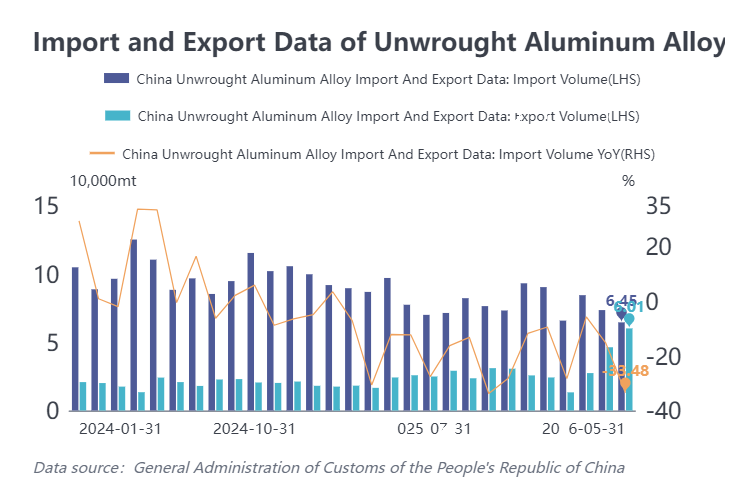

Customs data show: In May 2026, imports of unwrought aluminum alloy totaled 64,500 mt, down 33.5% YoY and down 12.1% MoM. Cumulative imports from January to May 2026 reached 378,500 mt, down 18.6% YoY.

In May 2026, exports of unwrought aluminum alloy totaled 60,100 mt, surging 148.7% YoY and up 29.9% MoM. Cumulative exports from January to May 2026 reached 171,400 mt, up 81.3% YoY.

From the import source structure, China's unwrought aluminum alloy imports remained highly concentrated in May 2026, with the top five source countries accounting for about 78% of the total. Among them, Russia overtook Malaysia to become the top source, with 18,000 mt (28% share). Malaysia fell to second place with 17,000 mt (26% share). Thailand, Vietnam, and Indonesia ranked third to fifth, with imports of 7,000 mt, 6,000 mt, and 2,000 mt, respectively. On a MoM basis, among the top five sources, besides Russia's imports increasing by 6,000 mt, the other four all saw declines ranging from 1,000 to 6,000 mt, resulting in a total MoM decrease of about 9,000 mt.

From the export destination structure, Japan remained the largest export destination, with exports of 20,000 mt in May, accounting for 34% (pulled back from the previous month's high of 49%). The trade mode was primarily processing trade with supplied materials. South Korea and Thailand followed, with exports of 12,000 mt and 6,000 mt, accounting for 19% and 9%, respectively. On a MoM basis, except for a slight decrease of 3,000 mt in exports to Japan, exports to other regions all showed growth, particularly South Korea, which increased significantly by 9,000 mt MoM.

Overall, in May 2026, China's imports of unwrought aluminum alloy continued to pull back, falling to a new low in nearly five years; exports were strong, hitting a single-month record high and forming a clear divergence from imports.

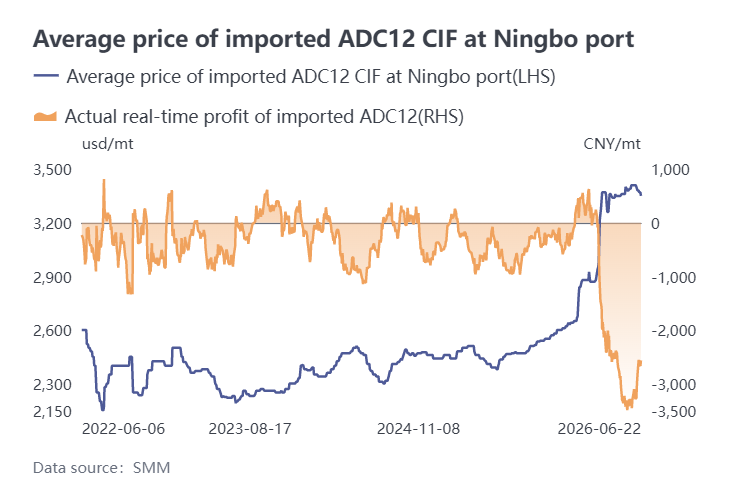

On the import side, affected by both soaring costs outside China and tightening domestic policies, the import profit of ADC12 underwent a sharp inversion before partially recovering. Since March, geopolitical tensions in the Middle East have continued to escalate, and the surge in LME aluminum prices coupled with logistical disruptions sharply pushed up ADC12 prices outside China, causing import profits to shrink rapidly and fall into losses. Entering April, the combination of high overseas prices and domestic weak adjustments exerted double pressure, widening the inversion further, with the loss per mt reaching as high as 3,500 yuan. A turnaround came in mid-May as tightening domestic tax invoice policies, raw material shortages, and expanding production cuts provided strong support for domestic ADC12 prices, driving the price center to steadily rise in June. Meanwhile, pressured by the decline in LME prices, ADC12 prices outside China fluctuated downward, with current quotes concentrated at $3,300-3,370/mt. As a result of these offsetting changes, the import loss per mt has narrowed to 2,500 yuan. Although the inversion pressure has eased somewhat, the absolute loss remains high, and June imports are expected to remain under pressure at a low level of around 60,000 mt.

On the export side, driven by both the supply gap outside China caused by geopolitical conflicts and the widened price spread between Chinese and overseas markets which opened an export profit window, China's exports of aluminum alloy to Japan, South Korea, Thailand and other destinations performed outstandingly, with both processing trade with imported materials and Ordinary Trade exports showing significant growth. However, as the price spread between Chinese and overseas markets has gradually narrowed recently, export profit margins are under pressure. Total exports in the short term are expected to remain at a relatively high level, but the absolute volume may face a slight pullback.