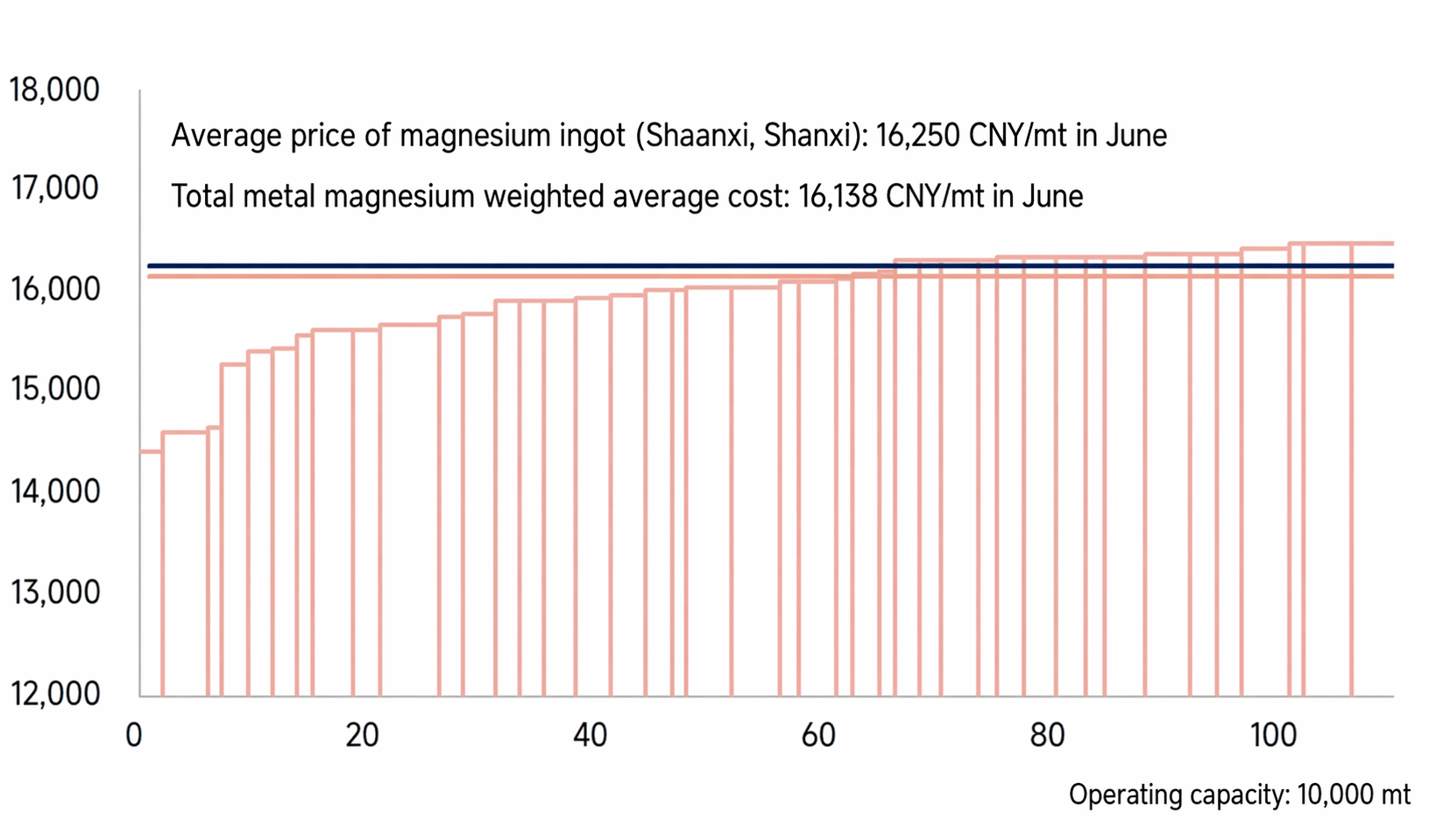

In June, the tax-inclusive full cost of China's magnesium ingot industry rose 1.18% MoM to 16,138 yuan/mt, an increase of 1.18% MoM, as the cost advantage from the previous month largely evaporated. A safety incident at the Qinyuan coal mine in late May directly tightened the supply of circulating raw coal in the region, driving market coal prices up rapidly. There was a clear time lag in the transmission of the semi coke market, which intensified production losses at semi coke plants and significantly raised the core energy feedstock cost for primary magnesium smelting. Enterprises mitigated some cost pressure by boosting capacity to spread fixed expenses such as plant and equipment depreciation, but the incremental cost impact from rising energy prices was stronger. Overall industry smelting costs trended higher, continuing to compress processing margins at upstream smelters and narrowing profit space for most enterprises.

Raw material costs: Delivered prices for dolomite ore remained stable, with limited overall impact.

A leading dolomite quarry in the Wutai area of Shanxi faced a prolonged shutdown, sustaining a local supply shortage. Most magnesium smelters locked in long-term ore procurement contracts, keeping delivered dolomite purchase prices stable. Quarries in multiple regions, including Hubei, Henan, and Inner Mongolia, continued to ramp up shipments, effectively filling the market supply gap. The regional diversion of ore sources reduced the impact of supply disruptions from any single origin, leading to relatively small cost fluctuations for dolomite feedstock. This exerted a limited boost on overall magnesium ingot production costs and did not create significant upward cost pressure.

Auxiliary material costs: Ferrosilicon prices ground lower while other auxiliary materials edged higher, leaving costs basically flat MoM.

At this stage, the tug-of-war between longs and shorts is intense in the ferrosilicon market. Upstream raw coal and semi coke costs provided bottom support, suppressing downside room, but downstream demand from the steel and foundry industries remained sluggish with weak procurement enthusiasm. These opposing forces offset each other, constraining wild swings. In the short term, spot ferrosilicon prices moved sideways near 5,950 yuan/mt, with a weak trend as it continued to grind lower. Slight price increases for other smelting auxiliary materials offset concessions in ferrosilicon, leaving the comprehensive cost of auxiliary materials basically flat MoM, without imposing additional cost burdens on magnesium smelters.

Energy cost: Coal prices weakened initially before strengthening, but had a limited impact on magnesium smelting costs.

Safety rectifications at the Qinyuan coal mine in late May tightened the circulating supply of raw coal, with spot raw coal prices surging quickly in the short term and pushing up feedstock procurement costs for semi-coke plants. The pace of semi coke price transmission lagged behind the rise in raw coal, making it difficult for semi coke plants to raise their selling prices in sync. The industry generally fell into losses, directly increasing energy expenditure for primary magnesium smelting. Raw coal prices pulled back at month-end, but the full-month average coal price was still higher than in May. Based on our calculations, the industry's energy cost per mt of magnesium ingot increased by approximately 150 yuan MoM, making it the core driver of this month's cost increase.

Labour cost: With operations running at full capacity, per mt labour costs remained low and stable.

The current market magnesium price bottoming out boosted production enthusiasm at smelters. Mainstream primary magnesium enterprises in China largely maintained continuous full-capacity production, maximizing the operational efficiency of on-site personnel and equipment. After allocating total labour expenditure per mt of magnesium ingot, the figure remained low with no significant monthly fluctuations. The cushioning effect of amortized labour costs was evident, and this segment did not boost the full cost of the overall industry.

![Magnesium Ingot Market Bottoms Out, Off-Season Demand Under Pressure Drags on Price Rise [SMM Magnesium Weekly Review]](https://imgqn.smm.cn/usercenter/jMeFI20251217171722.jpeg)