Abstract

The overseas secondary aluminum market experienced a "rise–stabilize–decline" pattern during the first half of 2026. Supported by stronger LME aluminum prices, escalating geopolitical tensions in the Middle East and tightening supply expectations, aluminum scrap and ADC12 prices climbed sharply during the second quarter. As logistics gradually normalized, geopolitical risk premiums gradually faded, LME prices weakened and downstream demand remained subdued, the market shifted back toward supply-demand fundamentals.

Beyond price movements, H1 2026 marked an important turning point in the global aluminum scrap market. A series of policy developments—including the UAE's temporary export restrictions on aluminum scrap, the EU's proposed 15% export tax on aluminum scrap and the U.S. HB9161 investigation into scrap exports—highlighted a growing global focus on resource security and domestic recycling. Aluminum scrap is increasingly being viewed not only as a traded commodity but also as a strategic resource supporting industrial competitiveness, decarbonization and supply chain resilience.

SMM expects the Southeast Asian secondary aluminum market to become increasingly demand-driven in H2 2026. While geopolitical developments and resource protection policies may continue to support premium-grade aluminum scrap and create short-term volatility, downstream demand recovery will remain the key factor determining ADC12 prices and the overall market trend.

1.0 Price Review

Supply Risks Drove Prices Higher as the Market Priced Expectations Rather Than Physical Shortages

The overseas secondary aluminum market experienced three distinct phases during the first half of 2026.

The first phase, spanning from the first quarter to early second quarter, was characterized by broad-based price gains across aluminum scrap and ADC12 markets. Supported by rising LME aluminum prices, escalating geopolitical tensions in the Middle East and growing concerns over supply chain disruptions, market participants increasingly priced in future supply risks rather than immediate physical shortages.

The second phase unfolded during the first half of the second quarter. As geopolitical tensions intensified, concerns over shipping through the Strait of Hormuz and the Red Sea increased significantly. Market participants became increasingly concerned not only about freight delays but also about the stability of aluminum scrap supply from the Middle East. At the same time, the UAE introduced temporary export restrictions covering selected industrial waste and metal scrap categories, reinforcing expectations of tighter availability for premium-grade aluminum scrap across Asia. As a result, aluminum scrap prices entered a period of rapid appreciation.

The third phase began in late June. As logistics gradually normalized and concerns over supply disruptions eased, the geopolitical risk premium embedded in aluminum prices started to unwind. Meanwhile, weakening LME aluminum prices and sluggish downstream demand pushed both ADC12 and aluminum scrap prices into a correction phase, bringing the market back to fundamental supply-demand dynamics.

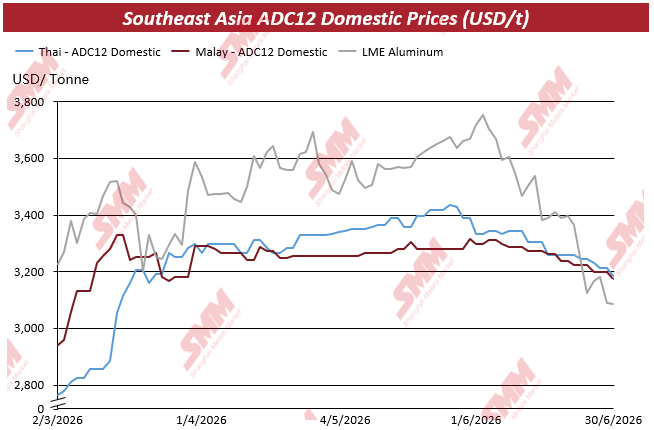

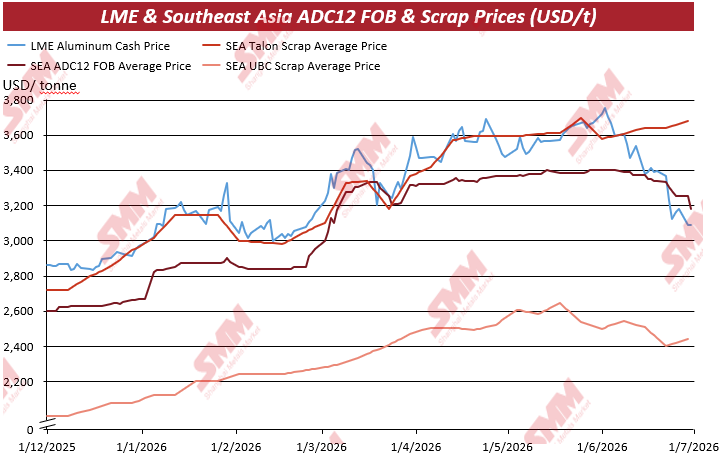

According to SMM's pricing assessment, LME aluminum remained the primary benchmark for the overseas secondary aluminum market throughout H1. Driven by supply concerns, the LME three-month aluminum price climbed from approximately US$3,156.5/mt at the end of February to above US$3,500/mt in early March. Although prices corrected temporarily afterwards, LME aluminum continued to fluctuate within the US$3,400–3,600/mt range during April and May, providing strong cost support for both ADC12 alloys and aluminum scrap across Southeast Asia.

Supported by stronger LME prices, ADC12 prices across Southeast Asia also moved higher. Domestic ADC12 prices in Thailand rose from below US$2,800/mt in early March to above US$3,400/mt by late June, while Malaysian domestic prices recovered from below US$3,000/mt to around US$3,300/mt. FOB quotations across the region followed a similar trend. Prices for Talon, Tense and UBC scrap all strengthened alongside ADC12, with premium-grade scrap outperforming finished alloys.

However, this rally was not driven by stronger downstream consumption. Instead, it reflected a market-wide reassessment of future supply availability.

According to SMM market surveys, traders were less concerned about whether material was immediately available than whether stable supplies could still be secured in the coming months. Against a backdrop of tightening supply expectations, many suppliers slowed spot sales in anticipation of higher prices, while downstream consumers accelerated purchases to secure premium-quality scrap. Consequently, prices for Talon and Tense increased more rapidly than those of ADC12.

Finished alloy producers faced a different situation. Although raw material costs rose significantly, producers were unable to fully pass higher costs downstream. For ADC12 producers, sustained price increases ultimately depended on whether die-casters, automotive component manufacturers and other end users were willing to accept higher quotations. As downstream orders failed to improve meaningfully, the market's ability to absorb higher costs remained limited.

This imbalance became increasingly evident during the second half of the second quarter.

Although prices for premium-grade scrap remained relatively firm, gains in ADC12 prices began to lose momentum. As Middle East logistics improved and supply concerns gradually eased, the geopolitical risk premium accumulated earlier in the year started to fade. At the same time, weaker LME aluminum prices further reduced cost support for overseas ADC12.

According to SMM assessments, FOB quotations for Southeast Asian ADC12 gradually retreated into the US$3,100–3,200/mt range after June, with some spot transactions approaching US$3,150/mt. In the scrap market, premium Talon remained comparatively resilient, while UBC and lower-grade scrap began correcting earlier.

This price movement clearly illustrates that the H1 rally was primarily driven by supply expectations rather than genuine improvements in downstream demand. Once supply risks eased, market pricing inevitably returned to consumption fundamentals, with end-user demand once again becoming the dominant factor influencing price direction.

2.0 Supply, Demand and Trade Flows

Trade Activity Normalized as Demand Replaced Supply Concerns

As supply disruptions gradually eased during the second quarter, the overseas secondary aluminum market entered a new phase of adjustment. Rather than experiencing an outright shortage of raw materials, the market was characterized by temporarily tight supply coupled with a slower-than-expected recovery in downstream demand. This imbalance gradually shifted pricing power away from supply concerns and back toward market fundamentals.

On the supply side, escalating geopolitical tensions in the Middle East and the UAE's temporary restrictions on aluminum scrap exports initially intensified concerns over the availability of premium-grade scrap. Many traders became increasingly reluctant to sell spot cargoes, while downstream consumers accelerated procurement to secure raw materials ahead of potential supply disruptions. Purchasing activity across Southeast Asia consequently strengthened during the first half of the second quarter.

However, as shipping conditions improved and logistics gradually returned to normal, supply expectations stabilized. The earlier concerns over prolonged disruptions began to fade, and market sentiment became noticeably more rational. At the same time, several scrap processors shifted their strategy from stockpiling to destocking in response to weakening price expectations, leading to improved spot availability across regional markets.

Demand, however, failed to recover at the same pace.

According to SMM market surveys, most ADC12 producers across Southeast Asia reported only modest improvements in orders from the automotive, die-casting and industrial manufacturing sectors. Purchasing strategies therefore remained conservative, with most manufacturers continuing to operate under just-in-time procurement and maintaining relatively low inventories. Few companies showed any willingness to rebuild raw material stocks despite earlier price increases.

Several market participants also indicated that higher scrap costs could not be fully transferred to downstream customers. As a result, actual transaction prices in many cases remained US$50–100/mt below prevailing market quotations, reflecting cautious buying sentiment and limited downstream acceptance of higher alloy prices.

Trade statistics further illustrate the shift in purchasing behaviour.

According to SMM data, ASEAN imported approximately 106,300 metric tons of aluminum scrap in April 2026, while exports totaled approximately 59,000 metric tons, resulting in net imports of roughly 47,300 metric tons. In May, imports increased to approximately 116,400 metric tons, while exports also rose to around 69,900 metric tons, leaving net imports broadly unchanged at approximately 46,500 metric tons.

Although gross imports expanded by more than 10,000 metric tons month on month, the corresponding increase in exports meant that net imports remained relatively stable. This suggests that higher import volumes were primarily absorbed by ongoing production requirements and normal trade circulation, rather than contributing to significant inventory accumulation across the region.

In other words, the market was replenishing material flow rather than inventories.

Price performance also began to diverge between premium aluminum scrap and finished secondary alloys.

Premium-grade scrap, including Talon and Tense, continued to benefit from concerns over resource availability and tightening policy support, allowing prices to remain comparatively resilient. ADC12, by contrast, is more directly exposed to end-use manufacturing demand. With orders from automotive and die-casting sectors recovering only gradually, alloy prices faced greater downward pressure as producers struggled to pass higher raw material costs through the supply chain.

By late Q2, the market had increasingly evolved into a pattern of "resilient raw material prices versus weaker finished alloy prices." This divergence significantly compressed margins for secondary aluminum producers, highlighting the growing disconnect between upstream raw material costs and downstream purchasing power.

Overall, H1 2026 represented a period of market rebalancing rather than outright supply shortages. Supply disruptions accelerated procurement during the early stages of the year, but slower demand recovery ultimately limited the sustainability of price gains. As geopolitical concerns gradually faded, purchasing behaviour, inventory management and regional trade flows all shifted back toward fundamentals, setting the stage for a more demand-driven market in the second half of 2026.

3.0 Resource Protection Is Reshaping Global Aluminum Scrap Trade

Policy Is Becoming a Structural Pricing Factor

While H1 price movements largely reflected the market's reassessment of supply risks, policy developments are beginning to reshape the long-term structure of global aluminum scrap trade.

As governments place greater emphasis on industrial resilience, decarbonization and circular economy strategies, aluminum scrap is increasingly being viewed as a strategic resource rather than merely a tradable commodity. The first half of 2026 saw a series of policy initiatives from major economies, all pointing toward the same direction: retaining more recyclable aluminum within domestic markets to support local manufacturing and strengthen supply chain security.

Among these developments, the UAE's temporary export restrictions had the most immediate impact on Asian buyers.

As one of the region's important suppliers of aluminum scrap, the UAE announced Ministerial Decision No. 105 of 2026, introducing a four-month temporary ban on exports of selected industrial waste and metal scrap, including several aluminum scrap products classified under HS7602. Existing international contracts could still apply for exemptions, but the announcement immediately heightened concerns over the availability of Middle Eastern scrap.

For import-dependent markets such as India, South Korea and parts of Southeast Asia, the policy reinforced expectations of tighter supply for premium-grade scrap. Buyers accelerated procurement plans, while suppliers became increasingly cautious in committing long-term volumes, contributing to stronger price support for high-quality material.

More importantly, the UAE policy should not be viewed as an isolated measure.

In recent years, the country has continued to strengthen its circular economy framework and industrial recycling strategy, encouraging more scrap to be processed domestically instead of being exported as raw material. As local secondary aluminum capacity expands, retaining higher-value recyclable resources within the country has become an increasingly important industrial objective. Consequently, future supply risks for Asian buyers may arise not only from logistics or geopolitical disruptions, but also from evolving resource management policies.

Europe is moving in a similar direction, albeit through different policy instruments.

Driven by the Clean Industrial Deal, circular economy initiatives and CBAM-related industrial strategies, the European Union has increasingly emphasized improving the availability of secondary raw materials for domestic manufacturers. SMM understands that the EU is proposing a 15% export tax on aluminum scrap, expected to take effect in September, with the objective of discouraging exports and prioritizing domestic recycling.

Should the proposal be implemented, it would increase the cost of sourcing European aluminum scrap for overseas buyers while reducing the competitiveness of European exports. Given Europe's role as a supplier of premium-grade scrap, Asian consumers may face higher procurement costs and intensified competition for alternative supply sources.

The United States is also sending an important policy signal.

Although the Secure Aluminum Supply Chains Act (HB9161) has not introduced any direct export restrictions, it requires an investigation into whether large-scale exports of aluminum scrap could undermine U.S. manufacturing competitiveness and supply chain security. The initiative reflects a broader shift in policy thinking: recycled aluminum is increasingly regarded as a strategic industrial resource supporting domestic manufacturing, rather than simply an export commodity.

Against the backdrop of reshoring initiatives, expanding electric vehicle production and continued investment in U.S. manufacturing, the strategic importance of aluminum scrap is expected to grow further. Even without immediate export controls, the legislation has already influenced market expectations, prompting participants to reassess the long-term availability of high-quality U.S. scrap.

Taken together, the UAE's export restrictions, the EU's proposed export tax and the U.S. supply chain review all point toward a common structural trend.

Rather than maximizing exports of recyclable materials, governments are increasingly prioritizing domestic value creation, industrial competitiveness and resource security. This marks a significant shift in the role of aluminum scrap within the global metals market.

For overseas secondary aluminum producers, the implications extend well beyond short-term price volatility. Future pricing will depend not only on LME movements and physical supply-demand balances, but increasingly on policy direction, regional trade flows and access to premium-grade scrap.

As global aluminum scrap trade becomes more regionalized, securing reliable long-term feedstock may become just as important as managing price risk itself.

4.0 H2 Outlook

Demand Will Drive Prices While Policy Shapes Costs

Looking ahead to the second half of 2026, the overseas secondary aluminum market is expected to enter a new phase in which downstream demand, rather than supply disruptions, becomes the dominant pricing driver.

The sharp supply concerns that characterized the first half of the year have gradually eased. Shipping conditions through the Middle East have improved, freight flows have become more stable, and spot availability has recovered compared with the peak of geopolitical tensions. At the same time, market conversations with scrap processors suggest that destocking is gradually replacing stockpiling as expectations shift toward a softer price environment. This does not imply that aluminum scrap has become abundant overnight, but rather that the market narrative is moving away from panic buying toward more selective procurement.

Despite improving availability, premium-grade aluminum scrap is unlikely to become structurally oversupplied.

Resource protection policies introduced by the UAE, the EU's proposed export tax and the ongoing policy discussions in the United States all suggest that governments are increasingly prioritizing domestic recycling and industrial competitiveness. These measures are expected to tighten the availability of premium-quality scrap over the longer term, even if short-term logistics continue to normalize. Consequently, high-quality scrap grades such as Talon, Tense and premium UBC are likely to remain relatively well supported compared with lower-grade materials.

Demand, however, is expected to remain the key variable throughout H2.

According to SMM market surveys, most secondary alloy producers across Southeast Asia continue to report cautious purchasing behaviour from downstream customers. Automotive production, die-casting activity and industrial manufacturing have yet to show a broad-based recovery, prompting buyers to maintain just-in-time procurement strategies rather than rebuilding inventories aggressively. Actual transaction volumes remain moderate, with many market participants expecting only a gradual improvement in consumption during the second half of the year.

Against this backdrop, LME aluminum is expected to remain the primary pricing benchmark for overseas secondary aluminum markets. Movements in LME prices will continue to influence ADC12 quotations and scrap valuations, particularly under the widely adopted pricing mechanism of LME plus conversion premium. However, unlike in the first half of the year, stronger LME prices alone are unlikely to trigger a sustained rally if downstream demand remains weak.

In the longer term, low-carbon manufacturing policies are expected to provide structural support for recycled aluminum demand. Although CBAM does not directly determine short-term price movements in Southeast Asia, it continues to reinforce the strategic importance of recycled aluminum within global supply chains. As automotive manufacturers and industrial consumers increasingly prioritize low-carbon materials, demand for secondary aluminum is expected to strengthen over time. Nevertheless, these structural drivers are unlikely to fully offset weaker short-term consumption during H2 2026.

Based on the current supply-demand balance and prevailing market sentiment, SMM expects Southeast Asian ADC12 FOB prices to fluctuate within the range of US$3,050–3,200/mt during H2 2026, with the market likely to remain range-bound. If LME aluminum continues to weaken, prices could test the lower end of the range. Conversely, any rebound driven solely by geopolitical developments is expected to be temporary unless accompanied by a meaningful improvement in downstream demand.

Looking ahead, several factors warrant close attention. These include the implementation of the EU's proposed aluminum scrap export tax, the progress of the U.S. HB9161 investigation, further developments in Middle East geopolitics, and the pace of recovery in Southeast Asia's automotive and die-casting industries. Together, these variables will determine not only price direction but also future trade flows and procurement strategies across the region.

Overall, the H2 market is expected to transition toward a demand-driven pricing environment in which policy increasingly shapes costs rather than short-term market sentiment. Geopolitical risks may still trigger temporary volatility, but without stronger downstream consumption, sustained price appreciation is likely to remain limited.

SMM View

SMM believes that the most significant development in the overseas secondary aluminum market during H1 2026 was not the correction in prices, but the shift in market pricing logic.

During the first half of the year, market participants initially priced in geopolitical risks, potential supply disruptions and tightening raw material availability. As these concerns gradually eased, pricing increasingly reflected actual downstream demand and purchasing activity. This transition marks a fundamental change in how overseas secondary aluminum markets are likely to behave going forward.

At the same time, aluminum scrap is undergoing a broader transformation within the global industrial landscape. Rather than being viewed solely as a tradable raw material, it is increasingly recognized as a strategic resource supporting manufacturing competitiveness, supply chain resilience and the transition toward a circular economy. Recent policy initiatives introduced by the UAE, the European Union and the United States all point toward the same long-term direction: strengthening domestic access to recyclable materials while reducing reliance on external supply.

In the short term, LME aluminum will continue to provide the primary pricing benchmark for overseas secondary aluminum markets, while downstream demand will determine the sustainability of any price recovery. Over the longer term, resource protection policies, regionalization of scrap trade and supply chain security are expected to become increasingly important structural pricing factors.

For market participants across the secondary aluminum value chain, future competitiveness will depend not only on managing price volatility but also on securing stable access to premium-grade scrap, diversifying procurement channels and building more resilient supply chains in an increasingly policy-driven global market.

![Geopolitical Conflicts Coupled with Inventory Destocking Drive SHFE and LME Aluminum to Drift Higher Short-Term [SMM Aluminum Morning Briefing]](https://imgqn.smm.cn/usercenter/yOYEC20251217171653.jpg)

![H1 auto production and sales fell YoY, ADC12 tug-of-war between sellers and buyers moved sideways [SMM cast aluminum alloy morning comment]](https://imgqn.smm.cn/usercenter/DCsGU20251217171652.jpg)