SMM News, July 9:

In H1 2026, intensified geopolitical games and rising trade policy uncertainties posed multiple challenges to the lead-zinc industry chain, including structural adjustments in ore supply, persistently declining TCs, and smelting costs under pressure. Lead concentrates remained in deficit, and the profit center shifted to by-products on the smelting side. How will the lead concentrate market play out in H2?

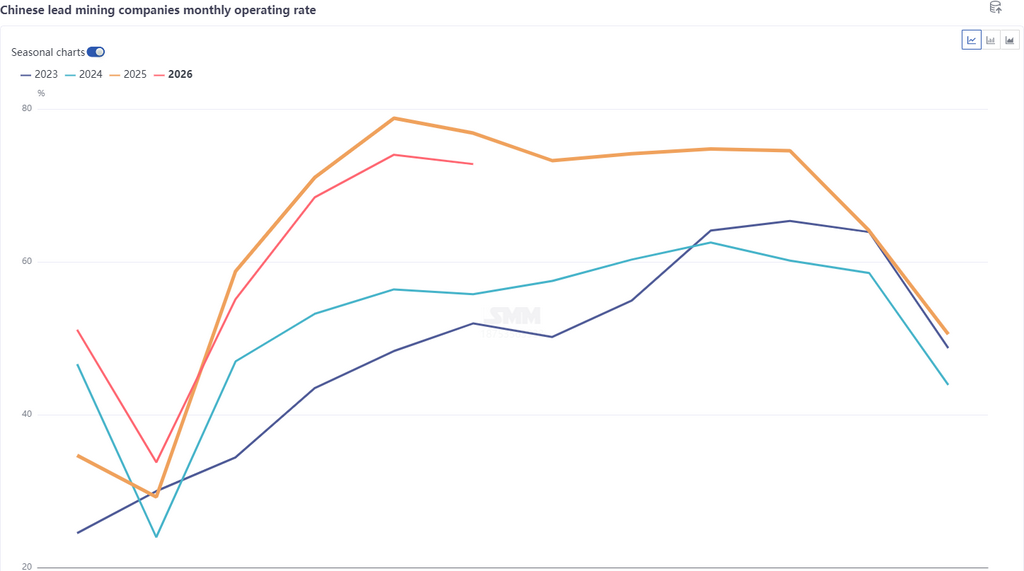

Production side, SMM lead concentrate production totaled 776,500 mt in metal content in January-June 2026, down 1.3% YoY, mainly due to declining raw ore grades and more frequent environmental and safety inspections at domestic mines. H1 production edged down slightly. In H2, with the gradual release of new capacity in China, production is expected to increase further, and full-year production is forecast to rise by 6,000 mt in metal content.

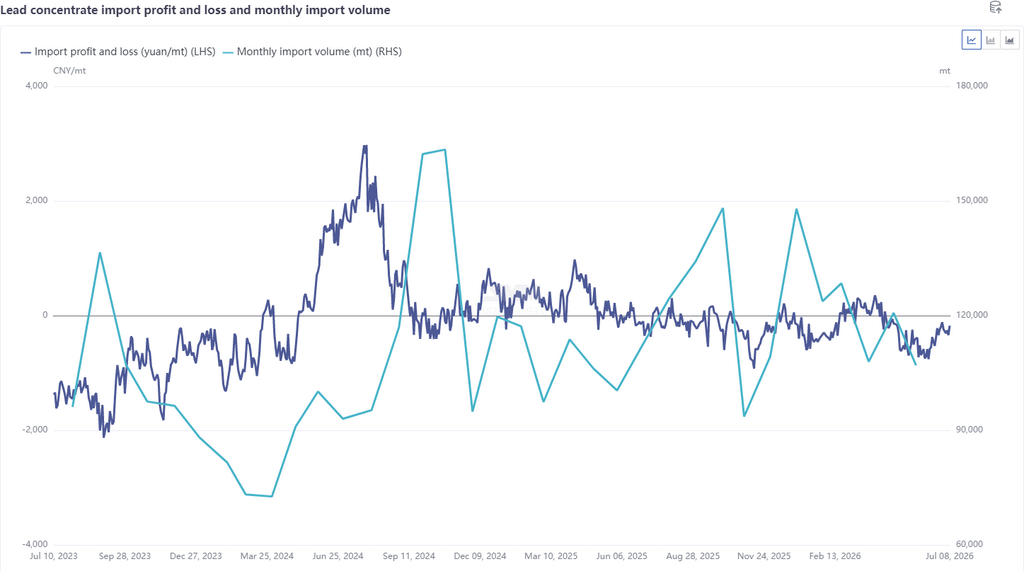

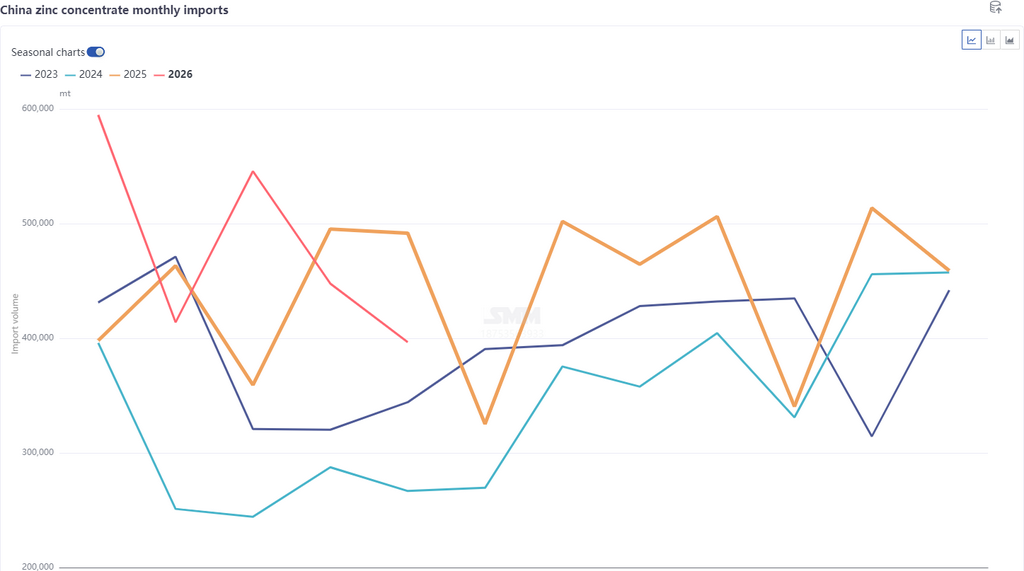

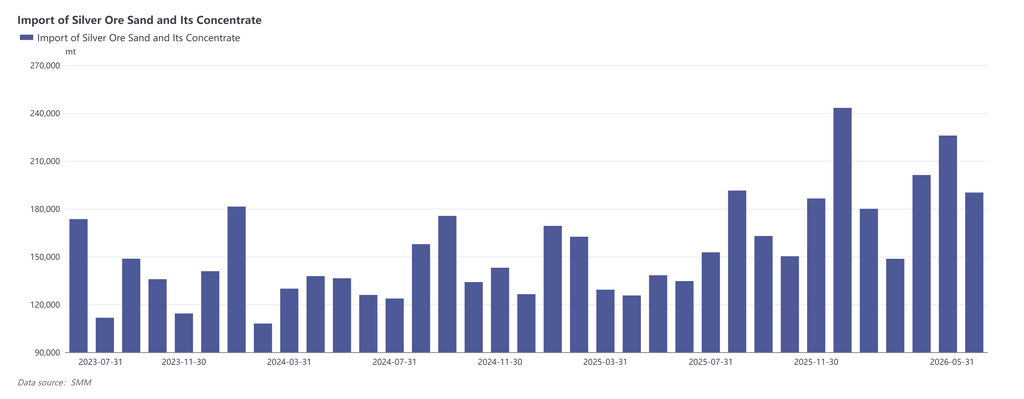

Imports side, China's lead concentrate imports reached 580,000 mt in physical content in January-May 2026, up 9.8% YoY cumulatively. In addition, part of the lead supply was supplemented by associated output from silver and zinc ores. Imports of silver ores and concentrates totaled 946,000 mt over the same period, up 130.5% YoY, and zinc concentrate imports amounted to 2.39 million mt in physical content, up 8.6% YoY. Imports of lead concentrates and lead content from other minerals partially offset the deficit in domestic production. For H2, considering lower ore grades outside China, strikes, energy shortages, and expectations of weakening price ratios, lead concentrate imports are expected to edge down slightly, yet full-year imports are still projected to register positive YoY growth. Driven by profits, silver ore and concentrate imports are expected to exceed 2 million mt for the full year. For zinc concentrates, facing similar challenges in H2 such as lower ore grades outside China, strikes, energy shortages, and import losses, full-year imports are forecast to edge down slightly.

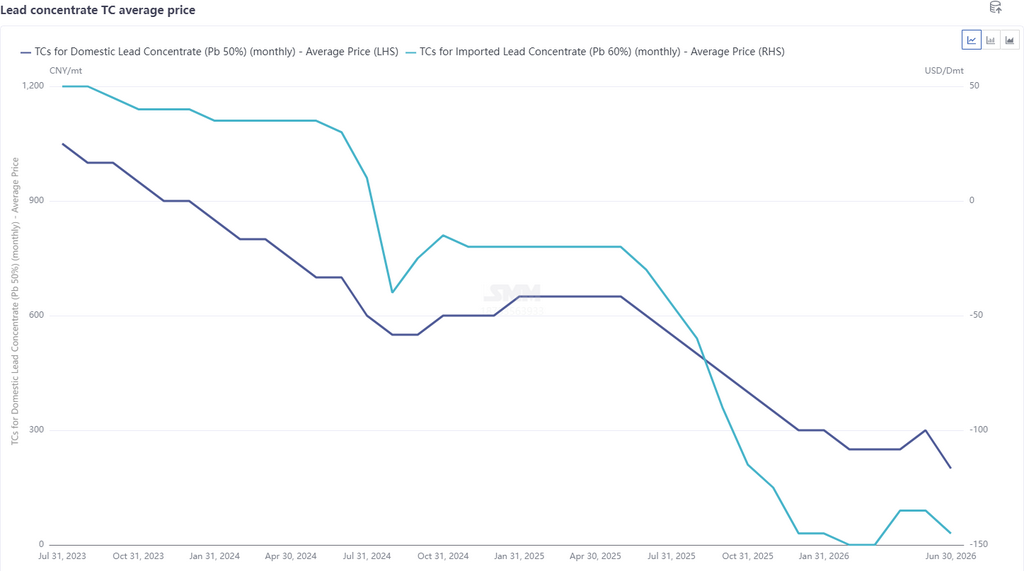

TC side, domestic lead concentrate TCs stayed in the doldrums in H1, mainly due to insufficient domestic ore supply and valuation boosts from silver by-products. Looking to H2, from a balance perspective, supply is expected to stay high, while ore-derived lead is expected to shift gradually to a slight surplus amid expectations for maintenance-related production cuts. However, given that silver-lead ore remains tight, lead concentrate TCs are unlikely to rebound, and with Q4 winter stockpiling expectations, TCs are still expected to edge down further.

Data Source Statement: All data other than publicly available information are processed by SMM based on publicly available information, market communication, and SMM's internal database models, and are for reference only; they do not constitute any decision-making advice.

![July 9 Scrap Battery Market Transaction Summary [SMM Daily Review]](https://imgqn.smm.cn/usercenter/XMxKT20251217171720.jpeg)