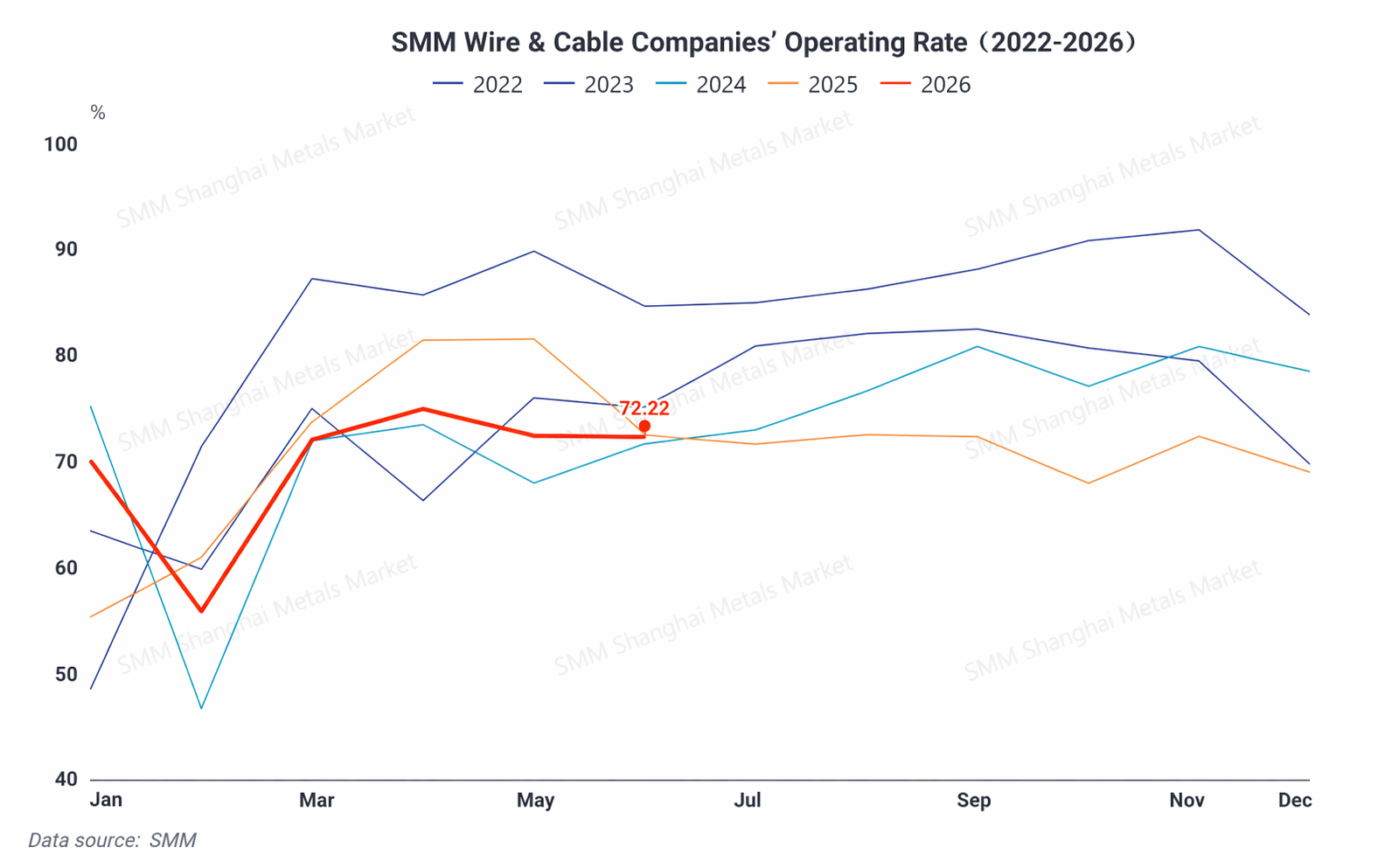

In H1 2026, the operating rate of China's wire and cable industry generally showed a trend of "rapid post-holiday recovery, peaking during peak season then gradually pulling back." At the beginning of the year, under pressure from Chinese New Year and high copper prices, the industry's operating rate hit bottom at 27.72%. It then rapidly recovered, driven by concentrated grid delivery and phased copper price pullback. Later, after copper prices rebounded and influenced by the traditional off-season, the operating level gradually pulled back.

I. H1 Market Review and Summary: Copper Price Fluctuations Dominate, Power Grid Shines

Wild swings in copper prices were the core variable influencing the industry's operating pace in H1. In Q1, the start of the "15th Five-Year Plan" power grid investment formed a demand base. The phased decline in copper prices further stimulated end-users to concentrate on restocking at lows. After copper prices rebounded in Q2, downstream purchase willingness was suppressed. However, structural volume growth in demand from emerging fields such as new energy and AI provided some support at the bottom for the operating rate.

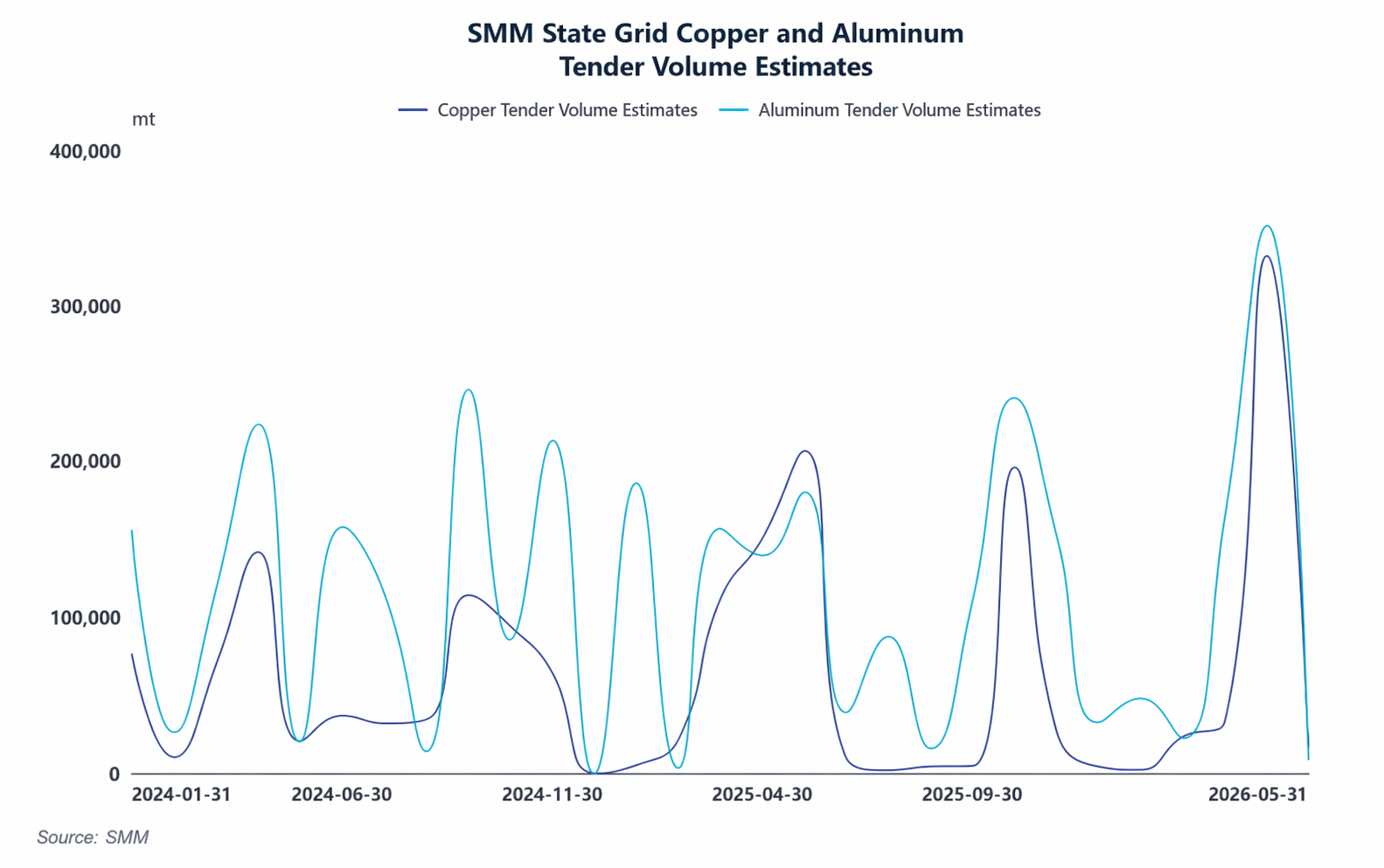

From the perspective of various demand ports, the proportion of cables used in traditional power grid infrastructure has declined, while the proportion for new energy supporting applications has risen significantly. Offshore wind power, energy storage, NEVs, and data centers have become the core new growth drivers. However, the power grid remains the core pillar of demand. In Q1, State Grid Corporation of China completed fixed asset investment of over 129 billion yuan, up 37% YoY, directly driving a concentrated release of wire and cable demand. Notably, the demand for cables supporting AI data centers has entered an explosive period. SMM forecasts that the growth rate of copper demand for AI data centers will reach 54.94% for the full year. Demand for high-speed copper cables and power supporting cables is growing steadily, and the operating rates and production schedules of relevant domestic enterprises are staying high. In contrast, in traditional sectors, data on new starts and completions in real estate remained sluggish. Demand for home decoration and civilian building cables also weakened, overall offsetting the growth dividend of emerging tracks.

Cost side, industry profitability was notably under pressure. On one hand, the overseas geopolitical conflict in March pushed up prices of cable auxiliary materials. Coupled with high industrial energy costs, enterprises' comprehensive production costs were passively pushed up. On the other hand, during the rapid surge in copper prices in May, enterprises' raw material procurement costs had already risen sharply, but some order settlements were still based on earlier lower monthly average prices, leading to further profit margin compression. Coupled with fierce competition in the ordinary cable track, enterprises basically have no room for price adjustment or premium, ultimately resulting in compressed profits for small and medium-sized wire and cable enterprises in H1, and industry profits concentrated upstream in raw materials.

II. Exports Remain Highly Prosperous, Imports Only Serve as High-End Supplement

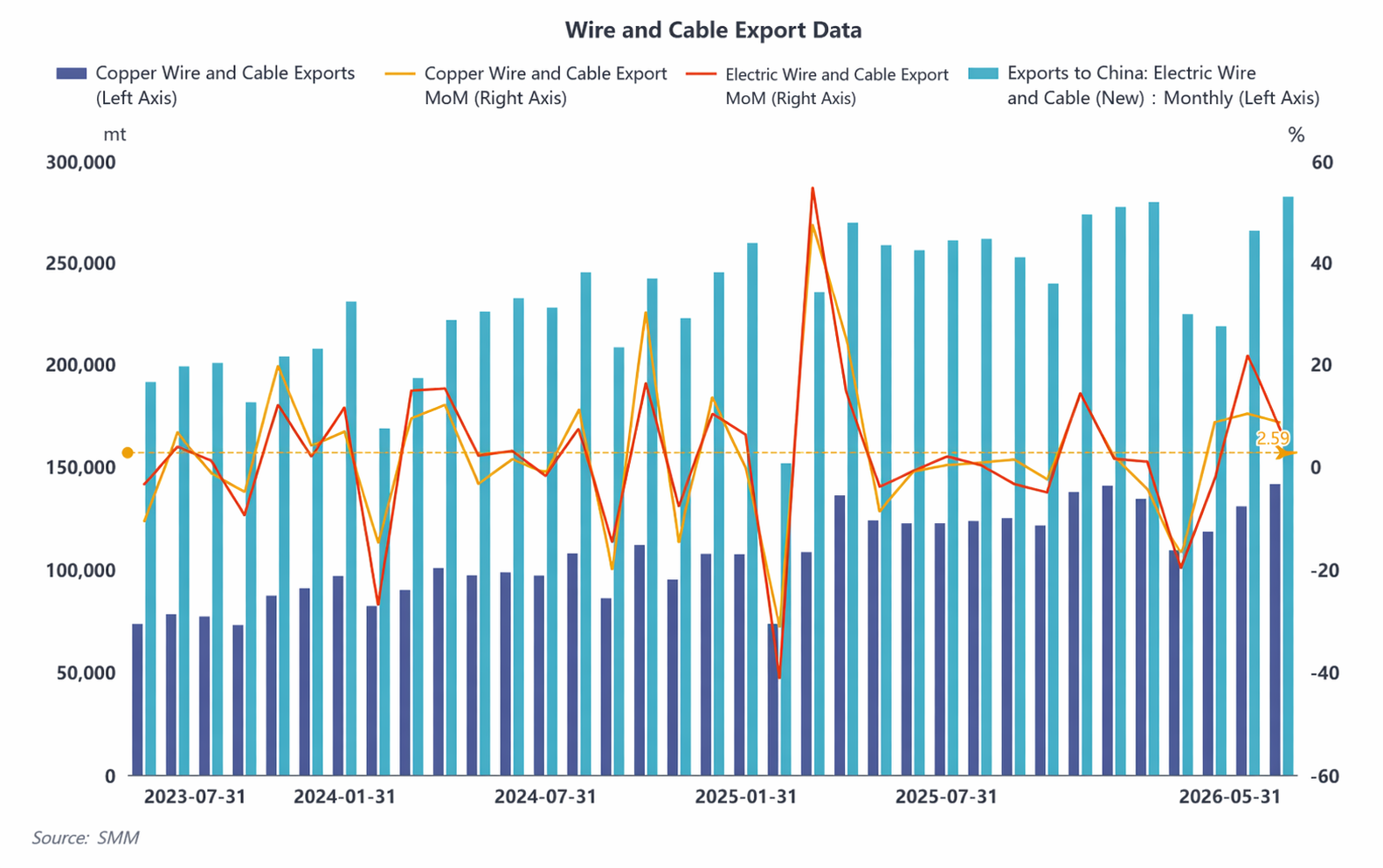

In terms of imports and exports, exports continued to be highly prosperous. From January to May, cumulative exports of wire and cable reached 1.2692 million mt, up 8.12% YoY. Among them, exports of copper wire and cable were 633,700 mt, up 15.6% YoY, with Australia, the Philippines, and Thailand being the top three destinations.The core driving force behind the export boom is the rigid import demand formed by infrastructure expansion and energy transition in Southeast Asia, the Middle East, and Africa. Grid renovation and AI computing power supporting construction in Europe and the US continue to release growth, boosting the willingness of domestic enterprises to go global. Imports are relatively small in scale. From January to May, cumulative imports of wire and cable were 53,400 mt, mainly serving as a supplement for high-end products.

III. H2 Market Outlook: Demand Structure Diverges, Emerging Tracks Maintain High Growth

Looking ahead to H2, copper price fluctuations remain the core variable throughout the second half. If copper prices continue to fluctuate at highs, they will continue to suppress end-user stockpiling willingness, limiting the room for demand recovery during the peak season. During the traditional consumption off-season, conventional terminal orders from real estate and civilian sectors are weak. The industry operating rate will consolidate at lows, and end-users will maintain a cautious strategy of locking copper based on orders and making just-in-time procurement. It will be relatively difficult for orders to recover. Entering the H2 consumption peak season, the first-year conclusion of the "15th Five-Year Plan" will drive a concentrated sprint in power grid projects. Ultra-high voltage and distribution network tenders are accelerating, and Q4 delivery expectations are sufficient, becoming the core support for H2 demand. The high prosperity of emerging tracks continues. The demand for copper cables supporting AI data centers continues to grow in volume. The growth rates of offshore wind power and energy storage cables are highly certain. The steadily increasing penetration rate of NEVs drives the growth of wiring harness and charging pile cable demand. The traditional construction and real estate sector is unlikely to improve and will continue to drag down overall demand performance. On the export front, the export momentum from H1 is expected to continue into H2. Rigid demand from grid renovation and upgrades in Europe and the US, as well as AI computing power supporting construction, continues to be released. In Southeast Asia, the Middle East, and Africa, infrastructure expansion and energy transition are advancing at a high speed, and import dependence on China's cables remains high. Coupled with the continuous deepening of domestic enterprises' go-global layout and increasingly mature overseas channels, export prosperity will remain at a high level in H2, and full-year cable exports are expected to hit a new high.

![Copper Cathode Rod Operating Rates Edged Up This Week; Pullback Expected Next Week Due to Poor Order Continuity [SMM Copper Cathode Rod Weekly Review]](https://imgqn.smm.cn/usercenter/CaLPF20251217171713.jpg)