Over the past two years, the Middle East has gradually emerged as one of the world's major emerging photovoltaic (PV) markets with significant potential. Various Middle Eastern governments have established distinct PV targets, such as Saudi Arabia's 'Vision 2030' plan, which aims to generate 50% of its electricity from renewable energy, and strategic plans like the 'Dubai Clean Energy Strategy 2050'. Meanwhile, regions such as Oman have also become critical hubs for the overseas expansion of the PV manufacturing supply chain.

Recently, geopolitical turbulence in the Middle East has emerged, bringing a certain degree of impact to the overall overseas PV market. Below, SMM provide an in-depth analysis of the current Middle East PV market from various perspectives:

I. Market Demand

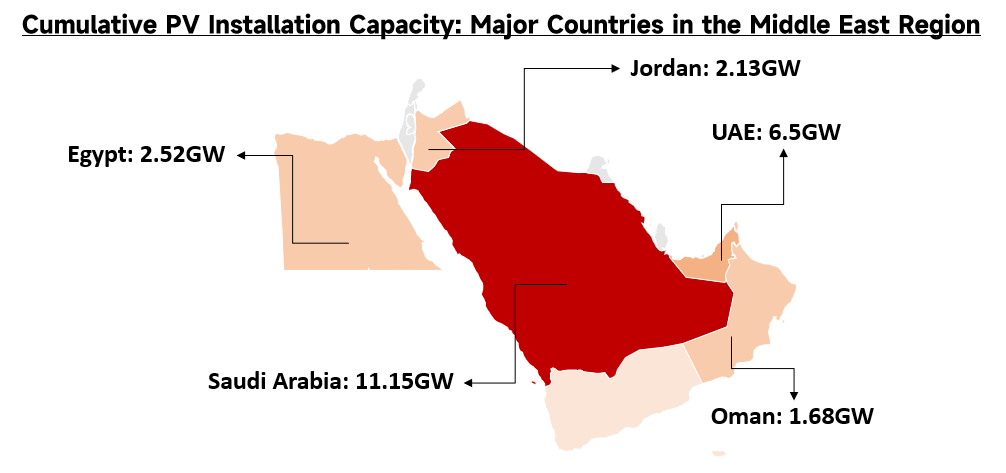

The Middle East exhibits prominent characteristics of an emerging PV market, demonstrating a highly synergistic trend between the expansion of local installed capacity and the demand for module imports. Regarding overall installed capacity, the energy transition process in the Middle East and North Africa (MENA) region has accelerated. By 2025, the total operational capacity of various renewable energy sources reached 43.7 GW, a significant increase from 30.3 GW in 2024. In the grid-connected PV sector, by the end of 2025, the actual operational PV installed capacity in the region reached 34.5 GW, representing an addition of 12.2 GW compared to the end of 2023. In terms of distribution among major countries, Saudi Arabia's operational PV capacity reached 11.15 GW, while the United Arab Emirates (UAE) reached 6.5 GW.

Source: SMM

On the module import demand side, the region shows a high degree of reliance on the overseas supply chain. According to incomplete statistics from SMM, the cumulative import volume of PV modules in the Middle East remained at approximately 24 GW from 2024 to 2025. In terms of the supply landscape, China is the absolute core source country for the Middle East PV market. PV modules exported from China to this region account for 95% of the total import volume, with an overall year-on-year increase of 74.57%. Regarding the distribution of major importing countries, the market exhibits high concentration: Saudi Arabia accounts for approximately 75% of the overall market share for module imports in the Middle East; the UAE demonstrates an extremely high growth rate, accounting for about 17% of imports with a year-on-year increase of 97.1%; Iran accounts for 5.5% of the total import share. Overall, the infrastructure demand for PV modules across Middle Eastern countries continues to remain at a high level.

II. Construction Progress

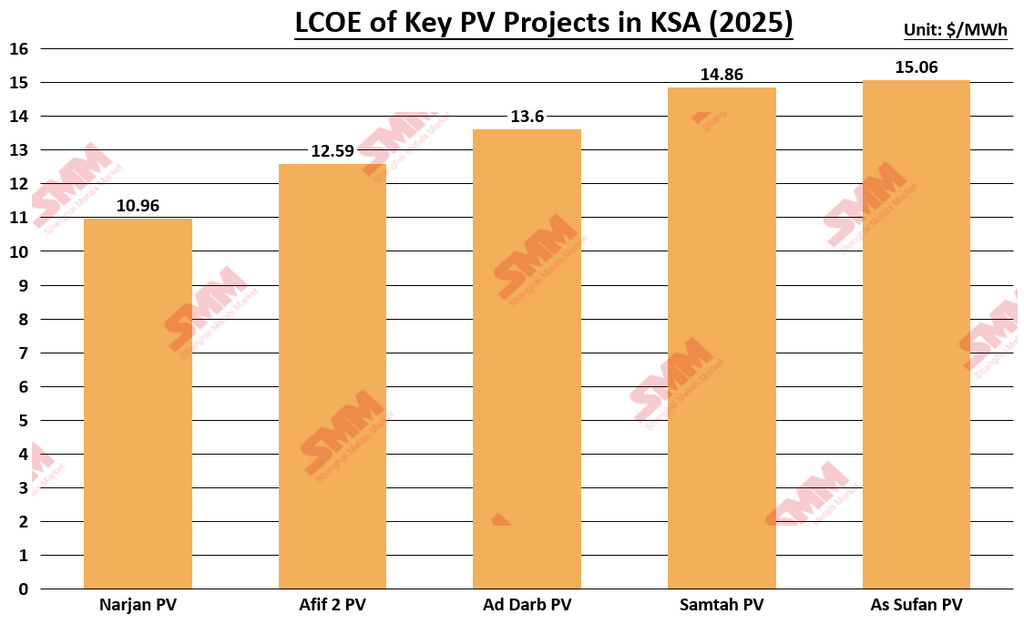

Middle Eastern PV projects generally adopt extremely low Power Purchase Agreement ('PPA') tariffs during bidding, which severely compresses profit margins. Taking the latest selected Independent Power Producer (IPP) projects in Saudi Arabia in 2025 as an example, the winning levelized cost of energy for the 1,400 MW 'Narjan PV' project is only 10.96 USD/MWh, and for the 2,000 MW 'Afif 2 PV' project, it is only 12.59 USD/MWh. This profit model highly tests the Engineering, Procurement, and Construction (EPC) contractors' ability to manage first-year cash flows with extreme precision. March to April is the traditional assessment node for grid-connection operations in the Middle East market. EPC contractors must complete full or partial grid connections during this phase to ensure the power plants can fully cover the high solar irradiation period of the summer from May to September. Current geopolitical conflicts have led to equipment supply chain disruptions and on-site construction restrictions. The actual impact is reflected in the following four core dimensions:

-

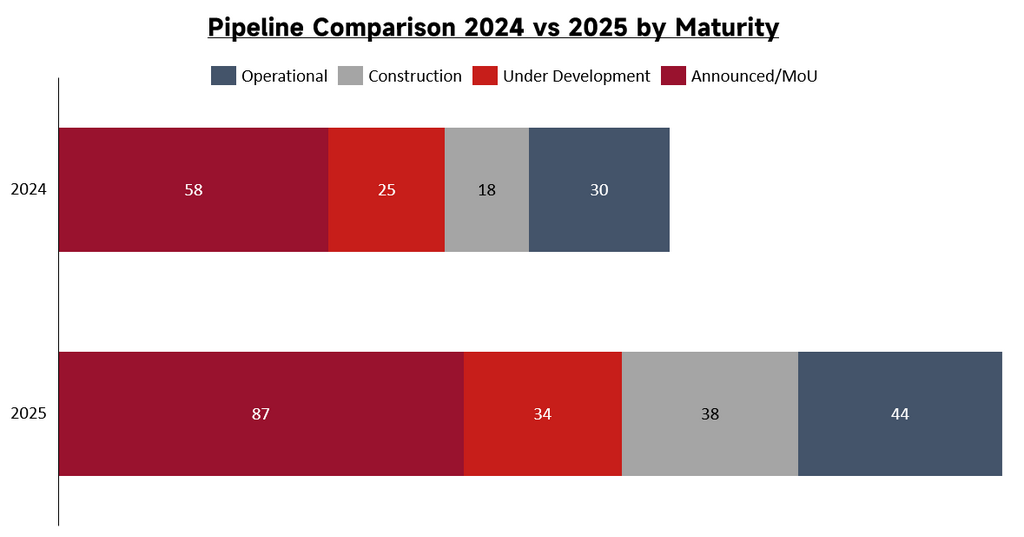

Impact on a massive and rapidly growing capacity base: Data shows that the total capacity of renewable energy projects under construction in the MENA region reached 38 GW in 2025, doubling the 18 GW recorded in 2024. In terms of project numbers, there are 61 renewable energy projects under construction in the region, primarily concentrated in Algeria (17), Saudi Arabia (14), and Egypt (10).

Source: SMM

-

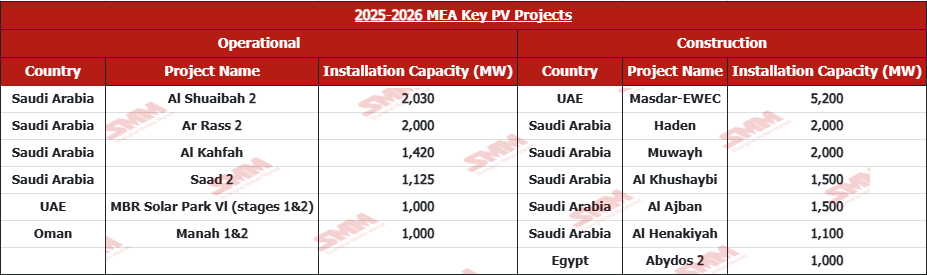

Major centralized projects facing delivery challenges: Geopolitical turbulence directly affects the delivery schedules of large-scale landmark projects currently under construction. Ultra-large projects presently in the construction phase include the 'Masdar-EWEC' (5,200 MW) in the UAE, as well as the 'Haden' (2,000 MW) and 'Muwayh' (2,000 MW) projects in Saudi Arabia. Although earlier projects such as 'Al Shuaibah 2' (2,030 MW) and 'MBR Solar Park VI' (1,000 MW) have been successfully commissioned, the newly added backbone capacity under construction faces significant schedule uncertainty.

-

Ancillary material delivery and labor shortages extending construction periods: Delays in the maritime transport of core modules, inverters, and tracking mounts, compounded by risk-aversion restrictions for foreign engineering personnel on-site, have caused the construction schedules of most large centralized projects to be postponed by at least one to two quarters.

-

Internal Rate of Return ('IRR') setbacks: If projects under construction miss this year's peak summer power generation period due to delays, the first-year power generation and expected revenue will drop significantly. As indicated by the aforementioned extreme winning bid prices of 10 to 15 USD/MWh, under the financial model of such low 'PPA' tariffs, the delayed inflow of first-year cash flow will directly breach the bottom line of the project's overall return on investment. Simultaneously, EPC contractors will also face the risk of massive Liquidated Damages ('LDs') compensation for failing to connect to the grid on schedule.

Source: Dii Desert Energy

III. Logistics and Transportation

The Middle East is not only an end market for PV products but also a critical node for global logistics. Currently, cross-border PV logistics face the dual pressures of peak domestic shipping volumes and obstructed international shipping lanes. On the domestic shipping side, the past two weeks coincided with the Chinese New Year holiday. The post-holiday period inherently faces the pressure of concentrated cargo transportation during the traditional work resumption phase. Furthermore, March is a critical window for the cancellation of China's PV product export tax rebates. To avoid cost increases brought by this policy adjustment, major enterprises are intensively accelerating shipments, which has further substantially driven up the overall export transportation pressure recently.

On the international transportation side, the massive wave of shipments is encountering severe tests from the geopolitical situation in the Middle East. Currently, the shipping lanes in the Strait of Hormuz are affected by blockades, directly cutting off the conventional transport route (via the Suez Canal) for Chinese PV modules destined for the European market. Logistics merchant vessels are forced to alter their routes and bypass the Cape of Good Hope in Africa. According to SMM, under the dual squeeze of post-holiday concentrated shipments and route alterations, the comprehensive transportation costs for shipments to Europe are expected to double. Concurrently, the overall maritime shipping cycle is extended by approximately half a month compared to the conventional route. Objectively, this series of factors significantly increases the supply chain financial pressure and inventory turnover time for the European PV market.

IV. Post-War Reconstruction

Regarding the restoration of post-war energy systems, PV power generation possesses the objective attributes of short construction cycles and precise cost control, making it the primary energy solution for the reconstruction of post-war power systems. Furthermore, the off-grid mode, which combines PV power generation equipment with energy storage systems, has the capability for independent operation during special periods. Storing the electricity generated by PV arrays in energy storage equipment can provide a stable power supply during periods when the external main power grid is paralyzed.

SMM believes that the comprehensive restoration of infrastructure after the war will strongly drive potential new demand for PV modules. Under conditions where traditional centralized transmission and distribution networks are damaged and difficult to fully repair in the short term, PV systems, due to their modular deployment characteristics, will be directly integrated into the reconstruction projects of residential and commercial facilities, as well as critical public infrastructure such as medical centers. Driven by the rigid electricity demand for post-war recovery, the Middle East market will enter a cyclical phase of incremental module procurement after experiencing short-term project stagnations. The power supply reliability demonstrated by solar-plus-storage hybrid technology under turbulent conditions will further solidify its core position in the civilian and industrial infrastructure planning of various countries, thereby substantively promoting the overall scale of PV module procurement and installation in the Middle East region.

V. Summary

Geopolitical turbulence in the Middle East is exerting a bidirectional impact on the global PV market. In the local market, the turbulent situation directly leads to the postponement of PV installation projects within the Middle East; from a long-term perspective, future reconstruction efforts based on infrastructure restoration will further stimulate the potential demand for PV-related products in the region. Regarding the global supply chain, the obstruction of Middle Eastern transportation hubs is triggering logistics delays and cost increases for other overseas markets, such as Europe.

Appendix: Major PV Projects in the Middle East (2025-2026)

Written by: Ryan Tey Tze Yang (ryan.tey@smm.cn)

![[SMM PV News] CHN Energy Commissions 4 GW Lingwu PV Base on Subsidence Land](https://imgqn.smm.cn/usercenter/dtQDq20251217171740.jpg)

![[SMM PV News] France's 2025 Renewable Curtailment Doubles to 3 TWh](https://imgqn.smm.cn/usercenter/LlMgj20251217171739.jpg)

![[SMM PV News] Premier Energies Unveils India's First 0BB TOPCon Solar Cell](https://imgqn.smm.cn/usercenter/vghcI20251217171739.jpg)