In H1 2026, China's silicone market was affected by multiple factors such as the cancellation of export tax rebates, industry self-discipline emission reduction, raw material cost fluctuations, and seasonal shifts between peak and off-peak demand in end-user industries. The overall market trend exhibited an inverted V-shape, initially strong then weakening, with a retreat after a rapid rise. The market landscape shifted from a tight supply-demand balance in Q1 to a weak pattern of ample supply and weak demand in Q2.

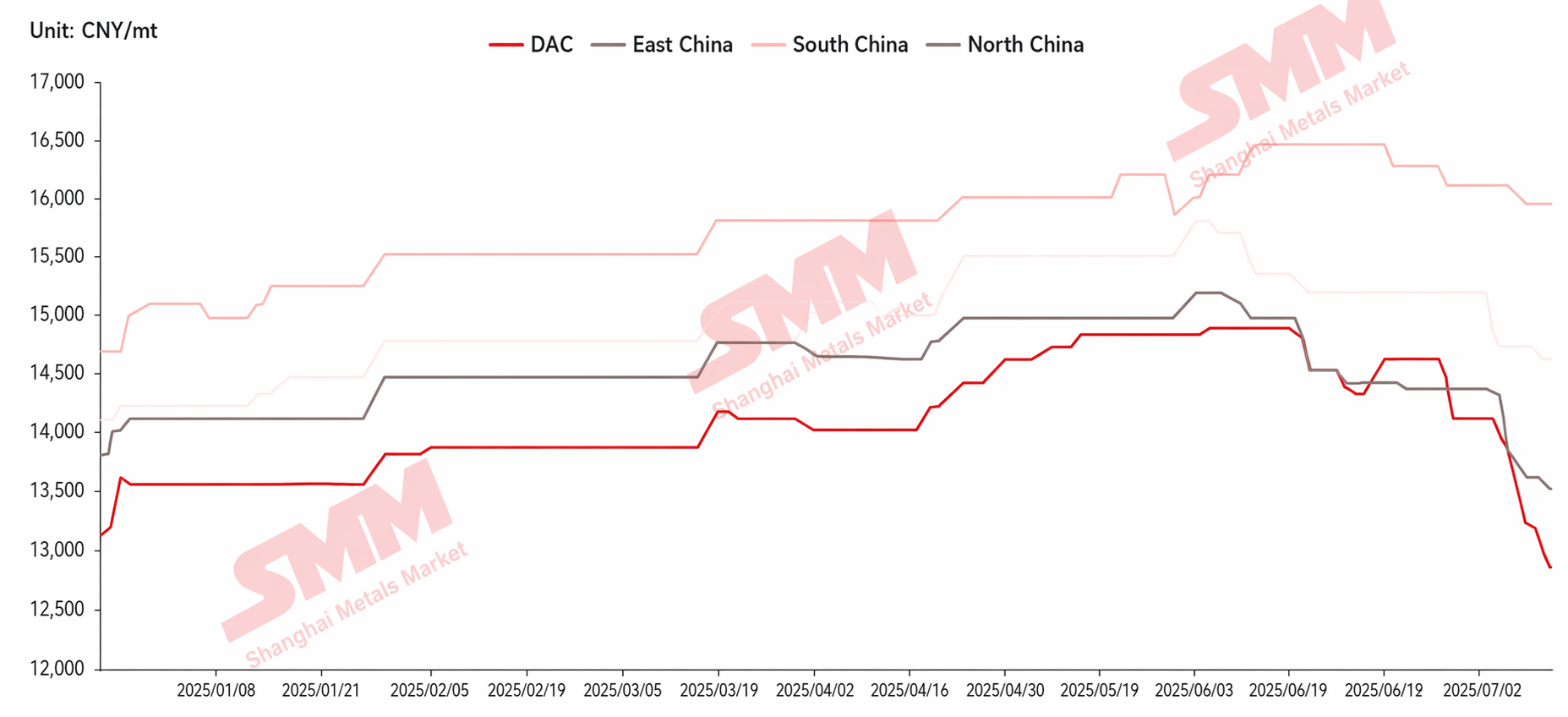

1. Price Trend: Multiple Bullish Factors Drive Prices Higher, Supply-Demand Reversal Leads to Deep Correction

In H1, prices of all silicone product categories, including DMC, 107 silicone rubber, silicone oil, and MVQ, followed an inverted V-shaped trajectory. From January to April, the industry's 35% self-discipline emission reduction and monomer facility maintenance tightened supply. This coincided with front-loaded orders before the cancellation of export tax rebates, bullish market sentiment, concentrated demand release from stockpiling around the Chinese New Year, and rising methanol raw material costs due to geopolitical conflicts. Supply, demand, and costs formed a positive resonance, pushing prices steadily upward. By the end of April, DMC prices surged to a high of 14,850 yuan/mt. In May, monomer maintenance units gradually resumed production, releasing supply. Meanwhile, in June, the industry's 40% reduction standard saw divergent enforcement and fell short of expectations. At the same time, downstream sectors entered the traditional off-season, and both domestic and external demand weakened. Enterprises competed on price to move goods, fueling bearish sentiment. Prices continued to retreat, with DMC dipping to 13,000 yuan/mt by the end of June, confirming a weak market pattern.

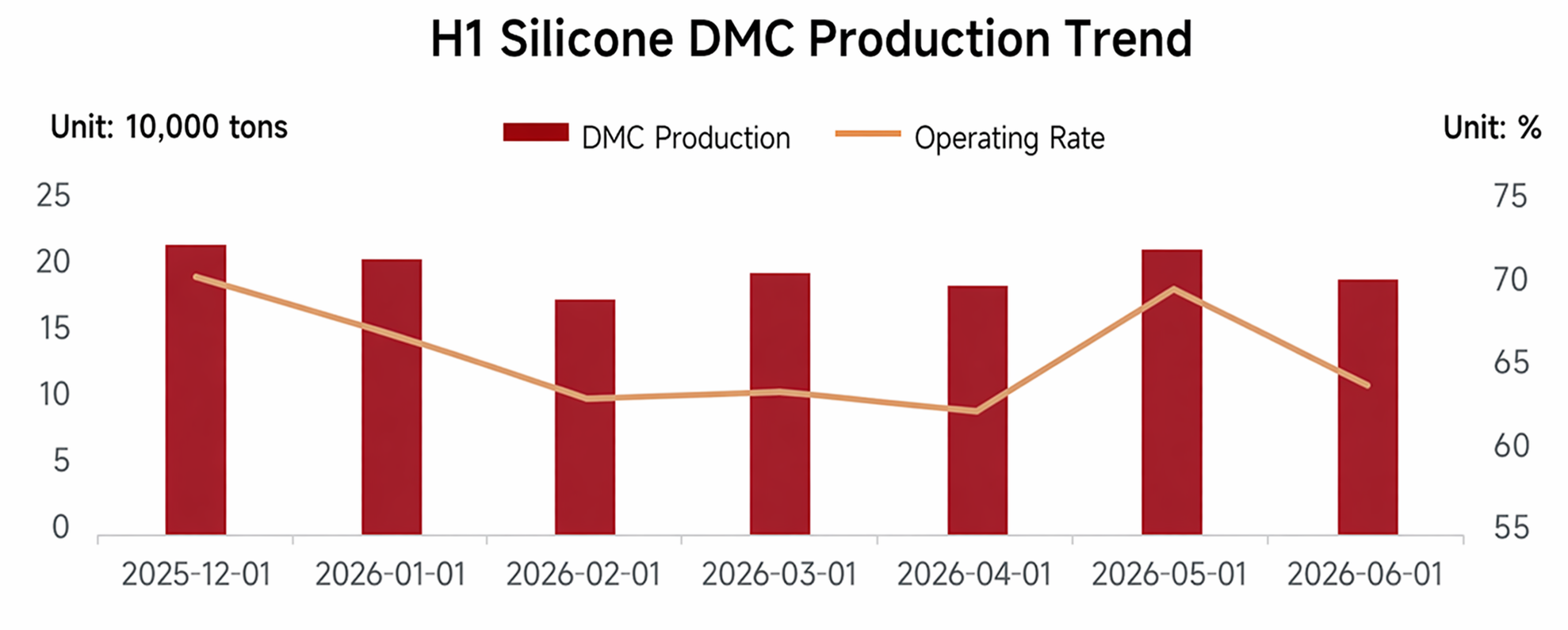

2. Supply Dynamics: Phased Volume Control and Contraction, Supply Ample in Mid-to-Late Period

H1 DMC production totaled about 1.1542 million mt, down 1.7% YoY, with an average operating rate of around 64%. From January to April, supported by the 35% self-discipline emission reduction and multiple plant maintenances, operating rates continued to decline, and supply contracted by 3.58% YoY, delivering significant phased output control. In May, production resumptions from maintenance units led to a surge in supply, directly boosting the overall supply base for H1. In June, although the industry raised the reduction standard to 40%, the lack of mandatory enforcement led to divergent implementation among enterprises, resulting in only a slight production pullback that failed to effectively ease supply pressure. The overall market remained in a state of oversupply.

3. Demand Fluctuations: Q1 Impulse from Domestic and External Demand, Persistent Weakness in Q2

H1 silicone market demand rose initially then declined, with strong phased characteristics. In Q1, driven by the cancellation of export tax rebates, overseas clients front-loaded orders intensively. Combined with Chinese New Year stockpiling and the traditional spring peak season, domestic and external demand together provided essential demand support, effectively absorbing market inventory and bolstering the market upturn. In Q2, following the implementation of the tax rebate cancellation, export orders dropped sharply. Meanwhile, domestic end-user industries entered the traditional off-season, and downstream players showed little willingness to restock proactively, only maintaining rigid procurement. Demand support was absent, and the supply-demand mismatch intensified downward market pressure, becoming the core factor dragging down the market.

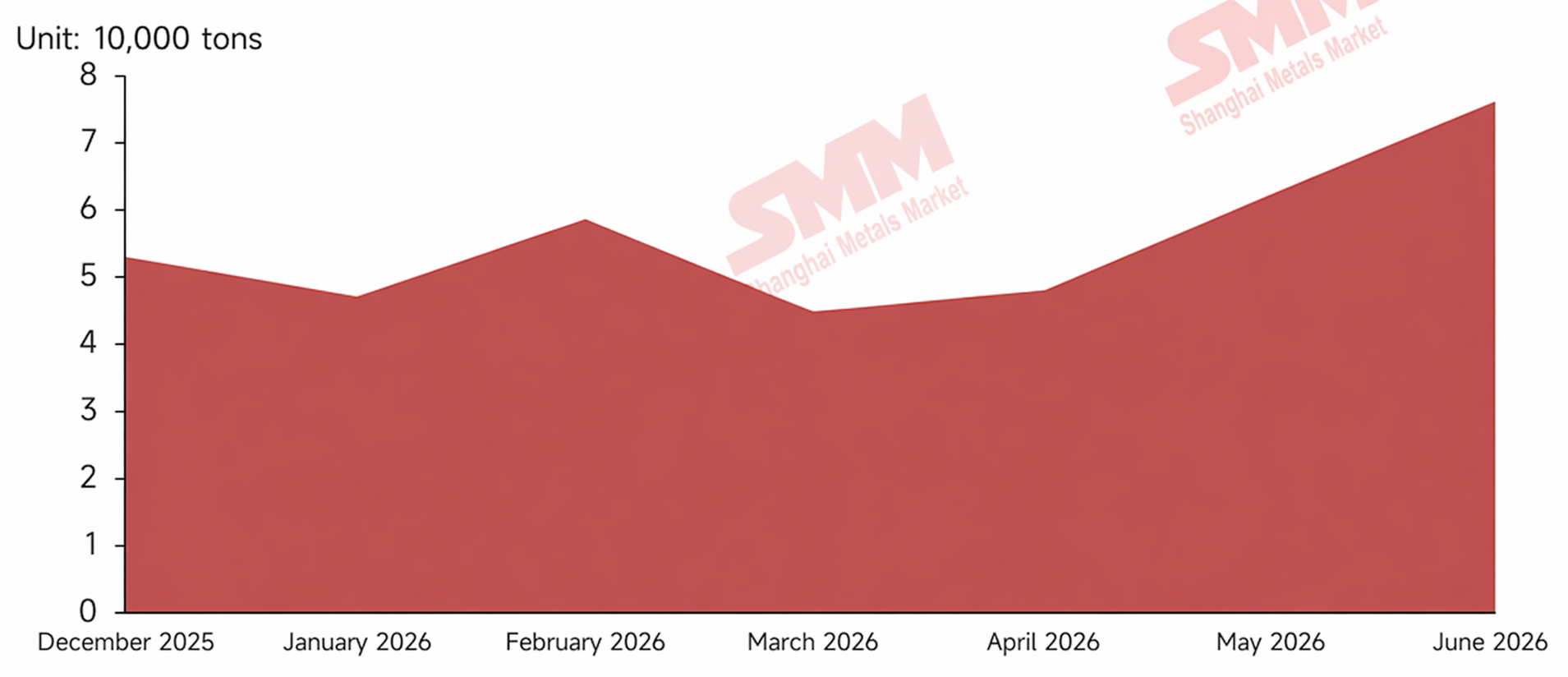

IV. Inventory Performance: Effective Destocking in Q1, Inventory Buildup Under Pressure in Q2

H1 monomer enterprises' polysiloxane inventory exhibited a divergent trend of initial destocking followed by buildup. In Q1, supply contracted and demand was intensively released, driving continuous destocking; upstream inventory remained low and the supply-demand pattern was tight. In Q2, exports shrank and domestic demand weakened, coupled with a concentrated supply release, leading to a loose supply-demand pattern and rapid inventory buildup; inventory surged about 42% MoM in May, sharply increasing upstream inventory pressure, forcing enterprises to cut prices to move goods, further intensifying bearish trading sentiment, and creating a negative cycle of inventory buildup, price cuts, and wait-and-see attitudes.

Subsequent market outlook: the overall market is expected to consolidate on a subdued note in the near term. On the supply side, the August resumption of a monomer facility in Shandong that has been idled for years will bring new supply; coupled with currently moderate industry profits, doubts exist over the enforcement of voluntary production cuts, so supply may be difficult to effectively curtail. On the demand side, although the traditional September-October peak season is expected to arrive, driving a modest recovery in rigid demand and a temporary price rebound, without special stimulus or policy dividends, the seasonal boost may be unsustainable, only influenced by the strength of end-user recovery. Overall, the peak season can only bring a phase-based recovery and is unlikely to reverse the overall weak tone. If subsequent supply and demand fail to meet expectations, the market still faces further downside risks.

For silicone-related inquiries, please contact: 021-20707889

![Cost Support and Off-Season Pressure Coexist, Secondary Aluminum Prices Continue to Move Sideways [Aluminum Scrap and Secondary Aluminum Weekly Review]](https://imgqn.smm.cn/usercenter/CkvAg20251217171724.jpg)

![Off-Season Demand Drags, EMM Remains Weak and Moves Sideways [SMM EMM Weekly Review]](https://imgqn.smm.cn/usercenter/rUQIB20251217171723.jpeg)

![Marginal Demand Recovery: Manganese Sulphate Rises Steadily and Mildly [SMM Battery-Grade Manganese Sulphate Weekly Review]](https://imgqn.smm.cn/usercenter/qbMSp20251217171722.jpeg)