SMM July 9:

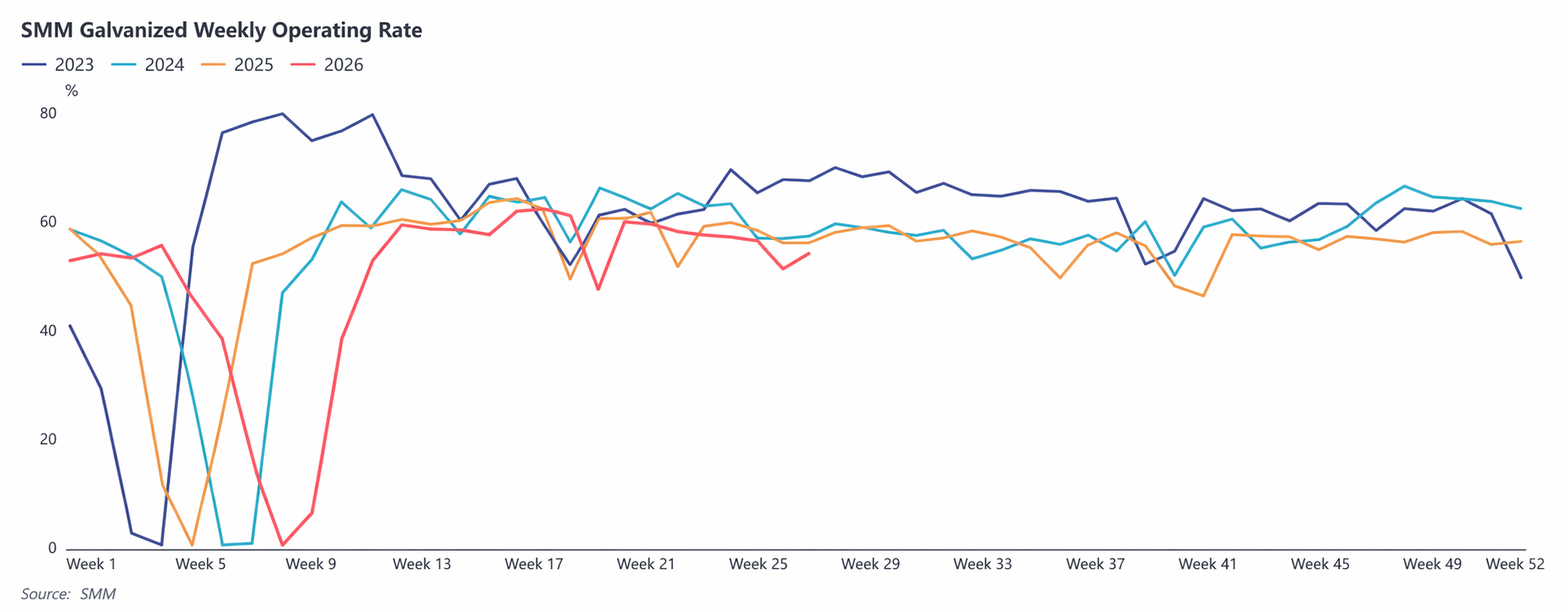

In H1 2026, the galvanizing industry exhibited a pattern of slow recovery in Q1 and underperformance in the peak season during Q2, with overall operating rates weaker than the same period last year.

In Q1, affected by the Chinese New Year holiday, persistent weakness in ferrous metals prices before the holiday, and insufficient willingness for winter stockpiling, enterprises halted production and went on holiday earlier; the pace of post-holiday work resumption and worker return was slow, compounded by environmental protection disruptions in the north. Although operating rates gradually recovered in March, they remained lower than the same period last year.

In Q2, traditionally a peak consumption season, the market broadly expected demand improvement, supported by policy expectations from the 15th Five-Year Plan, power grid, ultra-high voltage, and underground pipeline network construction. However, the actual end-use recovery fell short of expectations. New construction starts in real estate remained weak, with only projects under the ensure timely delivery of housing projects policy supporting some rigid demand. The pace of local government bond fund disbursement was slow, and infrastructure project starts progressed slower than expected. Policy benefits had not yet effectively transmitted to end-use consumption, leaving the industry overall facing insufficient peak season realization.

Nevertheless, there were still structural bright spots within the industry. Engineering-related orders such as steel towers, power grid, and export guardrails maintained strong resilience, while traditional demand for construction galvanized sheets and civil-use pipes remained weak. Overall, the demand recovery for the galvanizing industry in H1 was relatively slow, and operating rates remained weak on a YoY basis.

Outlook for H2 2026

Looking ahead to H2, the galvanizing industry is expected to show a trajectory of "weakness in the early part, strength later, and gradual recovery."

During July–August, real estate and infrastructure construction will still face certain constraints due to high temperatures and the traditional off-season, and the industry operating rate is expected to remain at low levels. As September peak season stockpiling starts at the end of August, and special-purpose bond funds gradually generate physical workload, construction of infrastructure projects such as underground pipeline networks, power grids, and UHV is expected to accelerate, and end-use demand will gradually improve.

After entering September, the impact of high temperatures will weaken, and the traditional peak season will arrive. Previously accumulated stockpiling demand and infrastructure construction demand will be released intensively, and the industry operating rate is expected to rebound significantly. Although real estate is unlikely to generate significant incremental demand, infrastructure investment, power grid construction, and some export orders will still provide support for the industry. It is expected that the industry's prosperity in H2 will improve compared to H1, and the YoY decline in full-year operating rates will continue to narrow.

(The above information is based on market collection and comprehensive assessment by the SMM research team and is for reference only. This article does not constitute direct investment or research decision-making advice. Clients should make cautious decisions and not use this as a substitute for independent judgment. Any decisions made by clients are unrelated to SMM.)

![2026 Low-Grade Zinc Oxide Market Half-Year Review [SMM Analysis]](https://imgqn.smm.cn/usercenter/EviJV20251217171754.jpg)