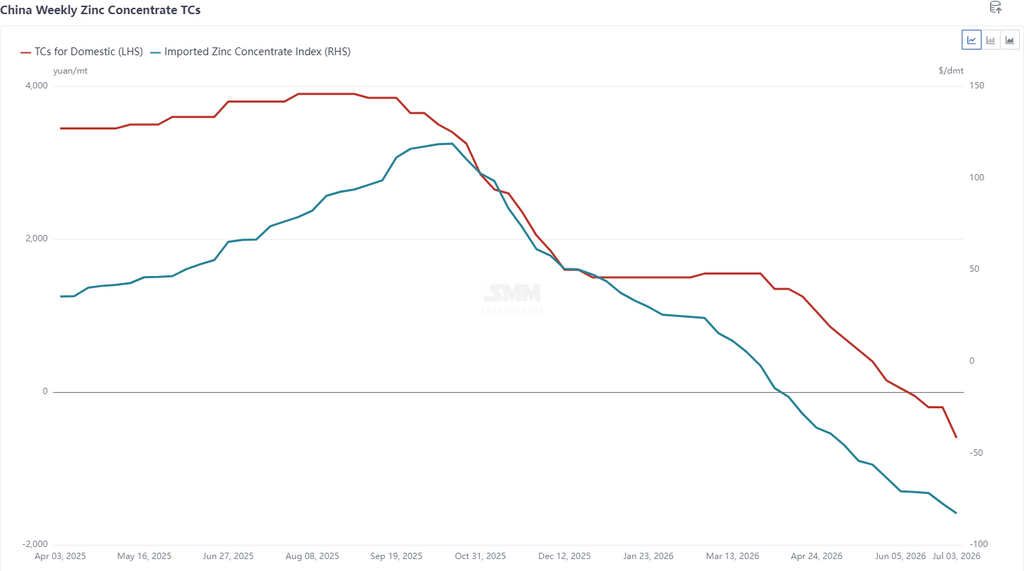

In H1 2026, the refined zinc industry struggled under multiple pressures. Ore supply remained tight, with both domestic and imported zinc concentrate TCs falling to record lows since data records began in 2013, directly squeezing smelter profits, and some enterprises have already fallen into losses. How will the refined zinc market develop in H2?

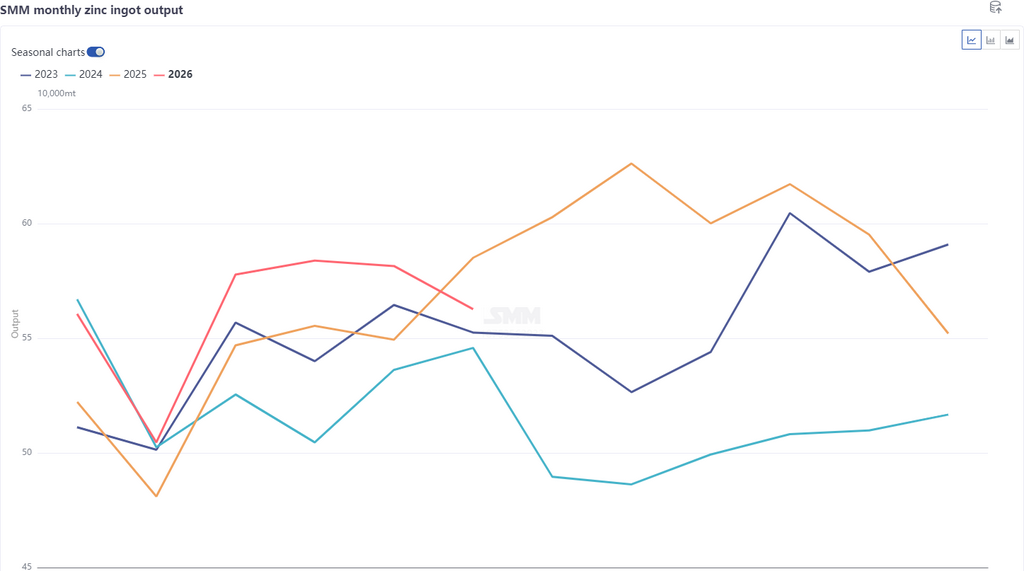

Reviewing H1, domestic zinc concentrate TCs fell to -600 yuan/mt in metal content, while imported TCs dropped to a historic low of -$82.83/dmt. Raw material shortages constrained smelters' production release. As of June, SMM's cumulative refined zinc production exceeded 3.37 million mt, up 130,000 mt YoY, below expectations.

In H2, from a profit perspective, although high sulphuric acid and minor metal prices provide support, TCs have hit new lows. Currently, some smelters are incurring losses after comprehensive recovery. According to SMM calculations, smelters using domestic ore incur an overall loss of around 300 yuan/mt after deducting full costs. For smelters using a mix of 40% imported ore and 60% domestic ore, the overall loss after deducting full costs is around 1,000 yuan/mt. However, on a cash-cost basis, smelters' loss margins narrow. Those with strong comprehensive recovery still retain a small profit. Furthermore, based on SMM's cost-profit model estimates, the profit center of smelting relies heavily on by-products—the revenue contribution share of sulphuric acid and minor metals has climbed above 81%, rendering TC income almost nominal. If TCs stop falling and sulphuric acid prices stay high going forward, the likelihood of smelting losses widening further is low; from a profit standpoint, the probability of production declining after concentrated H2 maintenance is limited, with full-year growth still expected to be nearly 100,000 mt.

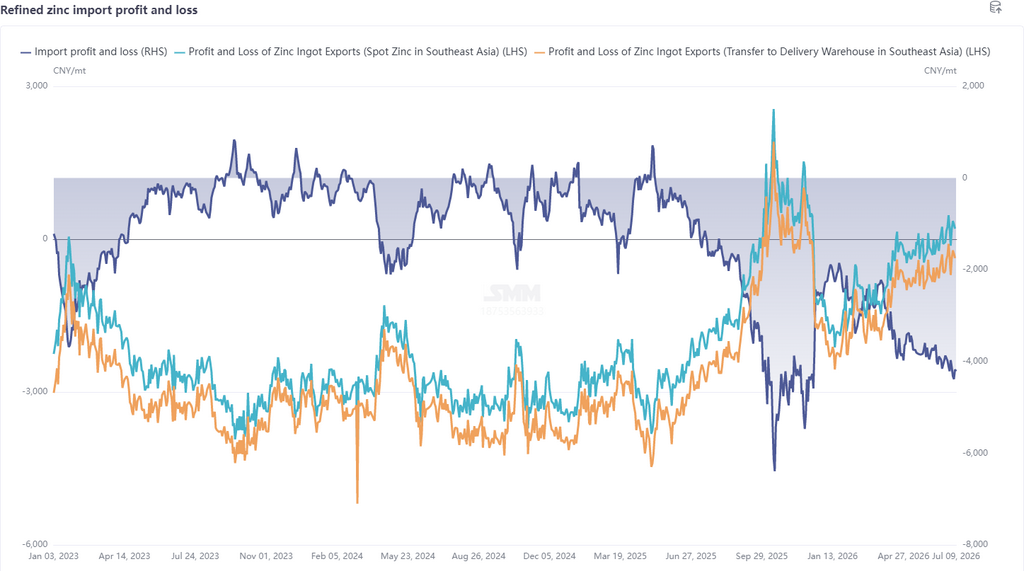

Additionally, from a price perspective, the price spread between Chinese and overseas markets is significant: inventories diverged, with China's social inventory breaking 260,000 mt to a three-year high, while LME inventory stood at only about 100,000 mt, a relatively low level. Coupled with overseas production disruptions, the overseas market outperforms the domestic market, keeping the SHFE/LME price ratio low. The spot export window for zinc ingots to Southeast Asia has already opened, and the window for shipping to delivery warehouses is expected to have further chances to open in Q3. In H2, key focuses include the periodic production constraints from concentrated smelter maintenance, the marginal support of sulphuric acid price resilience on profits, and whether the export window can remain open to adjust the supply-demand mismatch between domestic and overseas markets. Arbitrage suggestions: focus on domestic calendar spreads, and consider cross-market reverse arbitrage when the export window opens.