SMM, July 12:

In the first half of 2026, China's aluminum extrusion industry presented an extreme pattern of structural divergence. Traditional construction extrusion demand remained persistently weak, dragging down the industry’s overall operating load, while industrial extrusion maintained high prosperity, underpinned by new energy, power, and heat dissipation sectors, serving as the core pillar of the industry. Meanwhile, linked volatility in aluminum prices intensified both in and outside China, with the price spread repeatedly narrowing. The export market experienced a "deep V-shaped recovery" trajectory, and the overall industry performance was characterized by "weak recovery in domestic demand, initial suppression followed by recovery in overseas demand, and a stark contrast between strong and weak structural segments."

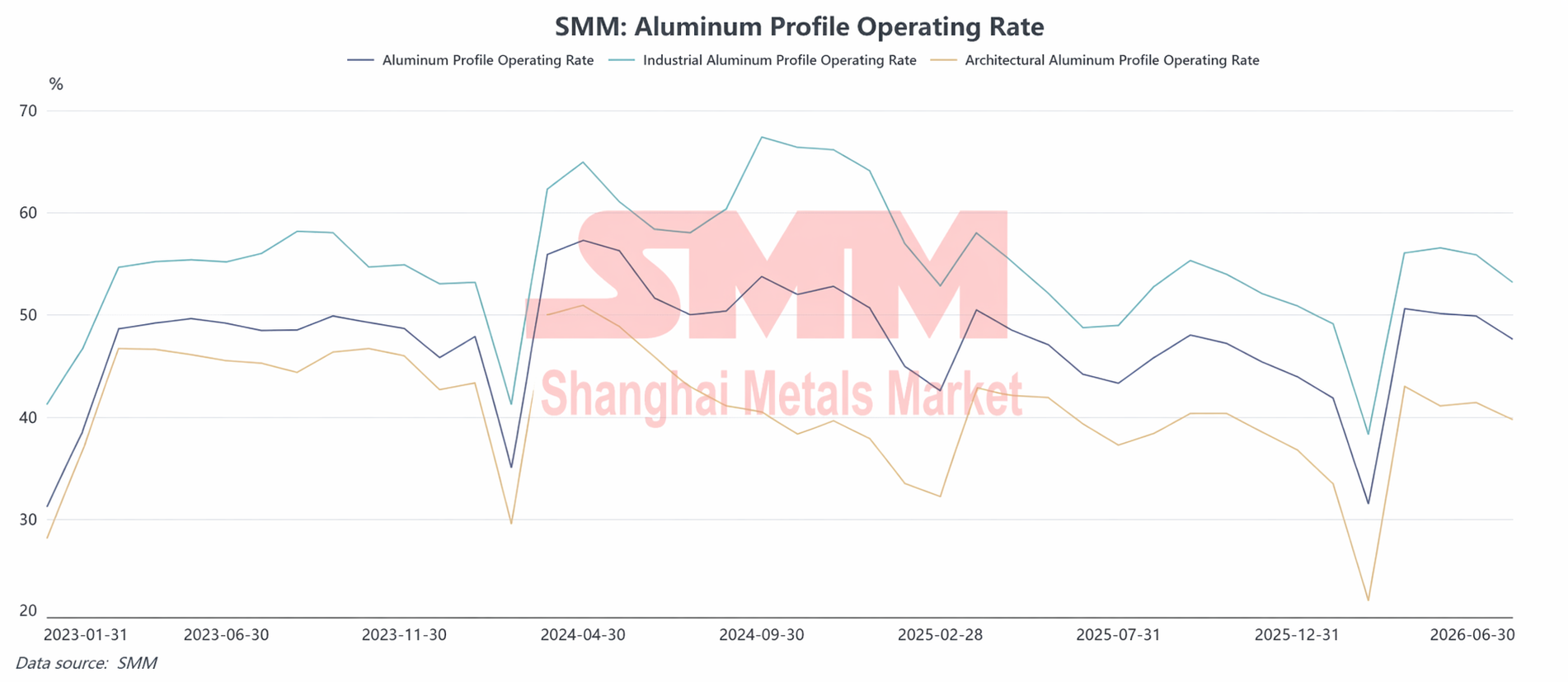

1. Extrusion Operating Rates: Construction Extrusion Continued to Drag, Industrial Extrusion Resilience Supported the Industry

After the 2026 Chinese New Year, the industry entered its traditional peak season for resuming work. In March, extrusion enterprises concentrated on production resumptions and downstream clients engaged in concentrated restocking, pushing the industry's composite operating rate to its H1 peak of 50.6%. Entering Q2, genuine downstream demand follow-through was insufficient, raw material prices fluctuated at high levels, and the industry was further impacted by the rainy season in south China and environmental protection inspections in some regions. As a result, the industry operating rate continued to pull back mildly, falling to 47.6% in June, with the overall operating level weaker than the average for the same period over the past three years.

Construction extrusion was the core weak spot dragging down the industry’s overall operations. In H1, data on commercial housing transactions and new construction starts in China remained persistently weak; developers' financial positions showed no significant improvement, and payment returns from project sites were slow. Orders for housing construction-related doors, windows, and curtain wall extrusions continued to shrink. From January to May, domestic aluminum prices generally consolidated at highs, and downstream end-users exhibited strong resistance to high-priced raw materials. Traders and processing plants generally maintained low inventory levels, moving goods in and out quickly, with low willingness to initiate restocking. Although the industry actively expanded non-residential construction demand from industrial parks, standard factories, and government and enterprise public buildings, and home decoration for existing home renovations and home decoration retail recovered slightly, the incremental volume was limited, completely failing to offset the decline in bulk project orders. In H1, construction extrusion operations remained under pressure, making it the biggest drag on the industry.

The structural prosperity of the industrial extrusion segment continued to rise, strongly underpinning the industry's operating rates. Demand for power transmission and transformation, energy storage structural components, industrial heat dissipation extrusions, and rail transit supporting profiles maintained steady growth. For PV extrusion, affected by the official cancellation of the export tax rebate policy for PV-related products on April 1, overseas clients concentrated on front-loading orders and enterprises rushed to meet production deadlines in Q1, driving the operating rates for PV frames and mounting extrusions to stage a temporary surge. After the policy took effect, the bonus from overseas rush orders faded, and PV extrusion production schedules returned to rationality, maintaining stable operation from April to June. NEV extrusions showed structural divergence: demand for lightweight extrusions for auto body and chassis remained robust, while demand for ordinary interior extrusions weakened. Overall, the resonance of prosperity across multiple industrial extrusion tracks effectively offset the weak demand for traditional construction materials, highlighting the structural resilience of the industry.

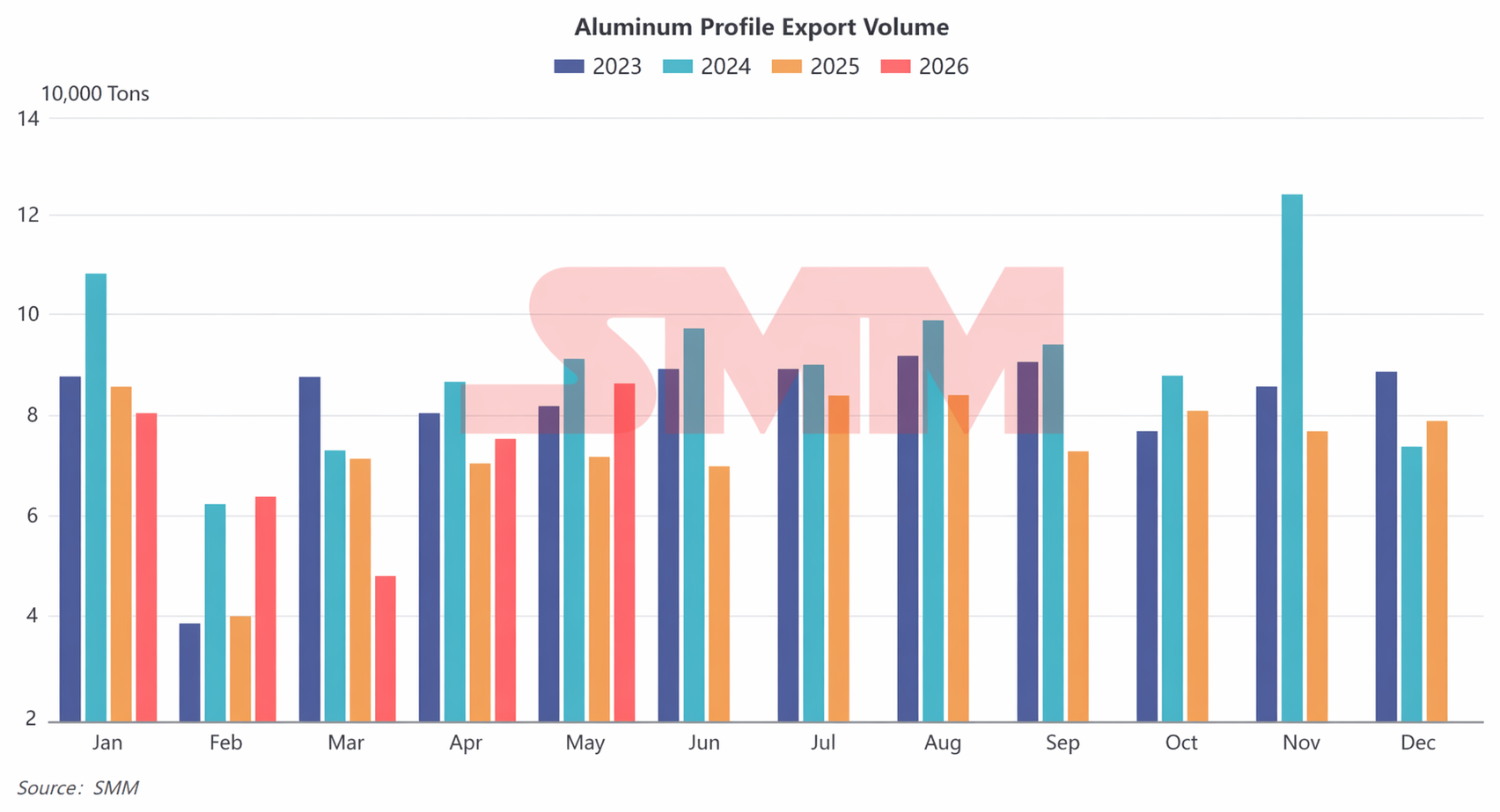

2. Aluminum Extrusion Exports: Deeply Under Pressure in Q1, Continuous Recovery in Q2, V-Shaped Reversal in H1

In H1 2026, China's aluminum extrusion exports followed a V-shaped trend overall, with a sharp decline in Q1 followed by consecutive recoveries in Q2. The driving logic shifted from price inversions and off-season effects overseas at the beginning of the year, towards the release of demand in emerging markets and the transfer of China's processing and manufacturing advantages.

Q1: Domestic and Overseas Aluminum Price Inversions Combined with Overseas Off-Season Led to Sharply Weaker Exports

Exports from January to February showed off-season resilience, mainly supported by deliveries for orders placed ahead of the Chinese New Year. In January, China exported 81,000 mt of aluminum extrusions, up slightly by 1.4% MoM but down slightly by 5.3% YoY. In February, disruptions from the Chinese New Year holiday saw exports fall to 64,000 mt, a 20.4% MoM decrease but a sharp 62% YoY increase, significantly outperforming the precipitous declines of past Chinese New Year periods. The core reason was that secondary aluminum extrusion enterprises in Guangdong and Fujian concentrated on delivering orders for Southeast Asia and the Middle East before the holiday, while some industrial extrusion enterprises adopted a model of "preliminary domestic processing and deep processing overseas" to speed up contract fulfillment, supporting export volumes at the start of the year.

In March, industry exports hit their low point for the first half of the year, with monthly exports of only 48,000 mt, down 24.8% MoM and plunging 32.8% YoY. The core reason for this export slump was not a single geopolitical factor but the resonance of multiple negative factors: first, orders placed ahead of the Chinese New Year overdrew demand from February and March, after which overseas markets entered the traditional consumption off-season; second, LME aluminum saw wild swings in March, and domestic and overseas aluminum prices quickly inverted, compressing export profits for domestic extrusions and leading enterprises to proactively control volumes and take fewer orders; third, the European and US CBAM carbon tariff continued to suppress high-end extrusion exports, causing continuous market shrinkage there, coupled with a slowdown in logistics and customs clearance in some Middle Eastern regions. These multiple factors caused a substantial pullback in export volumes in March.

Q2: Emerging Market Volume Surge, Exports See Double YoY and MoM Growth for Two Consecutive Months

Starting in April, the price spread between China and overseas markets gradually recovered, the overseas off-season ended, and industry exports began a continuous recovery channel. Exports that month were 76,000 mt, surging 56.8% MoM and up 6.9% YoY, returning to the normal range for past years. Trade and logistics order in the Middle East recovered, stockpiling in Southeast Asia ahead of the rainy season began, and domestic enterprises accelerated their layout in emerging markets in Central Asia and Latin America. Leveraging overseas affiliated warehouses and cross-border stockpiling models to continuously take on rigid demand orders for overseas doors, windows, and curtain walls, export prosperity recovered rapidly.

Exports in May continued their high-growth momentum, hitting the monthly peak for H1 at 87,000 mt, up 14.6% MoM and 20.1% YoY. The export structure continued to optimize; low-end construction extrusions saw steady incremental growth, while the export share of high-value-added industrial aluminum components, outdoor aluminum semis, and PV supporting extrusions continued to rise. Southeast Asia, Australia, South America, and Central Asia became the four core growth markets for domestic extrusion exports, effectively offsetting the shrinking demand in European and US markets.

3. H2 2026 Industry Outlook: Weakly Stable Domestic Demand, Marginal Export Weakness, Continued Structural Divergence

Looking ahead to H2 2026, the structural divergence pattern in China's aluminum extrusion industry is expected to become further entrenched, with overall operations characterized by "consolidation on a subdued note, industrial support, and construction material drag."

On the domestic demand side, the fundamentals of the real estate sector are hard-pressed to see a substantive repair in the short term. Commercial housing new starts and project payment returns are expected to remain weak, and construction extrusion demand will continue to operate in a low range without a trending recovery. Non-residential infrastructure and home decoration retail can only provide a slight offset, unable to reverse the overall weakness of construction extrusions. Industrial extrusion will remain the core pillar of the industry: in H2, steady climbing of domestic PV installations will drive the continued release of demand for PV frames and mounting extrusions; demand for new-type energy storage, data center heat dissipation, and power equipment extrusions will maintain steady incremental growth. NEV extrusions will show a divergence between strong and weak segments; demand for high-end lightweight structural components will be firm, but overall industry overcapacity and intensifying end-user competition will exert marginal contraction pressure on demand for ordinary automotive extrusions. Overall, industrial extrusion can defend the industry’s baseline but can hardly offset the downward pressure from construction extrusions. In H2, the industry's overall operating rate may be slightly lower than in H1.

Pressure on the export front will gradually emerge, with the trend potentially turning from the high growth of Q2 to a mild slowdown. In H2, the bonus from overseas traditional peak seasons will gradually fade, while the domestic-overseas aluminum price spread narrows, export processing profits are compressed, and overseas local aluminum processing capacity continues to be released, alongside persistent trade barriers against Chinese aluminum semis in some countries. This will gradually weaken the price advantage of domestic extrusion exports. Although secondary aluminum extrusion exports may still hold cost advantages, homogenized competition in low-end products is fierce and profits remain compressed. The export growth rate for aluminum extrusions is expected to slow down gradually in H2, with overall volumes weaker than in Q2.

In summary, throughout 2026, the aluminum extrusion industry is expected to continuously exhibit structural characteristics of weak construction, strong industrial, stable but weak domestic demand, and exports that are high in the first half and low in the second. Industry competition will further concentrate on high-end industrial extrusion, high-value-added deep processing, and overseas emerging markets, with low-end construction extrusion capacity continuously entering a phase of being cleared.

![Approaching the Weekend, Prices Rise Again, Spot Aluminum Pressure Intensifies [SMM South China Spot Aluminum Daily Review]](https://imgqn.smm.cn/usercenter/VTjoW20251217171653.jpg)