I. H1 2026 Aluminum Plate/Sheet, Strip and Foil Market Review

1. Supply-Demand Fundamentals

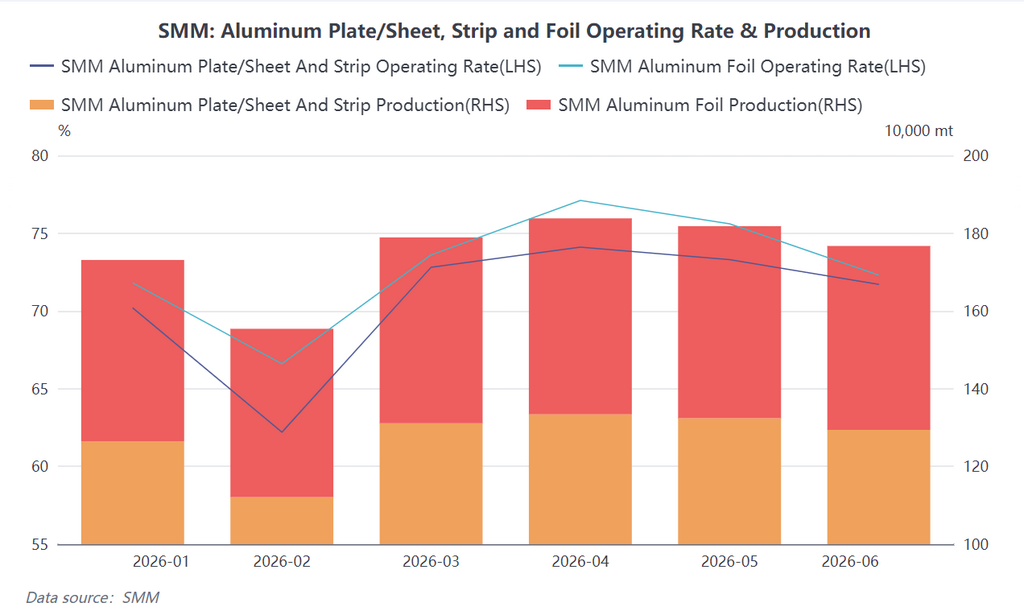

In H1, China's total aluminum plate/sheet, strip and foil production reached approximately 7.649 million mt, up 8.6% YoY; total aluminum foil production was about 2.848 million mt, up 5.8% YoY. The supply side clearly showed a dual-track recovery characterized by "domestic demand-led, external demand-driven" dynamics, broadly evolving through three stages:

Stage 1, January-February: Stronger-than-usual off-season, with environmental protection-driven production restrictions lifted and pre-holiday restocking providing weak support. The industry's operating rate unexpectedly rebounded in January, primarily driven by the resumption of production following the lifting of environmental protection-driven production restrictions in Henan. However, high aluminum prices significantly dampened the willingness of downstream users to stockpile centrally, with most end-users turning to purchasing as needed and shortening their restocking cycles. The Chinese New Year holiday led to a seasonal pullback in February's operating rates, with aluminum plate/sheet, strip and foil and aluminum foil falling to 62.2% and 66.6%, respectively. The supply recovery during this stage relied mainly on production resumptions in Henan and a few rigid restocking needs, showing limited sustainability.

Stage 2, March-April: Peak season materialized, with double-engine drive from can stock and energy storage pushing operating rates to highs. As the traditional peak consumption season arrived, end-use restocking demand was released centrally. Can stock packaging demand performed outstandingly, with its annual production growth rate expected to reach 8%, serving as the core support for plate/sheet, strip and foil operating rates. The booming energy storage sector drove order volumes for high-value-added products such as battery casings and brazing materials. On the aluminum foil side, demand for food packaging foil and pharmaceutical foil was robust, while battery foil achieved full production, benefiting from the surge in energy storage end-use demand. The operating rates for aluminum plate/sheet, strip and foil and aluminum foil hit their annual peaks in April, reaching 74.1% and 77.1%, respectively.

Stage 3, May-June: Domestic demand weakness gradually emerged, with export orders taking over as the core growth driver. Domestic demand divergence intensified entering May. Orders from traditional sectors, such as common plate for civil use and architectural curtain walls, weakened under the pressure of high aluminum prices. Although auto sheet showed a marginal recovery, automakers' "steel-aluminum substitution" plans had already planted hidden concerns. At this point, markets outside China became a key variable: benefiting from a global aluminum supply deficit and strong LME aluminum performance, export orders for Chinese enterprises increased significantly, with plate/sheet, strip and foil and aluminum foil export schedules generally extending into Q3. Strong exports effectively offset the pullback in domestic demand, but June operating rates still slipped to 71.7% and 72.3%, respectively, putting the overall industry on a "strong outside but weak inside" adjustment path. Demand side: Domestic and external demand structures diverged, with exports emerging as the biggest highlight. On the domestic demand side, can stock, energy storage, and NEV sheets & plates provided core support, while traditional construction and ordinary sheets & plates were notably suppressed by high prices, exhibiting "underperform in peak season" characteristics. On the external demand side, customs data showed that from January to May, cumulative exports of aluminum plate/sheet and strip rose 13.8% YoY, while cumulative aluminum foil exports were still down 4.6% YoY, even as monthly exports kept climbing. It is particularly worth noting that from March to May, plate/sheet and strip exports to the US surged due to order transfers caused by a fire at a leading North American plant, with monthly exports climbing from 15,000 mt to 37,000 mt, becoming the core source of short-term export growth. Meanwhile, although geopolitical conflicts in the Middle East briefly disrupted trade flows, backlog orders were released after detour shipping resumed. The phased boom in export markets effectively improved the supply-demand balance of the industry.

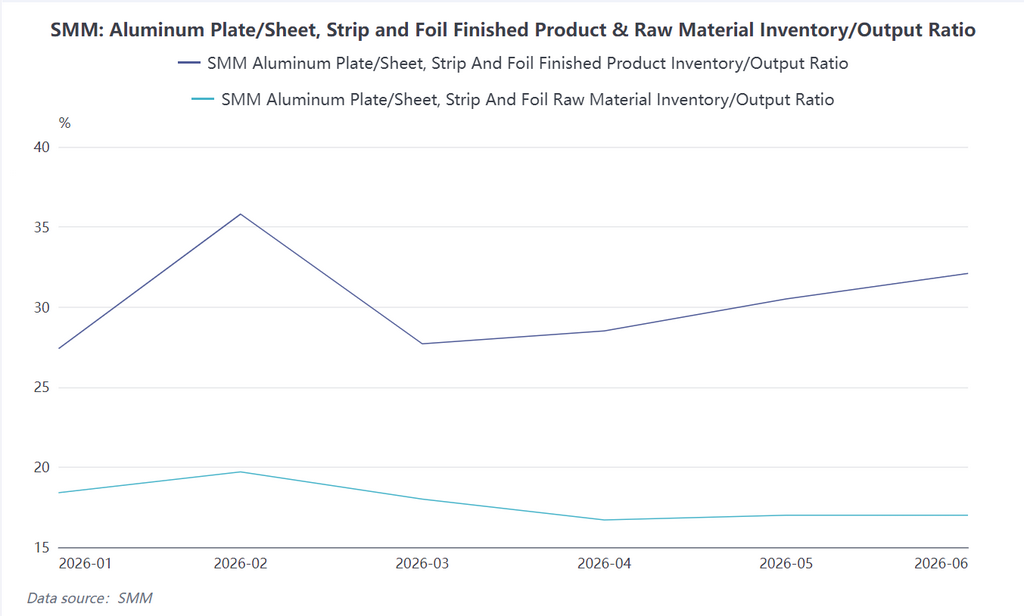

2. Inventory

Stockpiling for the Chinese New Year and production resumptions in January-February led to a rise in finished product inventories. In March-April, the peak season kicked off, accelerating destocking and returning inventories to normal levels. However, entering May-June, aluminum prices swung wildly at highs and a "rush to buy amid continuous price rise and hold back amid price downturn" mentality fermented among downstream players, weakening end-users' willingness to pick up goods and causing finished product inventories to accumulate again. In June, the finished product inventory/output ratio for aluminum plate/sheet, strip and foil rebounded to 32.1%, staying at a relatively high level for the year. At the same time, raw material inventories at end-user enterprises were generally low, as fear of high prices coexisted with just-in-time procurement, leading to pronounced structural divergence in inventory across the entire industry chain.

II. Outlook for the Aluminum Plate/Sheet, Strip and Foil Market in H2 2026

Supply side: Operating rates face downward pressure, and structural adjustment accelerates. Looking ahead to H2, the operating rate of the aluminum plate/sheet, strip and foil industry is expected to show a "stable first, then decline" trend. The cushion effect of external demand will persist in Q3, with limited downside room for operating rates supported by export orders. As the transferred order effect fades after North American plants resume production, overseas restocking cycles draw to a close, and the traditional domestic off-season arrives, downward pressure on operating rates will intensify significantly. Notably, changes in supply structure driven by the accelerating shift of double zero foil capacity to battery foil will tighten the supply-demand balance for packaging foil to a tight balance, keeping processing fees high. Meanwhile, air-conditioner foil will be constrained by sluggish property completions and high channel inventories, pushing the sector into a deep adjustment period with some capacities facing exit. In H2, operating rates for aluminum plate/sheet and strip are expected to range between 65% and 70%, and for aluminum foil between 67% and 72%.

Demand side: Export dividends gradually fade, while finding an anchor for domestic demand remains a challenging task. The export market faces a high-then-low pattern. In Q3, it will still be supported by the global aluminum supply deficit and long-term contracts signed earlier, keeping export schedules high. However, two variables loom: first, after the leading North American rolling plant resumes production, the transfer orders for can stock and automotive sheet taken on by China will significantly shrink starting July; second, the substantive impact of the EU CBAM carbon tariff and anti-dumping investigations against China in various regions will gradually unfold, driving up long-term compliance costs. On the domestic demand side, the energy storage sector remains the biggest source of certain growth. After the "630" grid connection deadline sprint, Q3 will see a brief breather, but global battery cell production for energy storage is expected to reach 1,033 GWh for the full year, providing sustained strong demand boost for battery cases, brazing materials, and battery foil. The can stock market faces a stockpiling lull before the implementation of the new national standard (effective in September), with can makers actively controlling inventories and upstream orders already showing signs of weakening. In the automotive sheet sector, the "steel-for-aluminum substitution" trend will accelerate in H2. The proportion of steel outer panels on low- and mid-end car models will rise, limiting room for aluminum sheet consumption growth. However, the NEV penetration rate exceeding 60% will provide a floor for high-end aluminum sheet demand.

H2 Supply-Demand Balance Summary:

In summary, the aluminum plate/sheet, strip and foil market will gradually shift from H1's "strong external demand and divergent domestic demand" to a rebalancing process in H2 2026 characterized by "waning external demand and domestic demand consolidating at lows." The contraction of transferred export orders will test the absorptive capacity of domestic demand. The can stock market, losing transfer orders and disrupted by the new national standard, faces a severe challenge in filling the demand gap in H2. Although energy storage consumption remains highly vibrant, it will be difficult to fully offset the demand slowdown in traditional sectors (home appliances, construction). The overall supply-demand pattern in H2 will loosen, operating rates will drop under pressure, and the industry will enter a cycle of active destocking. Aluminum price fluctuations will remain a core variable throughout the year. Against the backdrop of aluminum price premiums being given back and heightened expectations of decline, end-users' willingness to restock will remain suppressed. Industry profit margins are expected to stay low, and competition among enterprises will evolve deeply from "scale expansion" to "cost control and structural optimization."

![Approaching the Weekend, Prices Rise Again, Spot Aluminum Pressure Intensifies [SMM South China Spot Aluminum Daily Review]](https://imgqn.smm.cn/usercenter/VTjoW20251217171653.jpg)