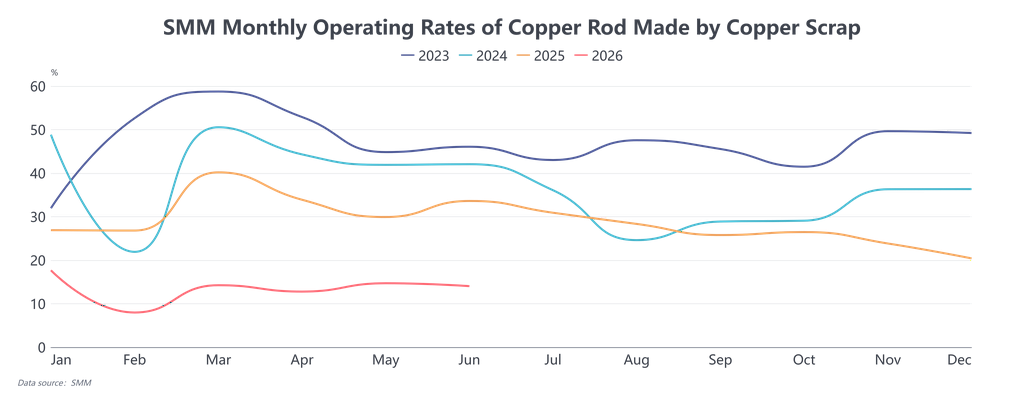

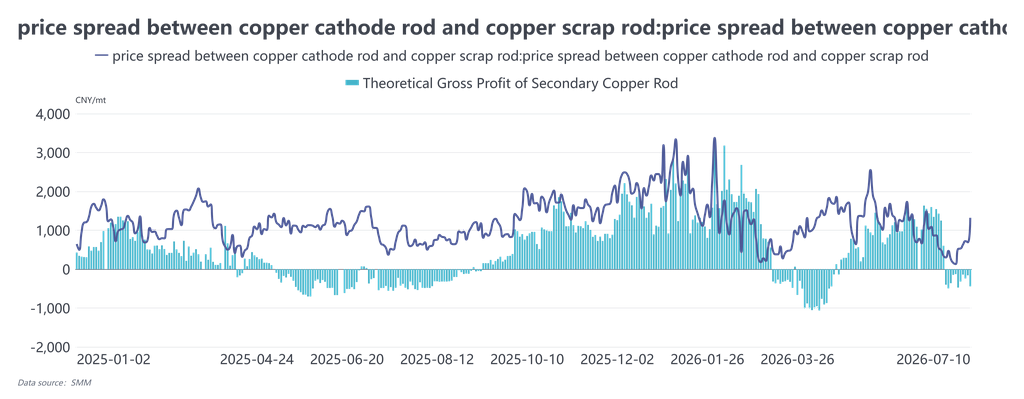

The core contradiction on the supply side has never been an overall shortage of copper scrap, but rather a scarcity of effective supplies that are "compliant for invoicing and ensure stable payment collection." This was also the fundamental variable constraining supply in H1. Early in the year, as the reverse invoicing policy was first rolled out, tax audits tightened across regions. Enterprises were forced to abandon previously non-compliant, low-priced sources and fully shift to purchasing domestically produced tax-inclusive or imported copper scrap with higher invoice tax rates. The invoice tax rate jumped from 9.1%–9.3% at the start of the year to over 10.5% by March. The cost of tax-inclusive raw materials rose rigidly, even resulting in losses where tax-inclusive copper scrap prices exceeded spot copper cathode prices, directly locking the cost floor of secondary copper rod. Even when copper prices retreated, raw material prices found it difficult to fall in tandem. In Q2, regions in south China such as Jiangxi, Hubei, and Shuyang in Jiangsu successively advanced compliance inspections on reverse invoicing and restricted invoicing quotas. Many small and medium rod enterprises suspended production due to insufficient invoices, further tightening the supply of compliant and invoice-capable material, and regional divergence became pronounced: in south China, due to slow working capital turnover and high compliance costs, the purchase price of bare bright copper was 400–600 yuan/mt lower than in the north. This abnormal structure of different prices for the same material was inherently a geographical difference in compliance costs, not a supply-demand gap. Meanwhile, the payment collection period was extended from the previous 3–5 days to more than two weeks. Traders faced severe capital tie-ups and were unwilling to stockpile and bet on price increases, generally switching to a "fast in, fast out to secure cash flow" strategy. Some even adopted a model of "raw material consignment plus installment settlement" with rod enterprises, further raising the actual circulation cost of raw materials. Constrained by these factors, the average operating rate of secondary copper rod in H1 was only about 13.8%, down 18 percentage points from the same period in 2025. After the Chinese New Year, the lowest weekly operating rate was just 2.15%, and even in March, the traditional peak season, it only rebounded to 14.25%. Capacity could never be released. Some enterprises, because their anode plate long-term contracts were stable and offered a discount to futures, opted to retain anode plate capacity, further reducing the supply elasticity of secondary copper rod. Demand side, constrained by high copper prices, unstable spreads, and reverse billing constraints, never gained endogenous growth momentum. In H1, absolute copper prices remained above 100,000 yuan/mt, and orders from terminal sectors such as wire and cable, real estate, and infrastructure were already weak. They widely adopted a “demand deferral” strategy to await copper price corrections. Especially in Q2, as copper prices repeatedly tested the 100,000 mark, end-users formed a consensus of “buy only after breaking below 100,000,” limiting procurement to rigid demand pulses. Traditional stockpiling activity for Chinese New Year and Dragon Boat Festival failed to materialize entirely. The price difference between copper cathode rod and secondary copper rod swung wildly in H1, collapsing from a historical peak of 6,000 yuan/mt in January to negative territory in March. For most of Q2, it fluctuated within 300–1,500 yuan/mt, never stably standing above the 1,500 yuan/mt economic viability threshold for secondary copper rod. Owing to rigid raw material costs, secondary copper rod frequently traded at a premium to copper futures, leading end-users to favor copper cathode rod or shaft furnace rod, further squeezing demand for secondary rod. Meanwhile, demand was also constrained by reverse billing: downstream procurement required matching compliant input invoices. Even if secondary copper rod prices were low, transactions remained difficult if suppliers could not issue invoices, further compressing effective demand. Throughout H1, secondary copper rod transactions were largely triggered by copper price fluctuations, without continuous volume releases. Although enterprises’ gross margins fluctuated with spreads and held around 1,000 yuan/mt, stability was extremely poor; most of the time, they survived by drawing down earlier inventories or engaging in spread arbitrage, with very weak risk resilience.

Overall, the core logic of the secondary copper rod market in H1 has shifted from a traditional “price–supply/demand” game to a structural game of “compliance costs–invoice settlement–end-user orders.” The essence of the “copper shortage” is a “shortage of compliantly settleable copper.” Looking ahead to H2, the key to breaking the deadlock hinges on two variables: first, whether the implementation rules for reverse invoicing can be further clarified—if invoicing quotas are relaxed and procedures simplified, the tightness in compliant supply may ease; second, whether copper prices can fall below the 100,000 yuan/mt mark to release pent-up end-user demand, and coupled with a substantive recovery in orders from power grid, infrastructure, and other sectors, if the economic viability of secondary copper rod is stably restored, transactions could see marginal improvement. If neither variable progresses positively, the stalemate of weak supply and demand will persist, and the industry may continue to operate within the triangle of “must produce–blocked by invoices–control payment terms.”