SMM News, May 5:

During the May Day holiday in 2026, LME zinc traded in a general sideways range, finding solid support at the 40-day moving average. In terms of specific performance, LME zinc showed an N-shaped trend of rising first, then falling and rebounding again. On April 30, LME zinc extended its intraday upward momentum in the overnight session. After opening on May 1, it continued to rally by inertia and hit a high of USD 3,395 per tonne before turning lower quickly. At the opening of this week, LME zinc dipped to USD 3,306 per tonne and then moved higher again, recouping part of its losses. As of 16:00 on Tuesday (May 5), LME zinc closed at USD 3,360.5 per tonne, with trading volume dropping to 2,620 lots and open interest falling to 232,000 lots. In terms of inventory, LME zinc stocks stood at 96,250 tonnes as of this Tuesday, a decrease of 2,400 tonnes compared with April 30 before the holiday.

During the May Day holiday, Japanese authorities intervened in the foreign exchange market before the holiday, triggering a sharp decline in the US Dollar Index. Meanwhile, Iran submitted a new negotiation proposal to Pakistan, easing geopolitical tensions. Multiple positive factors jointly pushed LME zinc higher. However, Trump took a wavering attitude toward the Iran negotiation and announced tariff hikes on EU automobiles, driving a rebound of the US Dollar Index and putting downward pressure on LME zinc. Subsequently, the LME was closed on Monday this week due to the UK bank holiday. After the market reopened, macro uncertainty remained, while the continuous decline in zinc concentrate TC provided cost support for prices, lifting LME zinc to move up again.

Macroscopically, the lingering uncertainty over Middle East conflicts has pushed up energy costs and lifted market risk-aversion sentiment, providing indirect support to non-ferrous metal prices. Nevertheless, persistently high oil prices and elevated inflation have weighed on global economic growth expectations. Meanwhile, market expectations for Federal Reserve rate cuts keep getting delayed, which has capped the upside room of zinc prices at the macro level. Attention should be paid to ongoing macro uncertainties in the follow-up market.

Fundamentally, SMM estimates that China’s refined zinc output in May 2026 will drop by 1.6% month-on-month, yet rise by 4.5% year-on-year. According to pre-holiday inventory data, domestic social zinc inventories remain above 250,000 tons at a relatively high level, keeping domestic zinc ingot supply ample.

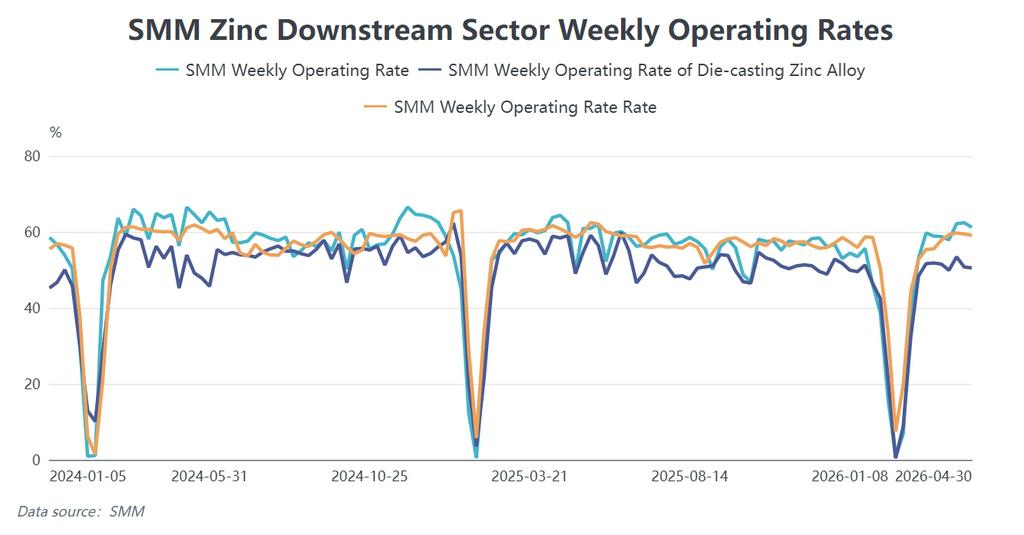

In terms of consumption, as of late April, domestic end-user consumption in galvanizing, die-casting and zinc oxide sectors all underperformed compared with the same period last year. The May Day holiday this year is longer than that of last year. Short-term ample zinc ingot supply and sluggish terminal consumption still place certain pressure on Shanghai zinc’s upside. It is necessary to keep an eye on the recovery of downstream consumption and changes in zinc ingot inventories after the holiday.

However, the continuous decline in domestic zinc concentrate treatment charges and the approaching opening of the export window offer bottom support and upward potential for zinc prices.

Overall, zinc prices are currently in a game phase intertwined with bullish and bearish factors. Mining-end costs and export expectations provide bottom support, while high inventory levels and sluggish consumption cap the upside space. Coupled with frequent disturbances from macro news, the short-term price trend will largely hinge on macro factors, as well as the pace of downstream restocking and the strength of inventory destocking after the holiday.