TiO₂ Market Monthly Review: Cost Support Keeps Prices Stable, Overcapacity Pressure Persists

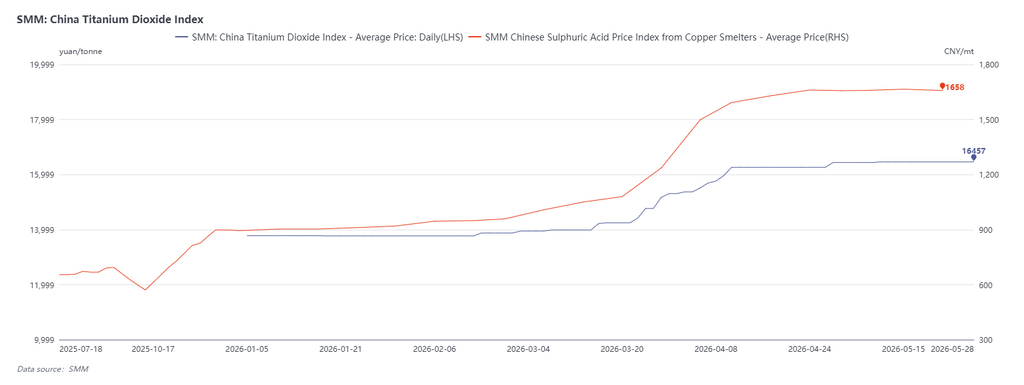

As of May 28, the China TiO₂ index stood at 16,457 yuan/mt, and the China copper smelting acid index was at 1,658 yuan/mt. Raw material sulphuric acid prices consolidated at highs, with some regions seeing slight price increases at month-end. Influenced by this, TiO₂ prices generally ran steadily in May, with some new orders already executed at April's new prices, as the market awaited price guidance from industry leaders at the beginning of next month.

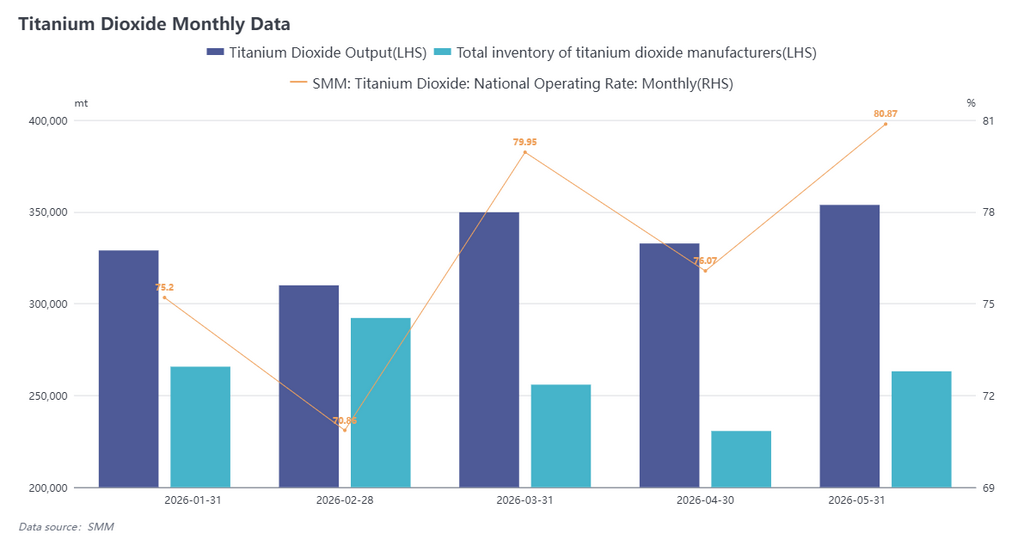

Production side, SMM data showed that China's TiO₂ production in May 2026 was 353,800 mt, up 6.31% MoM, with the industry operating rate reaching 80%; producer inventory was 263,000 mt, up 14.1% MoM. In May, TiO₂ operating rates stayed high, with chloride-process TiO₂ seeing robust supply and demand, and overall operations fluctuating at highs. However, approaching mid-month, domestic trade orders showed signs of weakness, with strong fear of high prices in the market. The current firmness in TiO₂ prices mainly relied on cost-side support.

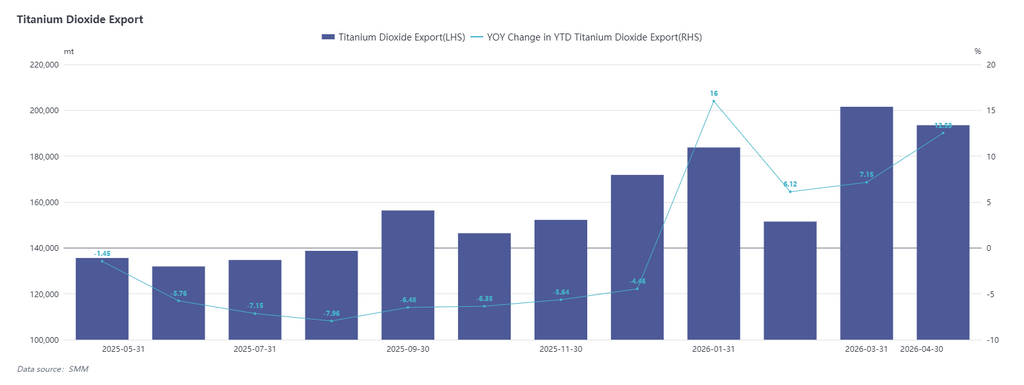

Export side, the TiO₂ export window continued to stay open in 2026, with cumulative exports from January to April reaching 730,000 mt, up 12.53% YoY. The foreign trade market provided strong support for TiO₂ prices.

Looking ahead, TiO₂ prices are expected to consolidate at highs in the short term. Driven by top-tier players and against the backdrop of prior loss pressure, enterprises' cost-based sentiment to hold prices firm remains strong. However, in the medium and long-term, capacity expansion has led to a notable market surplus, and future price trends will still depend on demand boosts from emerging sectors and continued broadening of foreign trade channels.

Titanium Sponge Monthly Review: Cost-Driven Mild Price Rebound, Supply-Demand Imbalance Unchanged

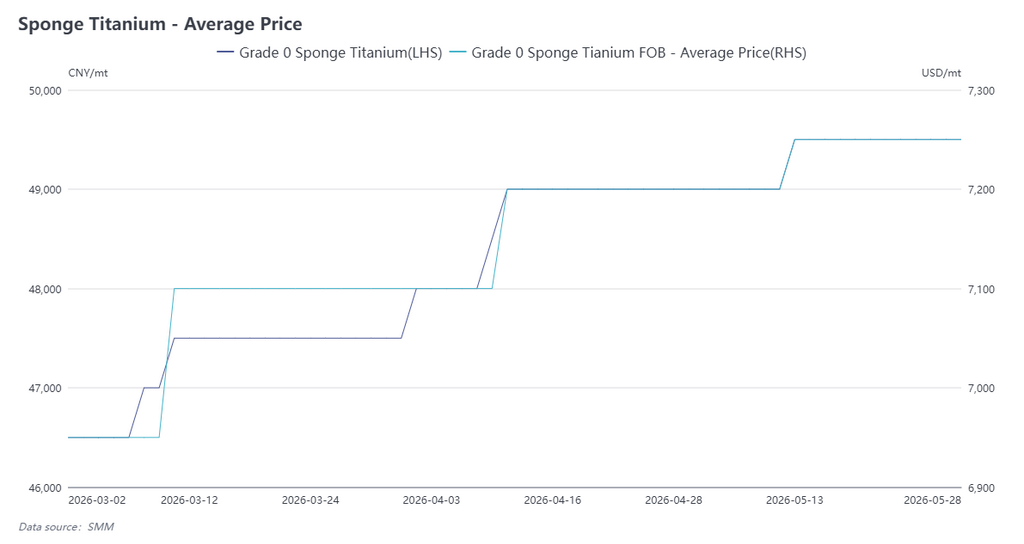

As of May 28, SMM Grade-0 titanium sponge was quoted at 48,000–51,000 yuan/mt, with FOB prices at $7,100–7,400/mt. Titanium sponge prices were slightly raised in May, mainly supported by the rise in cost-side magnesium ingot and titanium tetrachloride prices, with strong bottom support. Meanwhile, military order demand recovered slightly, but the civilian domestic trade market remained generally stable. In addition, titanium sponge enterprises had suffered consecutive severe losses, and top-tier players took the lead in adjusting prices to boost market sentiment. However, according to market feedback, the transmission of new prices to the titanium product end still faced certain resistance.

Production side, titanium sponge production in May 2026 was approximately 24,800 mt, up 10.75% YoY on a cumulative basis, with relatively small changes in production. However, overall capacity expansion this year has been significant, putting considerable pressure on enterprises. Combined with insufficient follow-up on new end-user project demand, the industry still faces an overcapacity situation. Export side, cumulative titanium sponge exports from January to April 2026 totaled 2,196 mt, down 11.27% YoY, with the foreign trade market contracting in tandem. Both domestic and foreign trade demand are in a weak phase.

Looking ahead, titanium sponge prices are unlikely to see wild swings in the short term. The future market still needs to rely on the implementation of new projects to create incremental demand and support the industry in emerging from its current difficulties.