SMM, July 9:

In H1 2026, the PV glass industry completed a full downward cycle of oversupply, weakening demand, prices hitting bottom, industry-wide losses, and accelerated capacity rationalization through cold repairs. Three factors—a phased pullback in China's new installations, declining demand after the export tax rebate removal, and the release of earlier expanded capacity—drove the PV glass industry back into a downward trajectory, accelerating the pace of capacity rationalization.

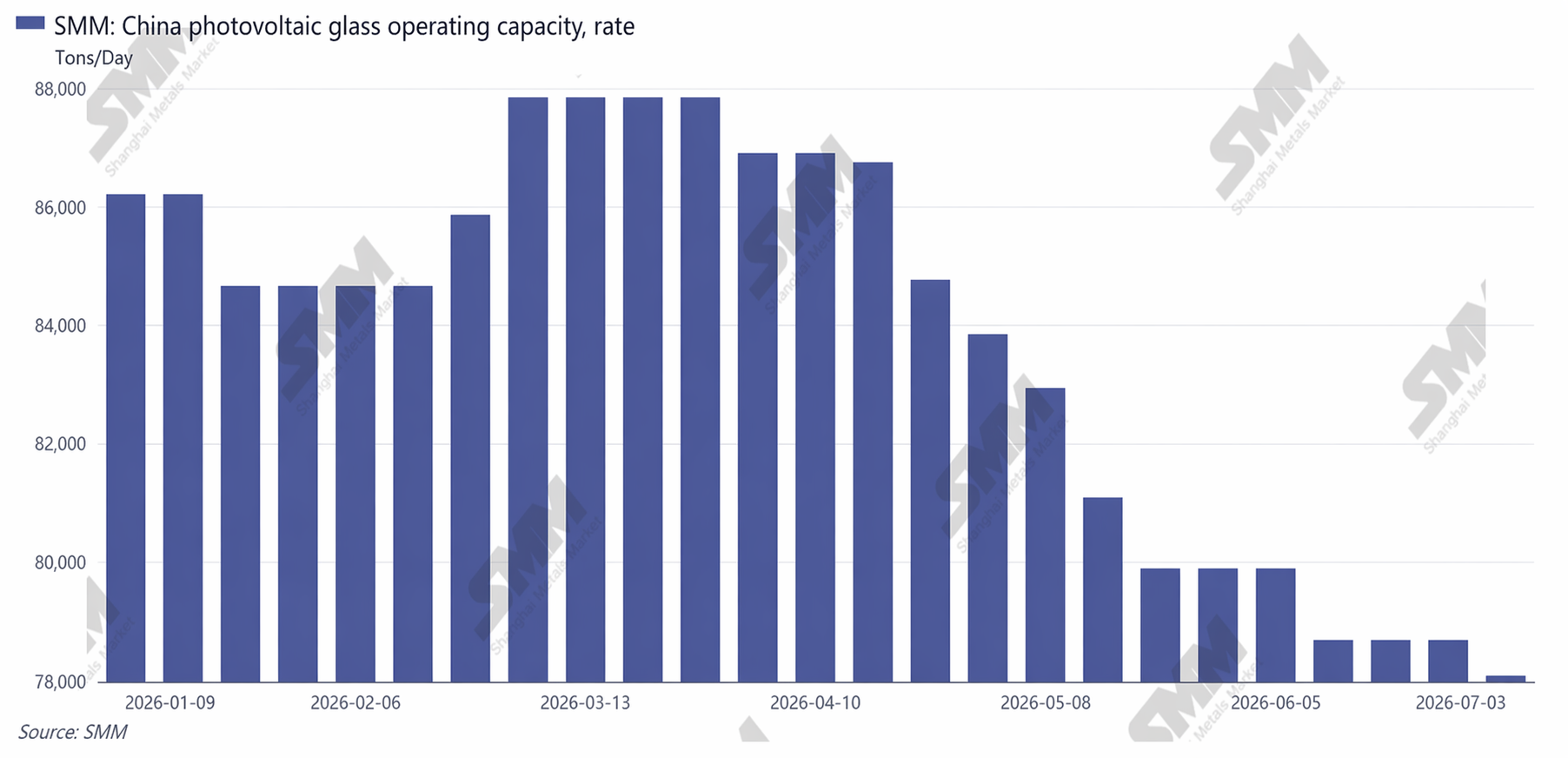

Supply Side: Operating Rate Contracted Continuously; Cold Repairs Became the Industry's Only Destocking Measure

In H1 2026, China's total daily melting capacity of PV glass stayed high. At the start of the year, the industry's operating daily melting capacity reached 86,210 mt/day, theoretically matching 47 GW/month of module demand. Top-tier players ignited and started production at kilns, while some second- and third-tier glass production lines that had started production earlier began capacity ramp-up, continuously increasing China's supply. However, due to the continuous operation requirements of kilns and their high start-stop costs, enterprises initially chose to cut production by plugging outlets rather than cold repairs.

After the export tax rebate was canceled, module enterprises' production schedules declined sharply, and glass purchases contracted significantly, leading to a very severe oversupply of glass. Enterprises began cutting production, and China's operating daily melting capacity dropped to 78,685 mt/day in June.

China's PV Glass Operating Capacity

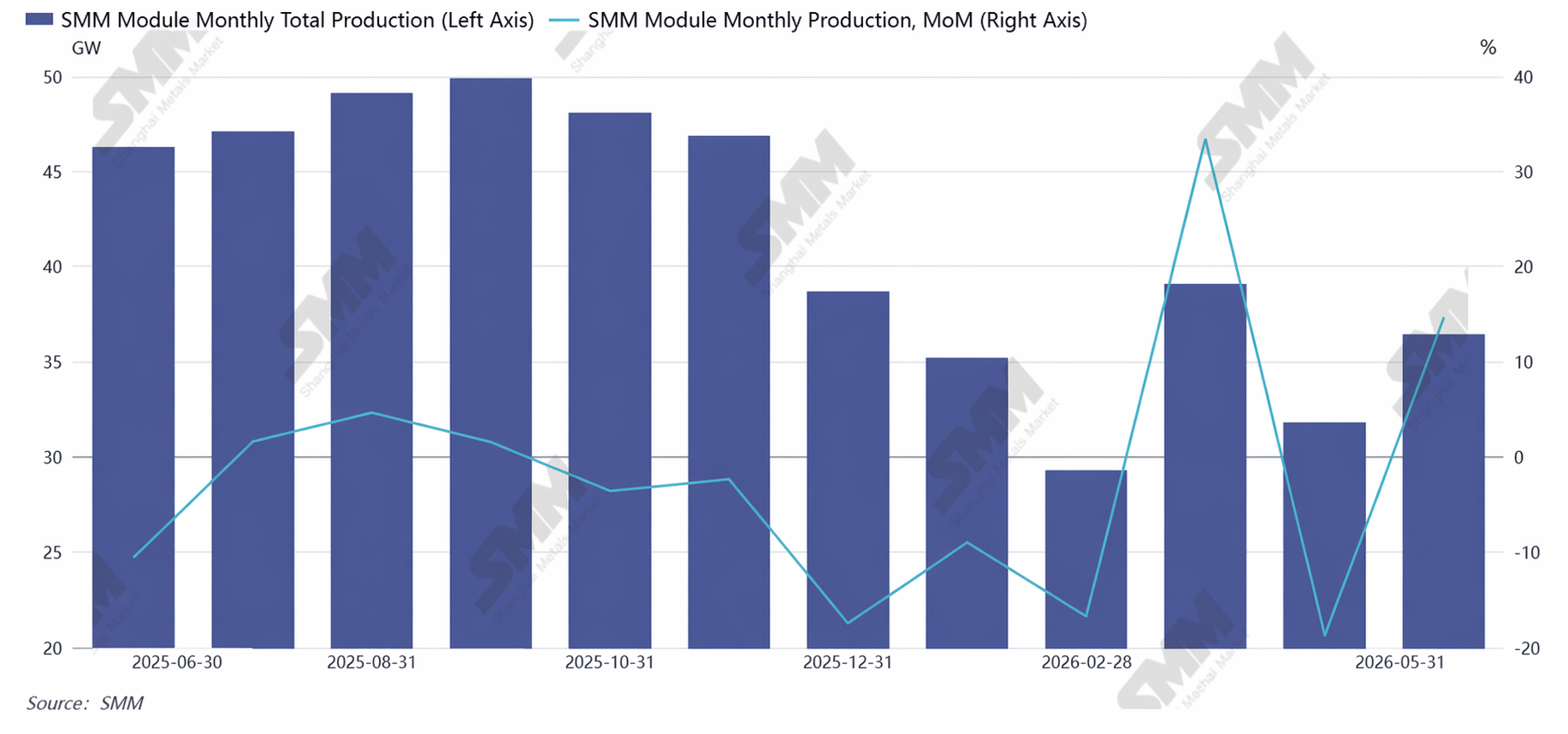

Demand Side: Domestic Installations Weakened; Overseas Markets Became the Only Demand Growth Driver

In 2026, due to China's consumption constraints, declining revenues from competitive grid pricing, and widespread delays in power station projects, H1 new installations in China fell significantly YoY, with the full-year expectation revised down to around 210 GW. Average monthly module production schedules in China dropped to around 35 GW in H1. Module factories prioritized destocking their own glass inventory, long-term contract purchases shrank substantially, and scattered rigid-demand purchases became the market mainstream, making pushing for lower prices an industry norm.

Overseas, by contrast, H1 installation expectations saw an overall increase of 30.24% from the previous year. Moreover, as overseas markets generally require localized production, local glass supply remains relatively limited, keeping their reliance on Chinese glass purchases strong.

Module Production Schedule Trend

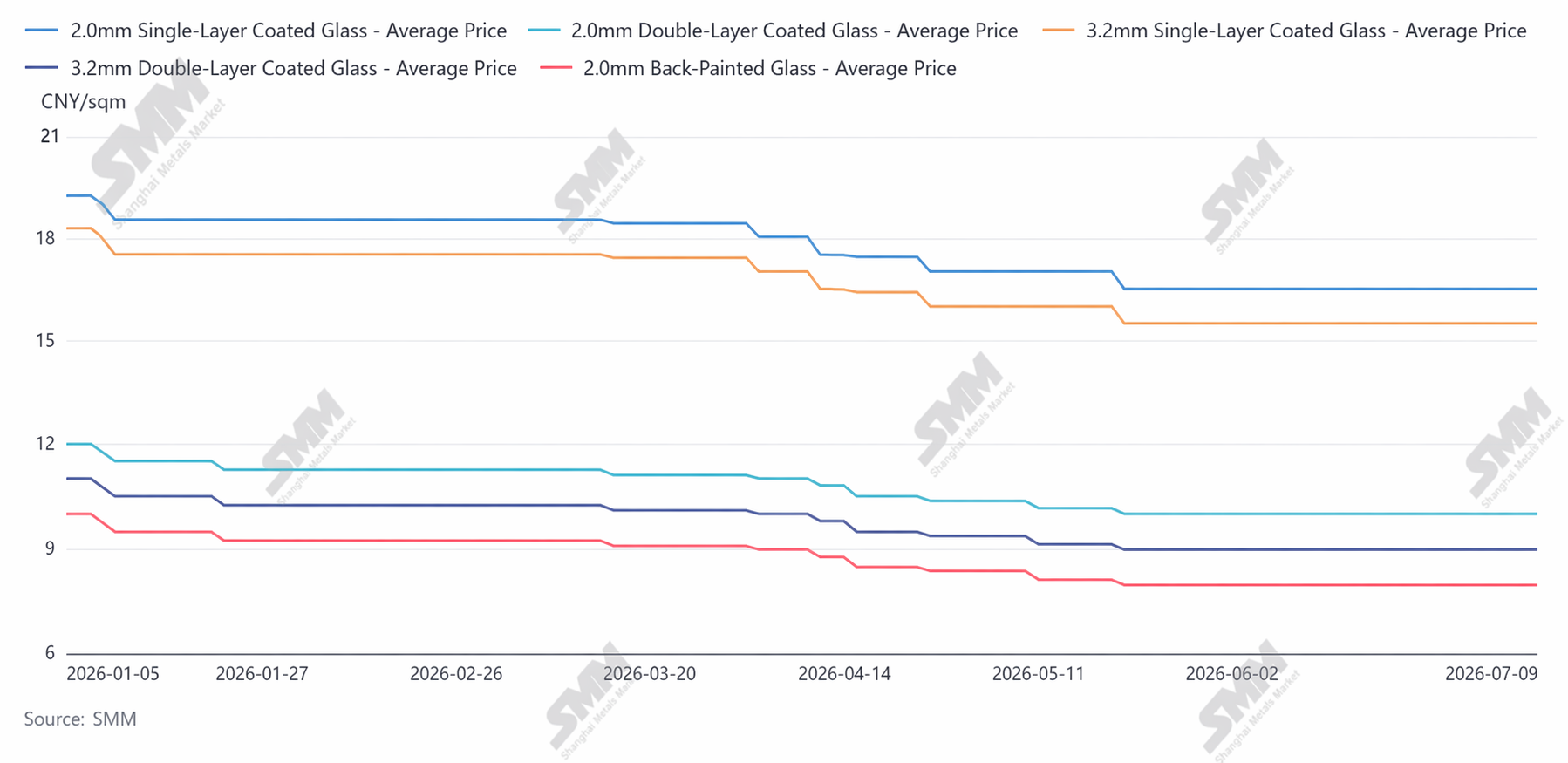

Price Trend: H1 Prices Fell Consecutively, Stabilized Slightly After Hitting Bottom in June; The Entire Industry Incurred Losses

PV glass prices in H1 2026 followed a trajectory of "a slow decline in Q1, an accelerated hit bottom in Q2, and a sideways trend at low levels in June," with all product specifications dropping to historic lows over the past five years. The price of 2.0mm single-layer coated glass was 10.5 yuan/m² at the start of the year, and by the end of June, the lowest transaction price had fallen to 8.0 yuan/m², a price decline of 23.8%, with losses reaching around 2 yuan/m².

The main reasons for the price decline were, on one hand, oversupply coupled with high inventory, driving enterprises to sell at low prices to recoup funds; on the other hand, downstream module makers, facing thin profits, continuously passed cost pressure upstream, creating a strong sentiment for pushing for lower prices.

Glass Price Trend

Technology Aspect: H1 Industry R&D Focused Entirely on Cost Reduction, Efficiency Improvement, and Compatibility with High-Efficiency Modules

First, thinner glass was fully popularized: 2.0mm became the standard for double-glass modules, and top-tier players advanced the mass production of 1.6–1.8mm ultra-thin glass, achieving weight reduction and lower silicon consumption for compatibility with large-format modules. Second, light transmittance exceeded 92.5%, with ultra-high-transparency glass reaching 94.7%, compatible with China's current high-efficiency modules. Finally, low-carbon melting furnace technology was implemented, and integrated PV glass scrap recycling production lines gradually commenced operation, reducing enterprises' production costs.

Regarding the H2 2026 outlook: Supply side, cold repairs for China's production lines are expected to keep advancing, accelerating the exit of inefficient capacity, contracting effective industry supply, and leading to slow inventory destocking. Demand side, Q3 is expected to see the launch of overseas demand and the start of centralized projects in China, so module production schedules are likely to rebound, marginally improving glass demand. Price side, after inventory declines persistently, prices are expected to have a foundation for recovery, but a significant price surge requires substantial capacity rationalization and a moderate increase in demand.

In summary, H1 2026 marked a trough period for the PV glass industry in recent years. However, as outdated capacity exits the market and technology is upgraded and iterated, glass supply and demand conditions are expected to recover, and China's involution behavior is likely to improve. The subsequent growth logic for the PV industry remains unchanged. After navigating through the industry cycle, glass is also expected to reach a new starting point.

![PV Aluminum Extrusion Operating Rate Remains Stable; Middle East Conflict and Aluminum Ingot Destocking Jointly Support Aluminum Prices [SMM Analysis]](https://imgqn.smm.cn/usercenter/FtiwK20251217171741.jpg)

![[SMM Analysis] Analysis and Outlook of the Solar Cell Market in H1 2026 – Prices Accelerate to Hit Bottom, Supply-Demand Recovery Still Awaits Verification](https://imgqn.smm.cn/usercenter/ZbnfH20251217171741.jpg)

![[SMM PV Flash] Xinjiang's 2027 Mechanism Electricity Price Bidding Announcement: PV 0.259 yuan/kWh](https://imgqn.smm.cn/usercenter/EcOMz20251217171741.jpg)