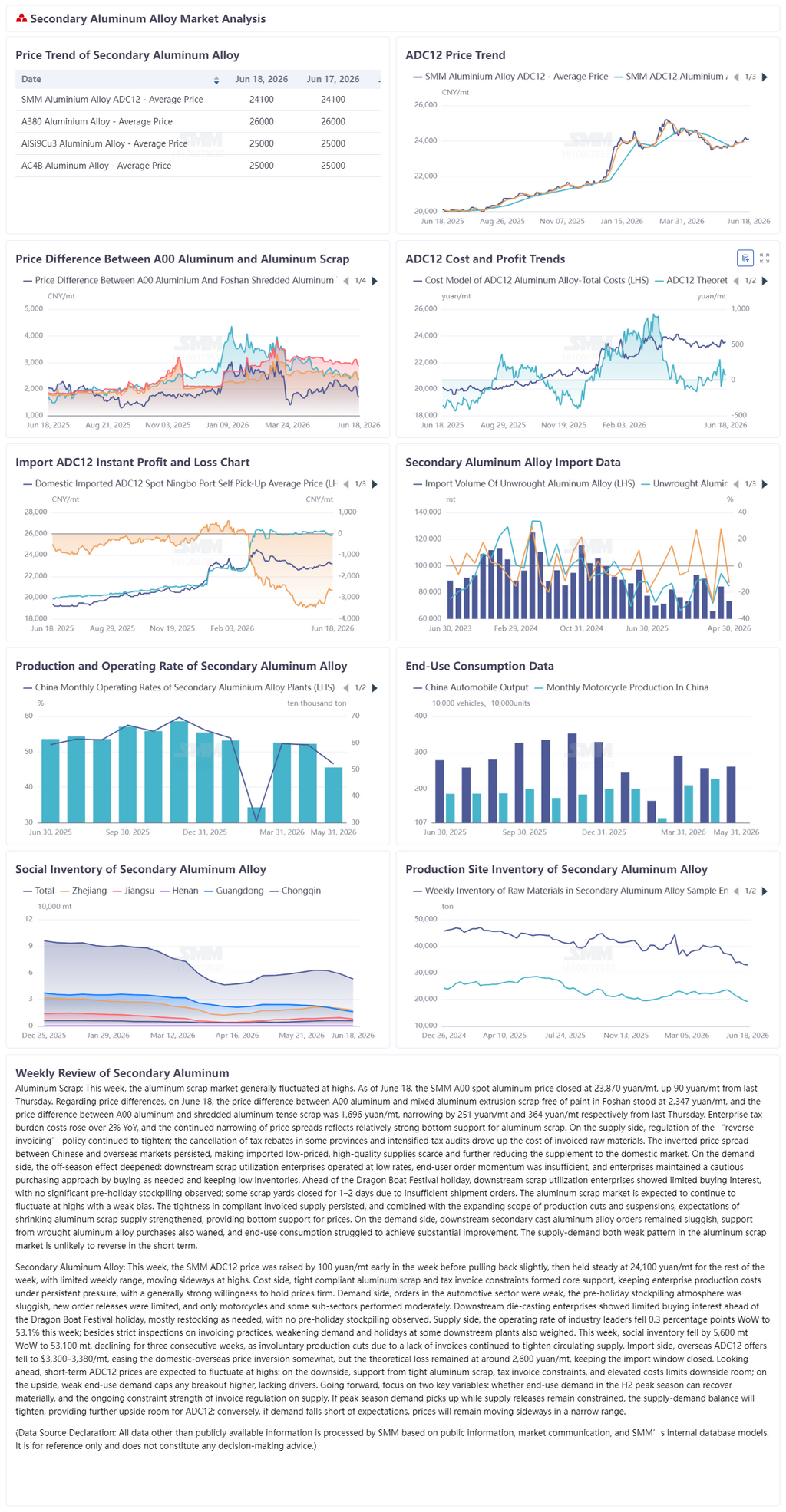

Aluminum scrap:

The aluminum scrap market mostly fluctuated at highs this week. As of June 18, SMM A00 spot aluminum closed at 23,870 yuan/mt, up 90 yuan/mt from last Thursday. Regarding price spreads, on June 18, the price difference between A00 aluminum and mixed aluminum extrusion scrap free of paint in Foshan was 2,347 yuan/mt, and the price difference between A00 aluminum and shredded aluminum tense scrap was 1,696 yuan/mt, narrowing by 251 yuan/mt and 364 yuan/mt, respectively, from last Thursday. Enterprise tax costs increased by over 2% compared to the same period last year. The continued narrowing of price spreads reflects strong bottom support for aluminum scrap. Supply side, the supervision of the “reverse invoicing” policy remained tight; cancelation of tax rebates in some provinces and intensified tax inspections drove up the cost of invoiced raw materials. The price spread between Chinese and overseas markets remained inverted, low-priced, high-quality imports were scarce, further weakening the supplement to the domestic market. Demand side, the off-season effect deepened. Downstream scrap utilization enterprises’ operating rates stayed low, end-user orders were sluggish, and enterprises maintained purchasing-as-needed and low-inventory strategies in a cautious buying atmosphere. As the Dragon Boat Festival holiday approached, downstream scrap utilization enterprises showed low purchasing willingness, no evident pre-holiday stockpiling was observed, and some yards closed for 1–2 days due to insufficient shipment orders. The aluminum scrap market is expected to continue its pattern of fluctuating at highs with a weak tone. Tight supply of compliant invoiced cargo persists, coupled with expanding production cuts and shutdowns, strengthening expectations of shrinking aluminum scrap supply and providing bottom support for prices. Demand side, downstream secondary cast aluminum alloy orders remained sluggish, purchasing support from wrought aluminum alloys also weakened, and end-use consumption was difficult to improve materially. The weak supply-demand pattern in the aluminum scrap market is hard to reverse in the short term.

Secondary aluminum alloy:

This week, the SMM ADC12 price was initially raised by 100 yuan/mt before pulling back slightly, then held steady at 24,100 yuan/mt for the rest of the week, with the overall weekly range narrow, presenting a pattern of moving sideways at highs. On the cost side, tight compliant aluminum scrap supply and tightness of tax invoices provided core support, keeping enterprises’ production costs under persistent pressure, and there was a generally strong willingness to hold prices firm. On the demand side, orders from the automotive sector were in the doldrums, pre‑holiday stockpiling sentiment was sluggish, new order releases were limited, and only the motorcycle sector and some niche segments showed moderate performance. Downstream die-casting enterprises showed limited purchasing willingness as the Dragon Boat Festival holiday approached, mostly restocking on an as‑needed basis, with no pre‑holiday stockpiling activity emerging.

On the supply side, the operating rate of industry leaders fell 0.3 percentage points WoW to 53.1%, with the decline attributable not only to strict crackdowns on invoice-related practices but also to weakening demand and holidays at some downstream plants. Social inventory fell 5,600 mt WoW to 53,100 mt this week, declining for three consecutive weeks, as passive production cuts caused by a shortage of invoices continued to tighten circulating supply. On the import side, overseas ADC12 offers dropped to $3,300–3,380/mt. The domestic‑overseas price inversion eased somewhat, but the theoretical loss remained at about 2,600 yuan/mt, and the import window stayed shut.

Looking ahead, ADC12 prices are expected to fluctuate at highs in the short term. On the downside, tight aluminum scrap supply, tax invoice constraints, and high costs underpin prices, leaving limited downside room. On the upside, weak end-use demand caps gains, providing little momentum for an upward breakout. Going forward, two key variables should be monitored closely: whether end‑use demand can recover substantially in the H2 peak season, and the extent of ongoing supply constraints from invoice regulation. If peak‑season demand materializes and supply releases are constrained, the supply‑demand balance will tighten, giving ADC12 further upside room. Conversely, if demand falls short of expectations, prices will remain range‑bound, moving sideways.

![[SMM Aluminum Flash News] Rising UK Aluminium Scrap Exports Raise Concerns Over Domestic Supply Security](https://imgqn.smm.cn/usercenter/LFPBA20251217171653.jpg)

![[SMM Aluminum Flash News] UK Scrap Aluminium Sector Needs 25% Annual Growth to Meet Future Demand](https://imgqn.smm.cn/usercenter/EVjRH20251217171653.jpg)