During the 2026 Labour Day holiday (May 1–5), the Chinese SHFE market was closed, and LME copper exhibited a fluctuating trend of initial decline followed by recovery. Before the holiday, SHFE copper 2605 contract closed at 100,970 yuan/mt, and LME copper closed at $13,019/mt on April 30. During the holiday, LME copper touched a high of $13,120/mt on May 1 before its center shifted downward, dipping to a low of $12,780/mt on May 4 before rebounding, and closed at $13,030/mt on May 5, edging up 0.64% from the previous day's opening.

I. On the Macro Front

During the Labour Day holiday when the Chinese market was closed, global macro developments, commodity markets, and ex-China policy dynamics continued to unfold. Multiple external factors drove a mild downward shift in the copper price center during the holiday. On one hand, expectations of US Fed policy tightening and geopolitical standoffs exerted downward pressure; on the other hand, tightening fundamentals provided floor support, resulting in copper prices moving sideways in the doldrums.

Geopolitical uncertainty persisted. On May 4, senior Islamic Revolutionary Guard Corps commander Yadollah Javani confirmed that Iran was controlling the Strait of Hormuz and that hostile vessels attempting forced passage would be dealt with decisively. On the same day, US President Trump refused to clarify whether the US-Iran ceasefire agreement remained in effect, only warning that Iran would be "completely destroyed" if it attacked US ships. The market thus judged that both sides had entered a standoff phase, with normal passage through the Strait of Hormuz unlikely to resume in the short term, and crude oil risk premiums remaining elevated. In this environment, wait-and-see sentiment was prevalent. LME copper dipped to the holiday low of $12,780/mt on May 4, then moved sideways around the $13,000/mt level, awaiting clarity on the geopolitical situation.

US Fed policy divergence intensified. The April rate-setting meeting kept interest rates unchanged, but internal dissenting votes reached four, the highest since October 1992. At the press conference, Powell acknowledged a lack of further progress on inflation but explicitly ruled out rate hikes, partially offsetting market concerns about escalating tightening. Meanwhile, US Q1 GDP annualized growth came in at 2.0%, a significant rebound from the prior reading of 0.5%, though consumer spending slowed; the April ISM Manufacturing PMI registered 52.7%, but the employment sub-index weakened. The overall picture presented "mild growth alongside rising inflation," with interest rate cut expectations for the year cooling, and copper prices continuing to face downward pressure as a result.

US-Europe trade friction escalated. On May 4, Trump announced that due to the EU's failure to honour the bilateral trade agreement already reached, the US would impose additional tariffs on automobiles and trucks imported from the EU next week, raising the rate to 25%. As a key end-use consumption segment downstream of the copper industry chain, the tariff hike will directly suppress European automobile exports and copper demand across the global automotive industry chain.

II. Fundamentals

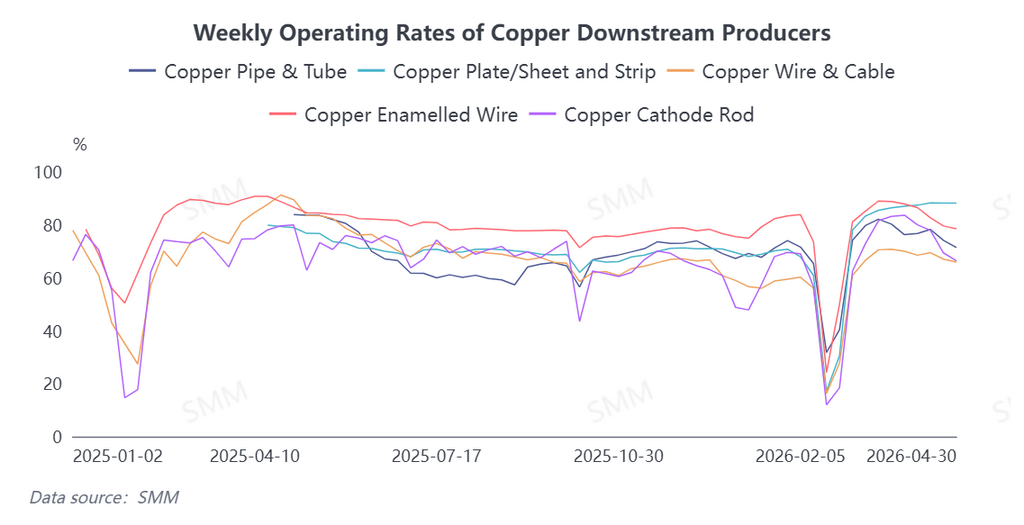

Supply side, both LME and COMEX were in Contango structure before the holiday, with inventories still at relatively high historical levels. However, social inventory in the Chinese market continued to decline, providing bottom support for copper prices. Demand side, according to SMM survey, downstream enterprises showed divergence in holiday arrangements. Copper cathode rod enterprises saw reduced new orders before the holiday, with mediocre stockpiling willingness and overall weak demand; the average Labour Day holiday duration this year was 1.33 days, up 0.16 days YoY. Most secondary copper rod enterprises that did not take holidays reported durations on par with 2025, but some enterprises that originally planned to take holidays adopted full production shutdowns this year to cope with fiscal and tax documentation challenges and raw material supply pressure. Wire and cable enterprises mostly continued the convention of previous years by maintaining production during the holiday, while some chose to halt production due to weakening orders to ease finished product inventory pressure. Affected by elevated copper prices, wire and cable enterprises adopted cautious on-demand procurement. Additionally, power grid orders declined due to earlier concentrated procurement having front-loaded some demand. Most enamelled wire enterprises conducted equipment maintenance based on order conditions, reducing overall operating loads; the number of enterprises choosing to shut down for the holiday due to persistently weakening orders increased notably YoY. End-use demand showed divergence: demand in energy storage, new energy and other sectors remained robust, the construction sector saw marginal recovery with the onset of the peak construction season, while demand in home appliance sectors such as air conditioning and the power grid sector is about to enter the off-season.

Looking ahead to May, the macro perspective remains focused on the direction of US-Iran tensions. Despite continuous negotiation signals being released, the Strait of Hormuz issue remains unresolved and market uncertainty persists. Meanwhile, continued attention should be paid to US economic data releases and their impact on market expectations for US Fed rate decisions. Fundamentals, consumption may enter the off-season in May. The trend of weakening orders and declining operating rates among downstream enterprises such as copper cathode rod and enamelled wire enterprises will be difficult to reverse in the short term. End-use consumption remains overall weak aside from structural bright spots such as new energy, and demand is expected to soften. However, it is worth noting that the supply side is expected to tighten. On one hand, the implementation of policies restricting sulphuric acid exports from China after May may exacerbate the sulphuric acid supply deficit outside China, thereby affecting hydrometallurgy smelting capacity. On the other hand, global smelters will also enter a concentrated maintenance period, and supply deficit concerns will provide bullish support for copper prices. Overall, copper prices are expected to have limited upside in the short term after the holiday, with attention on prior low-point support below.

![Inventory Inflection Point Emerged, Suppliers Held Back from Selling, Spot Premiums Rose [SMM Shanghai Spot Copper]](https://imgqn.smm.cn/usercenter/CYktX20251217171711.jpg)

![[SMM Flash] Middle East Official Sulfur Selling Prices Raised Significantly for May](https://imgqn.smm.cn/usercenter/kvwSZ20251217171710.jpg)