Around May 23, 2026, import and export data for cobalt and lithium battery industry chain-related products in April were released in a concentrated manner. Data showed that China's spodumene imports in April reached 758,000 mt in physical content, down 9.5% MoM and up 21.7% YoY. Lithium carbonate imports, China imported 32,650 mt of lithium carbonate in April, up 9% MoM and up 15% YoY....... SMM compiled the import and export data for battery materials, as detailed below:

Upstream

Lithium Concentrates

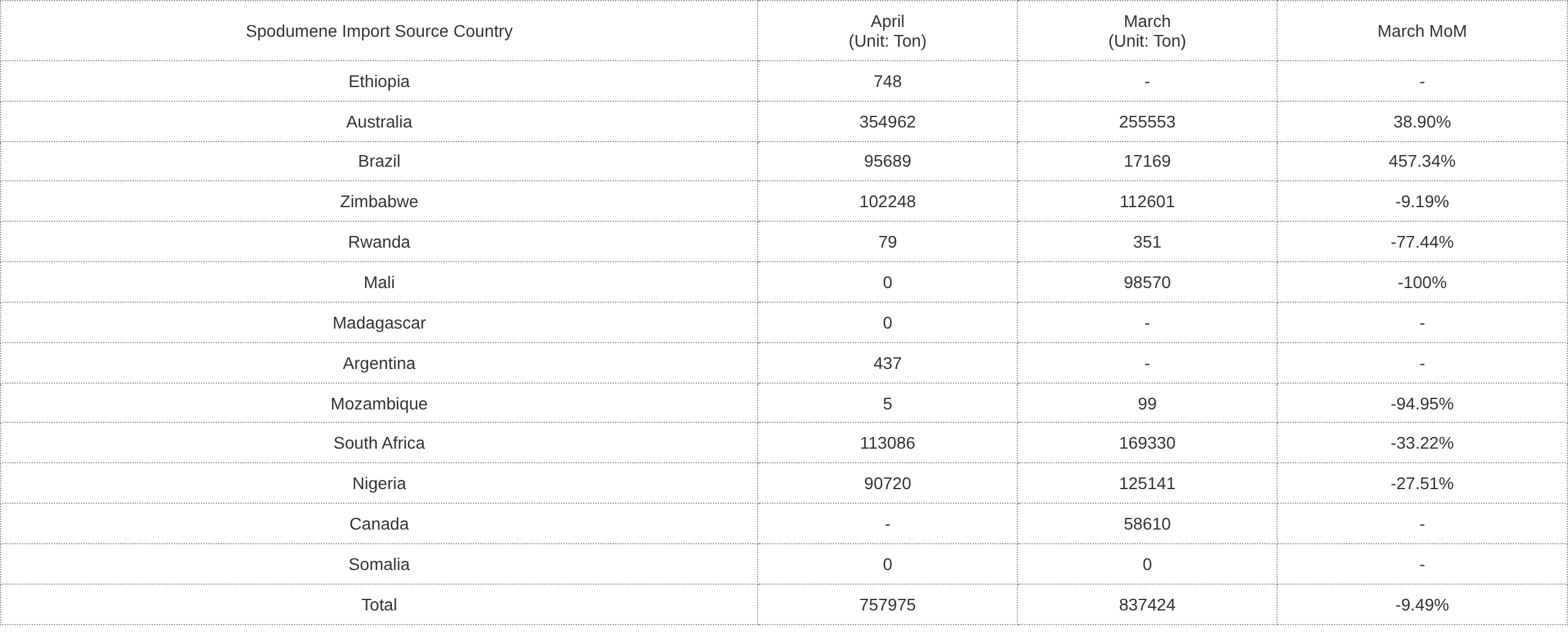

In April 2026, China's spodumene imports reached 758,000 mt in physical content, down 9.5% MoM and up 21.7% YoY, equivalent to approximately 63,000 mt of LCE. Customs data showed that April spodumene imports pulled back MoM from March, reaching 758,000 mt in physical content. By source country, Australian ore port arrivals returned to relatively normal levels, with over 350,000 mt arriving this month, up 38.9% MoM; Zimbabwe's earlier shipments arrived in the month at 102,000 mt, down 9.2% MoM; South Africa and Nigeria saw some contraction in monthly port arrivals, while ore from Mali had almost no notable port arrivals this month due to shipping schedule impacts. Notably, spodumene ore powder sold by Brazil in early 2026 arrived at ports this month, driving a significant increase in port arrivals from this country.

Additionally, after SMM screening, the month's incoming ore was equivalent to 63,000 mt of LCE. Among the incoming ore, lithium concentrates accounted for 67%, with the share edging down MoM, mainly because apart from Australia, ore from other source countries contained some relatively low-grade ore.

Source: China Customs, compiled by SMM

Spodumene concentrates (CIF China) spot pricing, according to SMM spot quotes, spot prices for spodumene concentrates (CIF China) fluctuated upward in April. As of April 30, the spot price for spodumene concentrates (CIF China) rose to $2,540/mt, up $221/mt from the month-end March price of $2,313/mt, a gain of 9.81%.

According to SMM, lithium carbonate prices continued to rise in April, and spodumene concentrates prices rose in tandem with salt prices, with gains exceeding those of lithium carbonate itself, causing non-integrated enterprises that purchased externally spodumene concentrates to suffer losses, with spot profitability remaining in deficit. In April, spot circulation of lepidolite concentrates relatively eased. Meanwhile, as lithium carbonate prices rose, processing fees for non-integrated enterprises also increased accordingly, preserving a certain profit margin for their processing operations and enabling these enterprises to achieve spot profitability.

However, recently, spodumene concentrates prices adjusted in tandem with lithium carbonate price fluctuations, and the price transaction center shifted downward. According to SMM's latest findings, disrupted by rumors of production resumptions at Jiangxi mines this week, lithium carbonate futures and spot prices declined, further dragging down the overall transaction center. Currently, lithium mines showed a weak willingness to make shipments, and transactions were mostly concentrated between traders and buyers. Port lithium ore inventory continued to decline.Going forward, attention should still be paid to the potential tight lithium ore supply triggered by high operating rates in the lithium chemicals industry, and lithium ore prices were expected to hold up well.

Lithium Carbonate

According to customs data, China imported 32,650 mt of lithium carbonate in April, up 9% MoM and 15% YoY. Of this, 21,000 mt was imported from Chile (65% of total imports), 9,555 mt from Argentina (29%), and 1,100 mt from Indonesia (3%). From January to April, China's cumulative lithium carbonate imports reached 116,000 mt, up 47% YoY cumulatively.

In April, China exported 370 mt of lithium carbonate, down 17% MoM and 50% YoY. From January to April, China's cumulative lithium carbonate exports totaled 1,886 mt, up 7% YoY cumulatively. In April, China imported 17,942 mt of lithium sulfate, up 9% MoM and 296% YoY. From January to April, China's cumulative lithium sulfate imports reached 58,900 mt, up 121% YoY cumulatively.

According to SMM spot quotes, spot lithium carbonate prices generally trended upward in April. As of April 30, the spot lithium carbonate price rose to 177,000 yuan/mt, up 14,000 yuan/mt or 8.59% from 163,000 yuan/mt on March 31.

According to SMM analysis, China's lithium carbonate prices followed a "V-shaped" trend of first declining then rising in April, with the monthly average price up 6% MoM. In the first ten days, geopolitical disruptions in the Middle East intensified global risk-aversion sentiment, causing non-ferrous metals and lithium carbonate prices to fluctuate downward. In the mid-to-late period, driven by Zimbabwe's export ban, Jiangxi mine license renewals, and rising costs, prices began to rebound and fluctuate upward, with the month-end price center shifting notably higher. Upstream and downstream purchasing remained stagnant, with the psychological price spread widening week by week. Upstream producers held prices firm and held back from selling, maintaining high offer prices; downstream buyers made just-in-time procurement only, with psychological price levels concentrated at 155,000-175,000 yuan/mt, restocking on dips only when prices fell rapidly. In April, battery-grade spot lithium carbonate prices dropped to around 155,500 yuan/mt in the first ten days, then rallied all the way to 177,000 yuan/mt by month-end.

As of May 29, domestic battery-grade spot lithium carbonate was quoted at 174,000-181,000 yuan/mt, with an average price of 177,500 yuan/mt.

Battery Materials

LiPF6

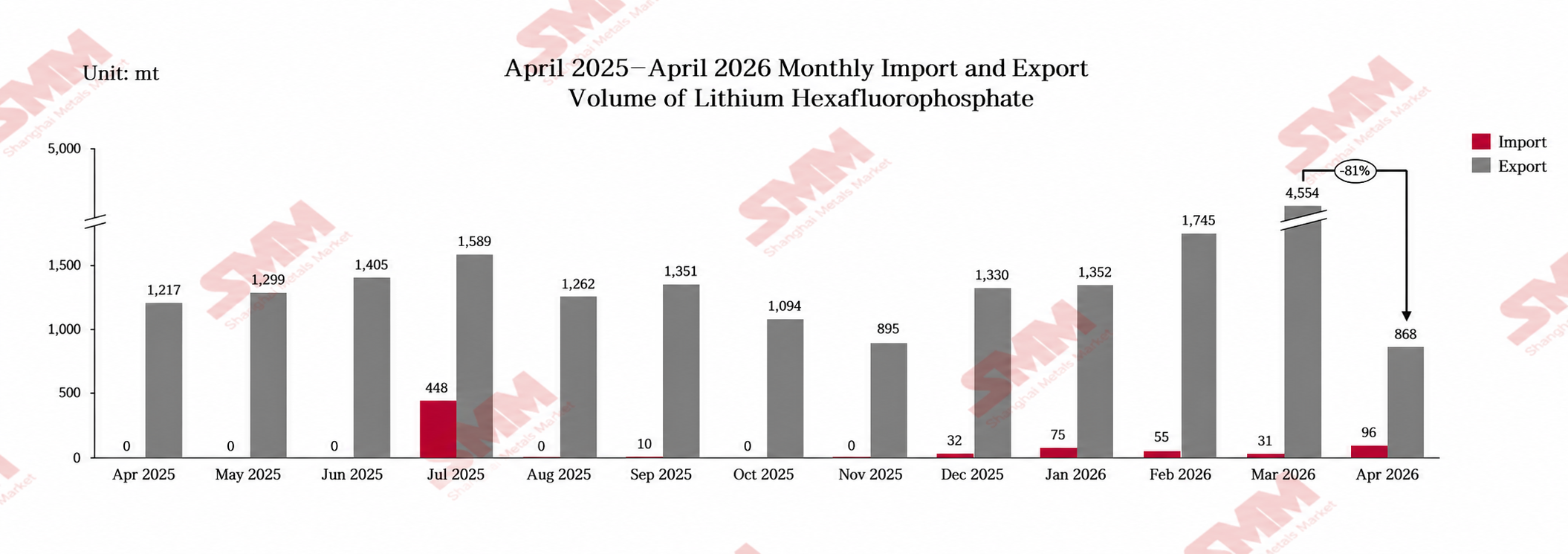

According to China Customs data, in April 2026, China's cumulative LiPF6 exports totaled approximately 868 mt, down approximately 80.9% MoM, while cumulative LiPF6 imports were approximately 96 mt.

Export side, China's LiPF6 exports in April 2026 were approximately 868 mt, down approximately 80.9% MoM from March and down approximately 33.2% YoY. Specifically, as the VAT rebate policy for LiPF6 exports was officially abolished starting April 1, 2026, enterprises rushed to export in March in advance, and ex-China electrolyte enterprises built up certain inventory, leading to MoM declines in China's exports to multiple major destination countries in April. Among them, exports to Poland were 337.5 mt (down approximately 80.4% MoM), South Korea 81.804 mt (down approximately 92.56% MoM), Czech Republic 150 mt (down approximately 67.43% MoM), and the US 101.908 mt (down approximately 61.7% MoM). Only exports to Japan saw an increase — exports to Japan were 191.37 mt, up approximately 50.77% MoM.

Artificial Graphite

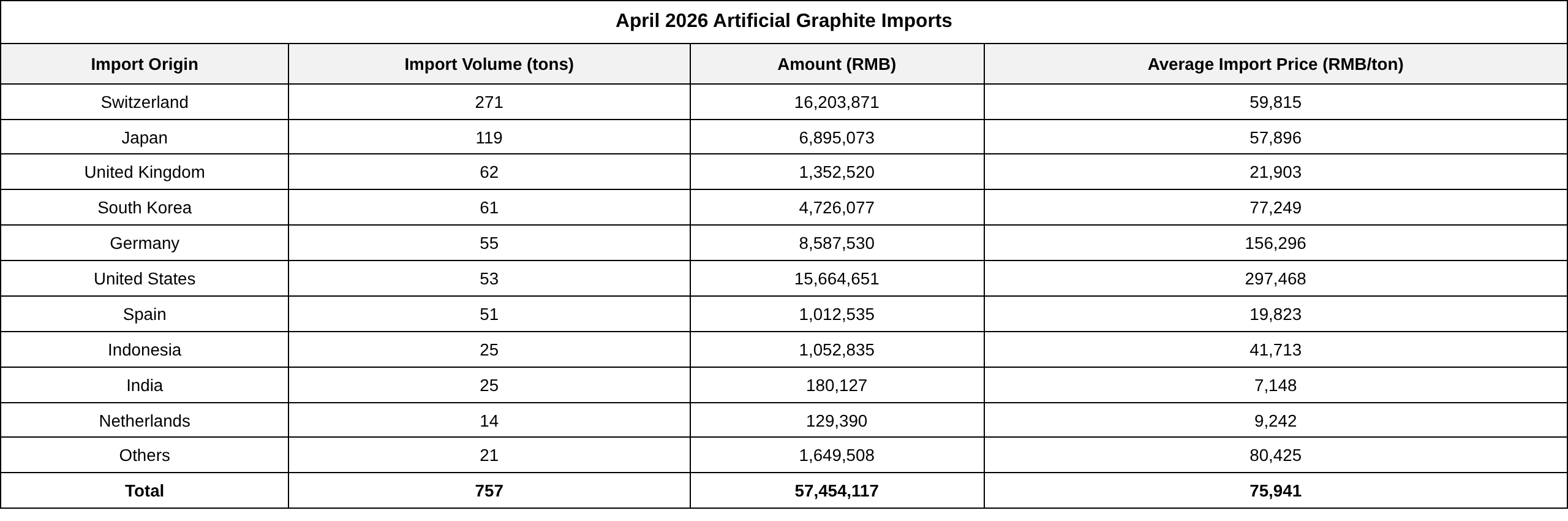

In April 2026, China's artificial graphite imports were 757 mt, up 12.4% MoM and down 32.9% YoY. Average import price side, in April 2026, the average import price of China's artificial graphite was 75,941 yuan/mt, up 23.1% MoM and up 14.6% YoY.

In April 2026, China's artificial graphite exports were 45,895 mt, up 22.3% MoM and down 21% YoY. Average export price side, in April 2026, the average export price of China's artificial graphite was 9,214 yuan/mt, down 6.6% MoM and up 0.26% YoY.

Exports from the top five provinces rose 21% MoM from the previous month, with two provinces seeing export growth exceeding 35% MoM and another province achieving a MoM increase of 20%.

Import market, downstream power battery enterprise orders in China gradually recovered in April. Combined with tight spot capacity at leading anode enterprises, restocking demand was released, boosting artificial graphite imports to rebound from weakness on a MoM basis. However, import volumes remained on a YoY decline, primarily because China's anode industry had ample overall capacity with supply still in a surplus pattern. Domestic self-sufficiency continued to strengthen, and the industry's reliance on imported raw materials and finished products steadily declined.

Flake Graphite

In April 2026, China's flake graphite imports were 3,178 mt, down 19% MoM and down 45% YoY.

Data source: China Customs, SMM

In April 2026, China's flake graphite exports totalled 4,093 mt, down 50% MoM and 54% YoY.

Export market, the official cancellation of the flake graphite export tax rebate policy this month directly squeezed the profit margins of foreign trade enterprises, significantly dampening overall export willingness across the market. Meanwhile, the approval pace for flake graphite export licences slowed down, hindering foreign trade shipment processes. Combined with weak ex-China end-use demand, multiple bearish factors converged to directly boost a sharp decline in industry export volumes.

The import market also continued to weaken. Goods originally destined for exports were redirected to the domestic sales market, making China's local supply increasingly abundant. Market enthusiasm for import procurement was insufficient, ultimately causing imports to decline in tandem this month.

Phosphate Ore

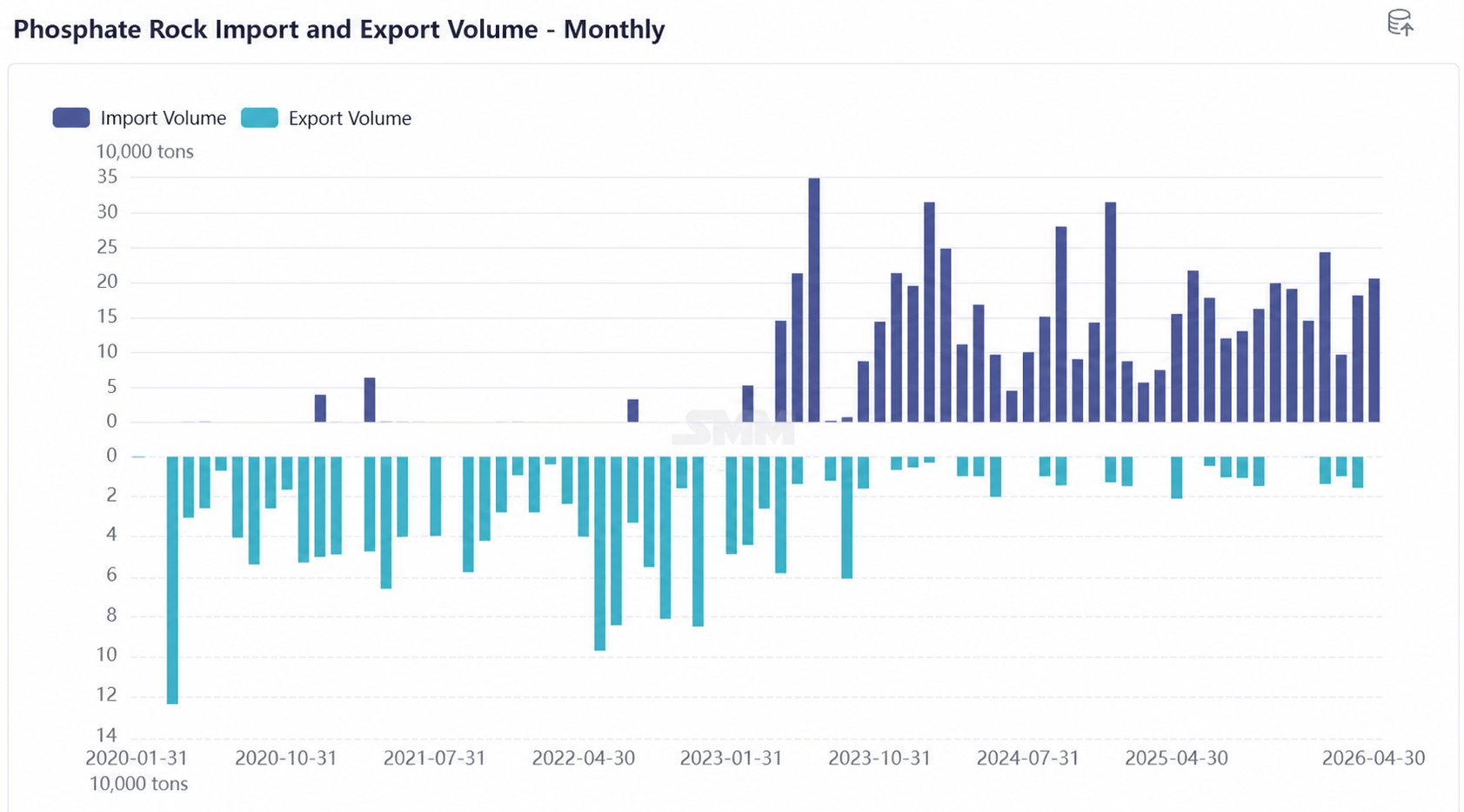

May 20, 2026, from customs data. In April 2026, China's phosphate ore imports were 207,000 mt. April imports rose 13.5% from 182,000 mt in March. The total import value in April was $19.741 million, up 35.7% MoM from $14.552 million in March. The average unit price was $95.5/mt, up 19.6% from $79.9/mt in March.

Import commentary: In May, Egypt's phosphate ore exports faced "policy tightening and weakening demand". On May 13, Egypt's Ministry of Petroleum and Mineral Resources announced it would no longer sign any new phosphate ore export contracts. Previously, Egyptian Prime Minister Mustafa Madbouly stated clearly at a meeting on May 10 that the government was pushing a transition from raw material exports to the manufacturing of high-value-added products such as phosphate fertiliser. Already signed long-term contracts would not be affected. This is expected to push up import prices and may affect import volumes going forward.

Cobalt

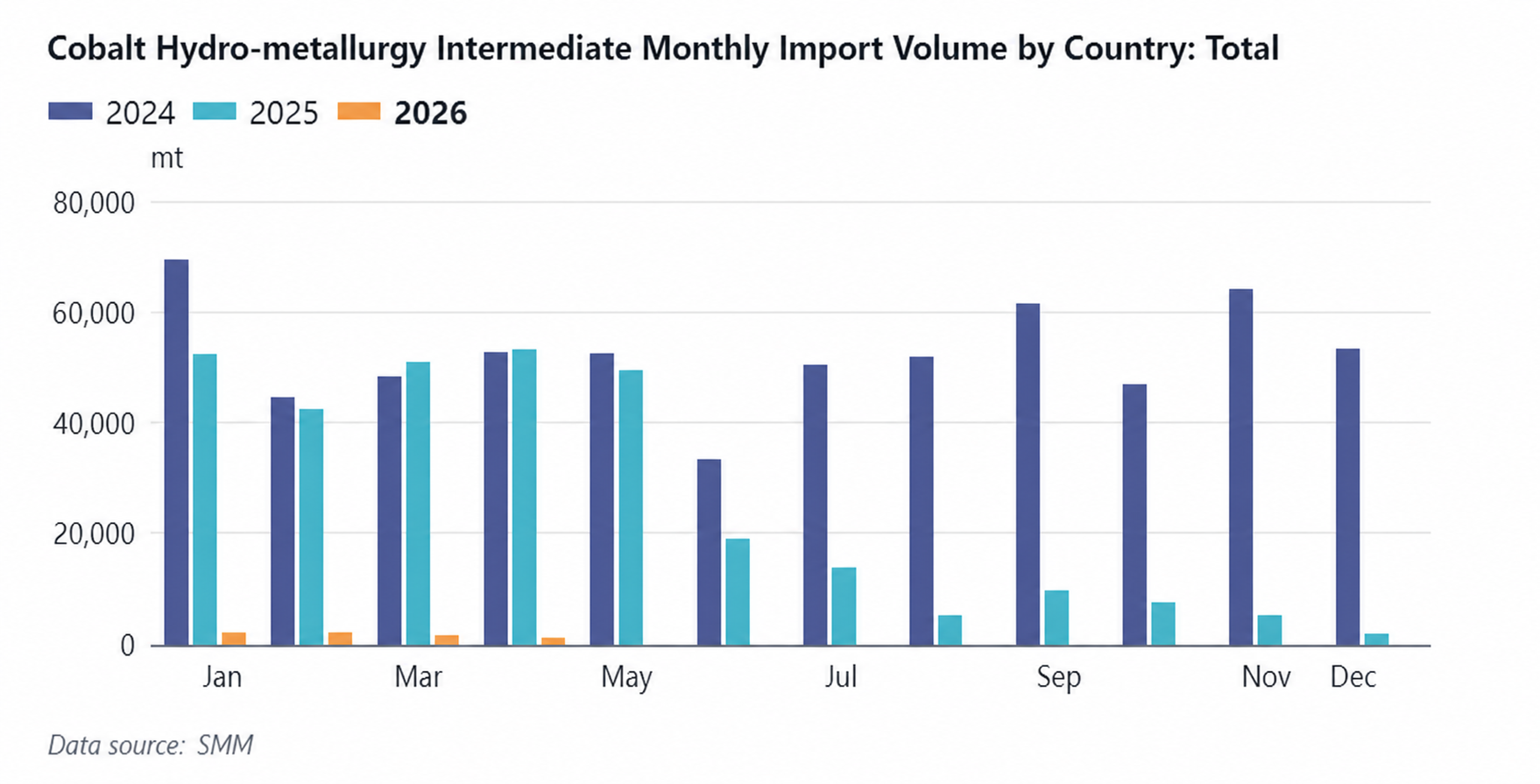

Cobalt Hydrometallurgy Intermediate Products

In April 2026, China's cobalt hydrometallurgy intermediate products imports were approximately 1,247 mt in physical content, down 26% MoM and 98% YoY. Of this, imports from the DRC were approximately 945 mt in physical content, down 43% MoM and 98% YoY. In April 2026, the average import price of China's cobalt hydrometallurgy intermediate products was $17,187/mt in physical content, up 2.63% MoM. It was reported that most miners had completed Q4 2025 quota approvals, but Q1 2026 quota approvals were again delayed due to issues with sampling, detection, and other procedural processes, resulting in lower approval efficiency. Additionally, DRC currently faced tight transportation capacity. For economic reasons, fleets prioritized transporting oil products and chemicals that were in short supply for production, followed by other metals with shorter turnover cycles, and cobalt among non-ferrous metals came last, meaning cobalt transportation capacity faced significant challenges. Constrained by the above factors, miners primarily focused on building in-transit inventory and had not yet concentrated on booking vessels, so the timing of large-scale intermediate product arrivals at ports was likely to continue being delayed.

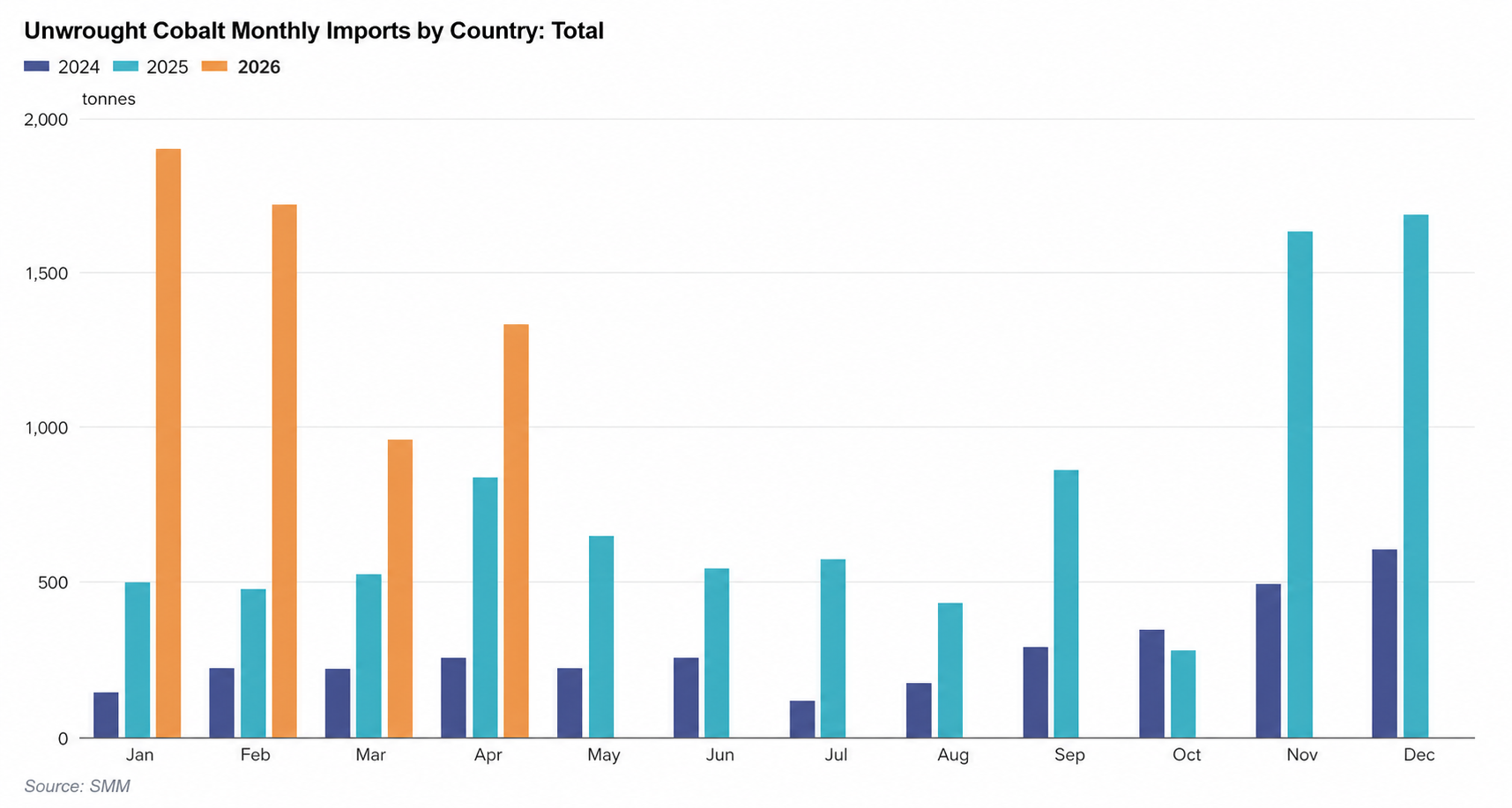

Unwrought Cobalt

China's unwrought cobalt imports in April 2026 were approximately 1,334 mt, up 39% MoM and up 59% YoY. In April, refined cobalt imports mainly came from Indonesia, Russia, and Madagascar, with imports of 462 mt, 457 mt, and 182 mt respectively. The main reason for the increase this month was that domestic smelters lacked intermediate product raw materials and imported cobalt slabs and cobalt briquettes for re-dissolution to ensure normal production. In terms of average import prices, the average import price of unwrought cobalt in China in April 2026 was $52,724/mt, up 4.72% MoM. Cumulative imports from January to April 2026 totaled 5,916 mt, up 153% YoY cumulatively.

Export side, China's unwrought cobalt exports in April 2026 were approximately 218 mt, down 47% MoM and down 95% YoY. By country, China's exports to the US dropped significantly, with April exports to the US at 35 mt, down 87.5% MoM. The main reason was that US alloy-grade refined cobalt demand pulled back in April, and ex-China branded refined cobalt was already sufficient to meet regional demand, with some refined cobalt traders redirecting destinations from the US back to China. In terms of average export prices, the average export price of unwrought cobalt in China in April 2026 was $54,590/mt, up 5.80% MoM. Cumulative exports from January to April 2026 totaled 1,792 mt, down 76% YoY cumulatively.

![Cobalt Products Prices Mostly Declined, Cobalt Salt Market Showed Mediocre Performance Overall — Where Is the Price Turning Point? [Weekly Review]](https://imgqn.smm.cn/usercenter/akEdZ20251217171728.jpg)