This week (20–26 March 2026), solid-state battery material prices showed structural divergence: sulphide-route LPSC and lithium sulphide prices declined, while oxides remained stable. On the industrial side, the Taiblue–Yadea two-wheeler semi-solid-state battery achieved commercial rollout; BTR’s solid electrolyte orders surged; and WELION New Energy’s 2 billion yuan project was sited in Huadu, Guangzhou. Upstream price cuts resonated with downstream deployment, accelerating the commercialisation process.

Recently, there were many industry conferences in and outside China in the solid-state battery field, and enterprises actively attended or held product launch events. Outside China, MG released a semi-solid-state battery with low liquid electrolyte content and is expected to enter Europe in 2026; QuantumScape released its commercialisation strategy for solid-state lithium metal batteries. In China, BTR’s solid electrolyte orders surged, and its oxide production line had completed construction; WELION New Energy’s 2 billion yuan solid-state battery project was sited in Huadu, Guangzhou; and the two-wheeler semi-solid-state battery co-developed by Taiblue and Yadea achieved commercial rollout.

I. Sulphide Route: Material Prices Under Pressure, Industrialisation Expectations Heating Up

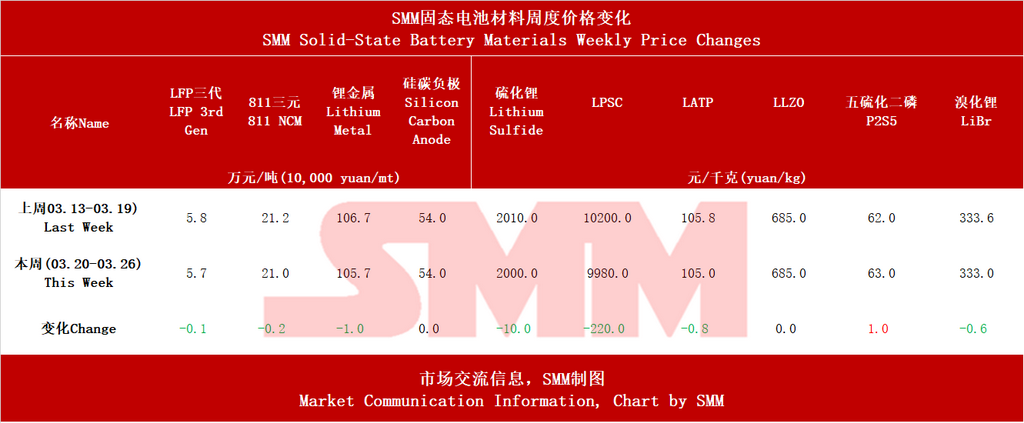

This week, core raw material prices for sulphide solid electrolytes showed a clear decline. The average price of battery-grade lithium sulphide fell to 2,000 yuan/kg, down 10 yuan week on week; LPSC (silver–germanium ore-type electrolyte) declined by 220 yuan to 9,980 yuan/kg, a drop of 2.2%. Supported by strong sulphur prices, the precursor P₂S₅ edged up by 1 yuan to 63 yuan/kg against the trend.

On 23 March, BTR disclosed that its solid electrolyte orders had surged; its 1,000-mt-class oxide production line had completed construction; and its oxide electrolyte sales exceeded 100 mt in 2025. Lishen Battery and FAW Co., Ltd. subsequently announced patents related to sulphide solid electrolytes. The sulphide route is regarded as the ultimate direction for all-solid-state batteries due to its ionic conductivity advantage; price declines on the materials side help reduce battery system costs and accelerate industrialisation.

II. Oxide/Polymer Route: Commercialisation Landing First

Commercialisation progress in the oxide and polymer routes was concentrated this week. The high-end electric motorcycle equipped with the semi-solid-state battery co-developed by Taiblue New Energy and Yadea, the “Guaneng Xingjian II-200L”, achieved commercial rollout, marking the first breakthrough in the two-wheeler scenario. Sinopec completed a polymer solid-state battery microgrid demonstration project in Suzhou; after one month of operation, it adopted a polymer solid electrolyte independently developed by the Sinopec Research Institute of Petroleum Processing. DARE Auto’s solid-state battery products made their first overseas appearance at the Tokyo Battery Show and the Australia Energy Storage Exhibition.

In terms of pricing, oxide electrolyte LATP and LLZO remained stable this week at 105 yuan/kg and 685 yuan/kg, respectively. Given higher process maturity, the oxide route already met commercialisation conditions in scenarios with relatively mild energy-density requirements, such as two-wheelers and energy storage.

III. Cathode and Anode: Slight Price Declines, Silicon Carbon Stable

This week, Gen-3 LFP fell by 1,000 yuan to 57,000 yuan/mt, and 811 ternary fell by 2,000 yuan to 210,000 yuan/mt. Lithium metal declined by 1 yuan to 105.7 yuan/g. The silicon carbon anode price was flat at 54 yuan/kg.

The decline in cathode material prices was mainly driven by the raw material side such as lithium carbonate, with a relatively indirect correlation to solid-state batteries. As a key material for high-energy-density batteries, the stable price of silicon carbon anodes reflected a relatively balanced supply-demand pattern.

IV. Industry Trends

The sulphide route entered a cost-optimisation phase: with declining LPSC and lithium sulphide prices advancing in tandem with capacity buildout (BTR) and patent deployment (Lishen, FAW), the industry was shifting from technical validation to cost justification.

Commercial rollout showed “two wings taking off together”: Taiblue–Yadea (two-wheelers), the Sinopec microgrid (energy storage), and MG SolidCore (automotive) achieved breakthroughs in different application scenarios, clarifying the “progressive” commercialisation path for solid-state batteries.

Overseas developments reinforced long-term expectations: QuantumScape released its commercialisation strategy for solid-state lithium metal batteries; and a three-party partnership among South Korea’s Kumho Petrochemical, POSCO, and BEI was developing an anode-free lithium metal battery, as overseas giants accelerated their deployment in next-generation technologies.

According to SMM forecasts, all-solid-state battery shipments will reach 13.5 GWh by 2028, while semi-solid-state battery shipments will reach 160 GWh. Global lithium-ion battery demand is projected to reach approximately 2,800 GWh by 2030, with the EV sector's lithium-ion battery demand showing a CAGR of around 11% from 2024 to 2030, ESS lithium-ion battery demand at a CAGR of about 27%, and consumer electronics lithium battery demand at a CAGR of roughly 10%. Global solid-state battery penetration is estimated at about 0.1% in 2025, with all-solid-state battery penetration expected to reach around 4% by 2030, and global solid-state battery penetration potentially approaching 10% by 2035.

**Note:** For further details or inquiries regarding solid-state battery development, please contact:

Phone: 021-20707860 (or WeChat: 13585549799)

Contact: Chaoxing Yang. Thank you!

![Weekly Review of the Lithium Carbonate Market: Spot Lithium Carbonate Fluctuated Upward on 3.23-3.26 [SMM Weekly Review]](https://imgqn.smm.cn/usercenter/WgbTp20251217171727.jpg)