- SMM Cold Rolling Production Schedule: Daily average cold rolling production schedule at steel mills increased 3% in February

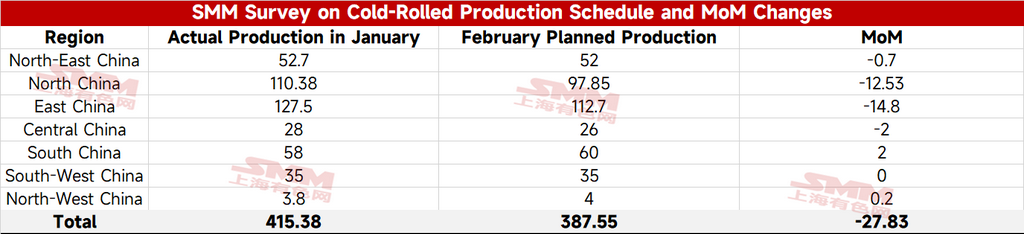

According to the latest SMM tracking, the total planned volume of cold rolled commodity materials from 31 mainstream steel mills this month was 3.8755 million mt, down 278,300 mt MoM from the actual production of cold rolled commodity materials last month, a decrease of 6.7%.

On a daily average basis, with February having 3 fewer days than January, the daily average production schedule for cold rolled commodity materials in February was 138,400 mt, up 3.3% MoM from the daily average actual production of cold rolled commodity materials last month.

- SMM HRC production schedule: February HRC production schedule down 7% MoM, daily average up 3%

According to the latest SMM tracking, the total planned volume of HRC commercial material from 39 mainstream steel mills this month is 12.8307 million mt, down 923,600 mt, or 6.7%, from the actual HRC commercial material production last month.

On a daily average basis, with 3 fewer days in February than in January, the daily average HRC commercial material production schedule for February was 458,200 mt, up 3.3% MoM from the actual daily average production last month.

In February, some steel mills in east China, northern and central China announced maintenance plans, and the impact from maintenance in February increased MoM from January, leading to a nearly 7% MoM decline in planned production of hot-rolled steel in February. However, due to fewer days in February, the daily average planned production showed an upward trend MoM compared to January.

Summary: Affected by steel mill maintenance, the total production schedule of hot-rolled commercial steel products in February decreased MoM. However, due to fewer days in February, the daily average production schedule rose 3% compared to January. Demand side, with the Chinese New Year approaching, market demand gradually stagnated, and SMM's total hot-rolled coil inventory began the Chinese New Year inventory buildup cycle at the end of January.

Post-Chinese New Year, attention should be paid to the extent of inventory buildup and the inflection point of destocking, as well as the boost from post-holiday steel mill restocking and expectations for key macro meetings. Considering downstream demand is expected to gradually pick up starting in March, be cautious of the risk that sheet & plate prices may retreat after a rapid rise if demand recovery falls short of expectations after the macro meeting period.

![Iron ore prices are expected to remain volatile in the short term [SMM Brief Review]](https://imgqn.smm.cn/usercenter/VgxkU20251217171719.jpg)

![[SMM Sheets & Plates Daily Review] Market transactions gradually stalled, intraday HRC prices were basically stable.](https://imgqn.smm.cn/usercenter/UqlZJ20251217171717.jpg)