SMM, May 28, 2026:

1. Aluminum Semis Exports Overview

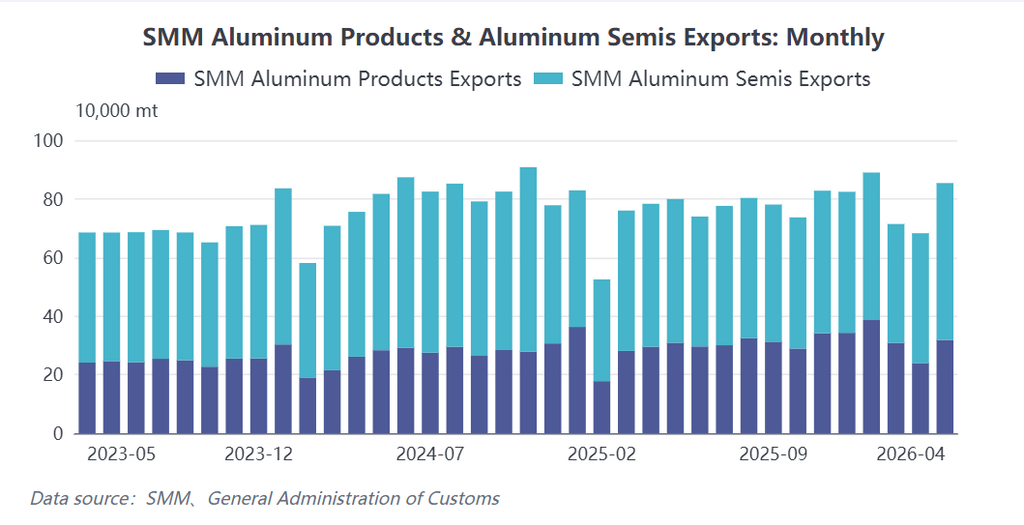

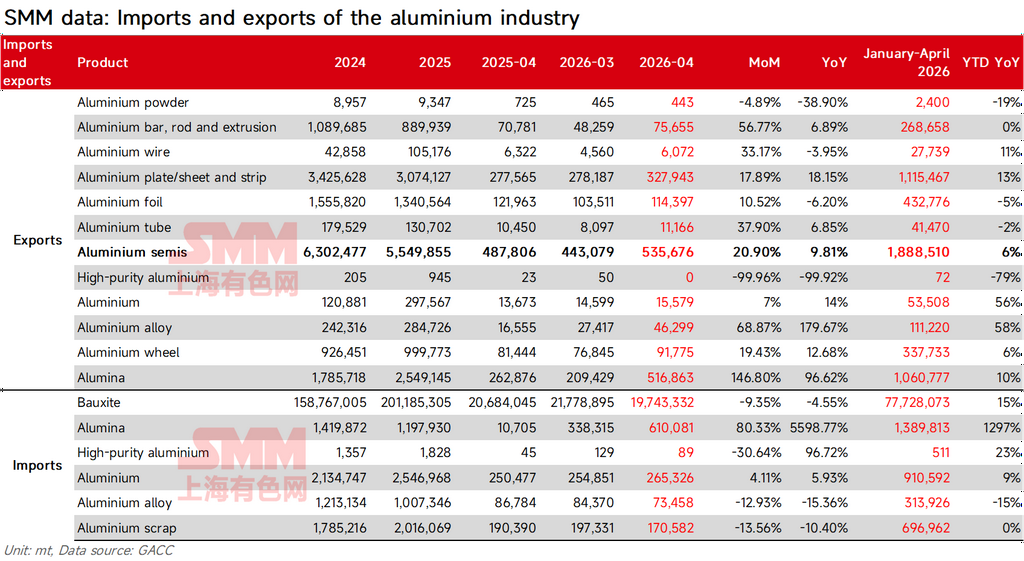

In April 2026, China's aluminum semis exports showed a strong rebound. According to customs data, April exports of aluminum semis (including aluminum extrusion, aluminum plate/sheet and strip, aluminum foil, etc.) reached 535,700 mt, up 20.9% MoM and up 9.8% YoY; exports of aluminum products (including aluminum wire, etc.) reached 318,000 mt, up 32.8% MoM and up 7.8% YoY. Cumulative aluminum semis exports from January to April totaled 1.1555 million mt, up 6.2% YoY cumulatively. Against the backdrop of global aluminum supply contracting due to geopolitical conflicts and a continuously widening price spread between domestic and overseas markets, China's aluminum semis exports are entering a phase of cyclical recovery.

2. Segment-by-Segment Analysis

Aluminum Wire: Pure Aluminum Stranded Wire Leading Growth, May Expected to Set New Record

In April, China's aluminum wire exports reached 27,580 mt, up 4.7% MoM and up 28.95% YoY. Notably, exports of pure aluminum stranded wire without steel core (tariff code 76149000) reached 15,500 mt, surging 94.5% MoM, with its share of total exports jumping from the normal range of 30%-40% to 56.4%. This directly reflected the surge in substitution demand for pure aluminum products following the widening of the price spread between domestic and overseas markets. In terms of destination, Southeast Asia (33.1%) and Africa (30.6%) were the main markets, with rigid demand from power grid construction supporting stable exports of aluminum conductor steel reinforced wire. Enterprise production schedules showed that pure aluminum stranded wire orders continued to increase in volume from May to July, and total aluminum wire exports in May are expected to surpass the single-month peak of the past five years.

Aluminum Extrusion: Middle East Orders Hit Bottom and Recovered, Demand Released in Latin America and Australasia

In April, aluminum extrusion exports reached 76,000 mt, up 56.8% MoM and returning to YoY growth of 6.9%, reversing the 32.8% YoY decline in March in one stroke. Guangdong Province, as the main production base (45% share), saw exports surge 124.4% MoM. In terms of export destinations, Southeast Asian countries such as Vietnam and Malaysia still dominated (22% combined), but Latin American countries such as Colombia, the Dominican Republic, and Chile rose to the 8th-10th positions, with a combined share of 8.7%, indicating steady release of construction extrusion demand in emerging markets. Although the Middle East showed some recovery (April exports of 769 mt, up 142% from 317 mt in March), the absolute volume accounted for only 1% of the total, far from returning to normal levels. Enterprises are actively going global to absorb surplus capacity through overseas joint-venture warehousing layouts in niche segments such as Central Asia, a trend that is clearly established.

Aluminum Plate/Sheet and Strip: Supported by Order Transfers from North American Fire, Middle East Recovery Still Shallow

In April, aluminum plate/sheet and strip exports reached 327,900 mt, up 18% MoM and up 18% YoY. Exports to the US remained at a high level of 34,800 mt (11% share), climbing month by month since October last year, mainly due to continued order transfers of can stock and automotive sheet following a fire at a leading North American plate/sheet and strip plant. The plant is expected to resume production in June, and transferred orders will continue to provide support until then. On the Middle East front, exports to the UAE rebounded from 1,580.9 mt in March to 6,029.2 mt in April, but surveys indicated that rerouting via the Red Sea was non-normalized transport behavior, and most clients had not yet resumed placing orders, with the overall recovery ratio remaining low. For the full year, if North American order stickiness continues and the Middle East gradually normalizes, full-year aluminum plate/sheet and strip exports are expected to reach 3.5 million mt; under conservative expectations, approximately 3.2 million mt.

Aluminum Foil: Export Rush Pushing Up Processing Fees, Geopolitical Persistence Determining Full-Year Upside

In April, aluminum foil exports reached 114,400 mt, up 10.5% MoM, but still down 6.2% YoY, with cumulative January-April exports down 5.4% YoY. The conversion of domestic double zero foil production lines to battery foil led to a contraction in traditional packaging foil supply. Coupled with clients' concerns over prolonged strait blockades prompting preemptive export rushes, domestic aluminum foil enterprises' export order production schedules have been extended to late July, with regular pouch processing fees surging to $1,000-1,200/mt. However, the current increase in aluminum foil exports is driven more by precautionary restocking rather than a recovery in end-use demand. China's aluminum foil exports to the UAE and Saudi Arabia showed some recovery, with exports to the UAE rebounding from 2,515 mt in March to 4,441 mt in April, and exports to Saudi Arabia from 4,868 mt to 6,387 mt, both still below normal levels. Under an optimistic scenario, if the strait blockade continues through Q3 and the export rush persists, the full-year total will reach 1.4 million mt; under a conservative scenario, if the blockade is lifted, leading to convergence of overseas market premiums and demand being front-loaded, the full-year total would be only 1.3 million mt. III.

3.H2 2026 Export Outlook and Full-Year Expectations

Currently, key aluminum semis export enterprises in China reported that orders for June-July maintained a growth trend, with some top-tier players seeing MoM growth of 15%-20%. However, the industry's overall production schedule has not yet recovered to the best levels of 2024. Ex-China, raw material inventory at semis processing enterprises was generally low. The backwardation structure in nearby LME aluminum prices suppressed stockpiling willingness, but rigid demand persisted in the construction, power, and electronics sectors. The core variables for H2 are: first, whether the production resumption of the leading North American flat-rolled products plant in June remains uncertain, and whether the stickiness of redirected orders can be sustained; second, whether tensions in the Strait of Hormuz will ease; and third, whether the price spread between domestic and overseas markets can maintain a widening trend. Overall, under the optimistic scenario, if rerouting shipments via the Middle East gradually becomes the norm, some North American orders are retained, and the price spread holds, aluminum semis exports are expected to increase to 600,000 mt in May and reach 670,000-680,000 mt in June, bringing full-year export volume to approximately 6.35 million mt, surpassing the 2024 level (approximately 6.3 million mt). Under the conservative scenario, if North American orders flow back after June, the Middle East recovery falls short of expectations, and the earlier export rush front-loads demand, full-year exports would be approximately 6 million mt, but still higher than 2025 (approximately 5.55 million mt). Regardless, the tone of recovery and rebound in China's aluminum semis exports in 2026 has been set. "Reclaiming the ground lost in 2025" is a high-probability event, and the pace of geopolitical conflict evolution and the sustainability of structural demand will be the core focus for subsequent tracking.

![[SMM Announcement] Announcement on the Classification Adjustment of Aluminum Semis Import Data in the SMM Database](https://imgqn.smm.cn/usercenter/DCsGU20251217171652.jpg)