SMM June 16 News:

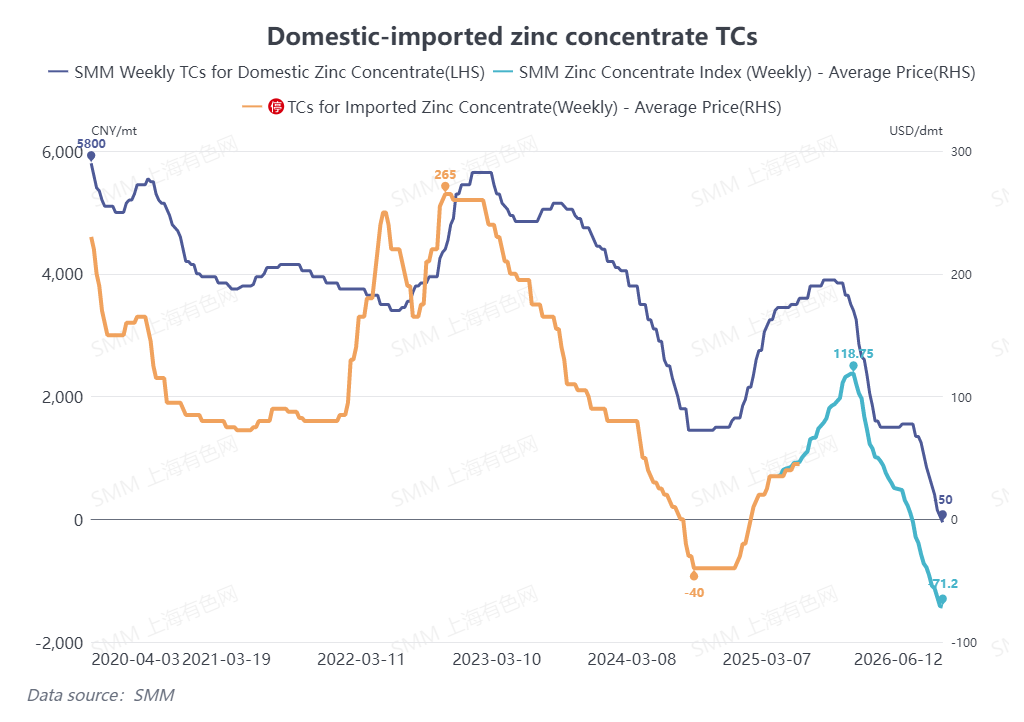

Time flies as the midpoint of 2026 approaches. The zinc concentrate market has witnessed another extraordinary price cycle this year. As of June 12, domestic zinc concentrate treatment charges (TCs) plunged to -50 yuan per metric ton of zinc metal, marking the arrival of negative TCs. Meanwhile, TCs for imported zinc concentrate tumbled to -71.2 US dollars per dry metric ton, both hitting all-time record lows.

I. Disturbances in Run-of-Mine Grades vs. Ramp-Up of New Capacities: Barely No Growth in Domestic Zinc Concentrate Circulation in H1

Domestic Mine Supply Side

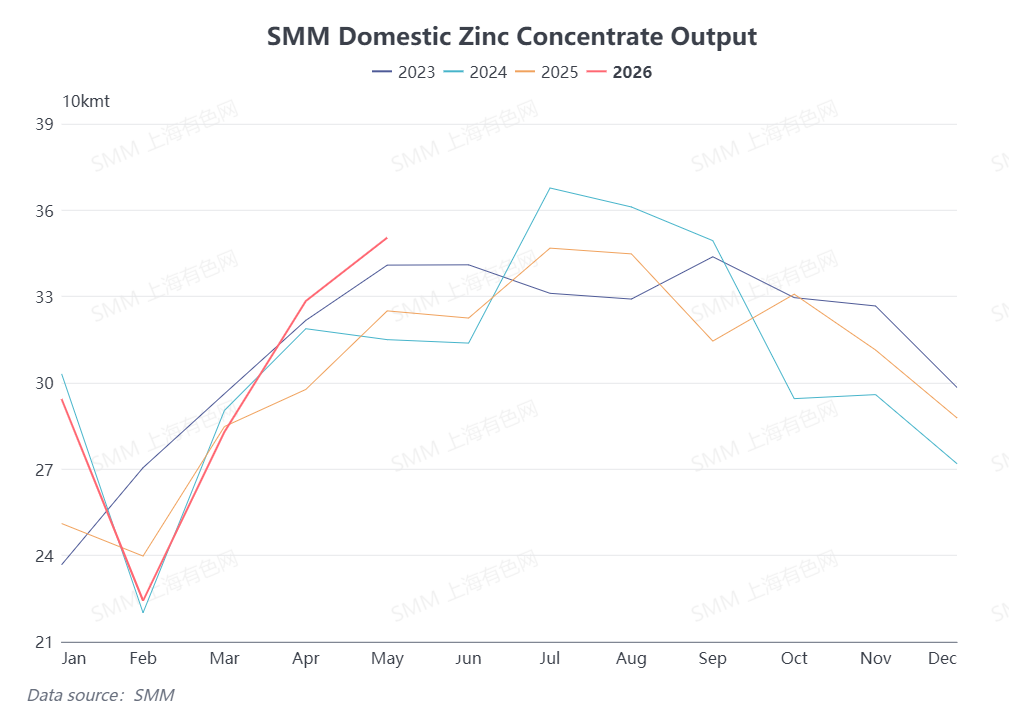

SMM statistics show China’s total zinc concentrate output reached 1.48 million metric tons of contained zinc metal from January to May 2026, representing a year-on-year increase of 5.9%. In terms of new capacities, the Huoshaoyun Zinc Mine maintained steady ramp-up throughout H1 and delivered the bulk of domestic output growth. Most other new mine projects are scheduled to launch capacity releases in H2, making limited contributions to H1 supply. For existing operating mines, improved profit margins of zinc concentrate facilitated the scheduled resumption of production at northern domestic mines that suspended operations earlier. This supported seasonal recovery in national output. Nevertheless, mines in North China, Southwest China and other provinces recorded year-on-year production declines due to falling run-of-mine ore grades. Combined with unplanned mine shutdowns and delayed production restarts, the overall circulating volume of domestic zinc concentrate saw virtually no growth in the first half of the year.

H2 Supply Outlook

Multiple new mine projects are set to commence production in Q3 and Q4, bringing incremental supply to domestic zinc concentrate. In addition, mines that halted production for seasonal maintenance fully resumed operations by June, while most mines suspended due to unforeseen disruptions plan to restart production in June and July. Coupled with sustained capacity ramp-up at the Huoshaoyun Zinc Mine, domestic zinc concentrate output is projected to register a sequential rise in H2 compared with H1.

II. Limited New Capacity & Frequent Mine Disruptions: Global Zinc Concentrate Output Outside China to Post Year-on-Year Decline in 2026

Q1 Performance

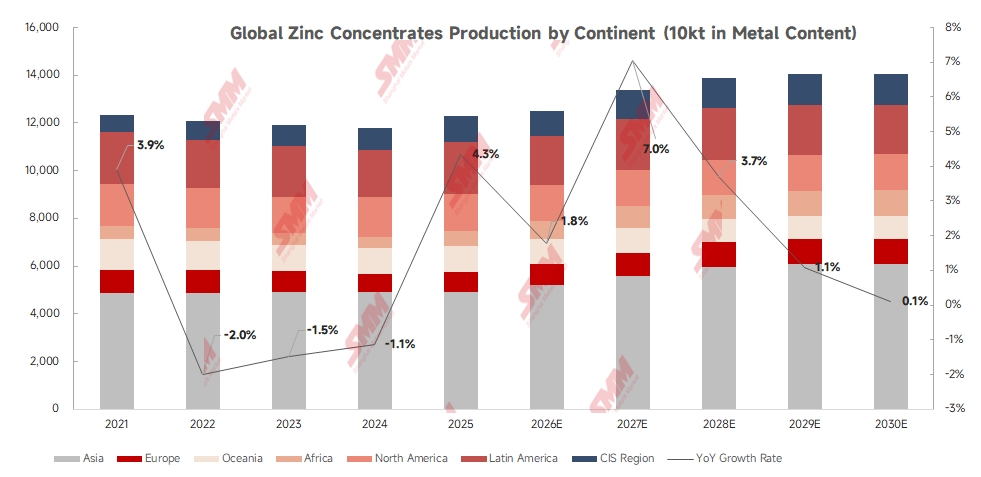

SMM tracked production data from 20 major overseas mining enterprises. Their aggregate zinc mine output totalled 1.282 million metric tons of contained zinc metal in Q1 2026, down 41,000 tons or 4.1% year-on-year, and down 119,500 tons or 8.5% quarter-on-quarter. Production across overseas mines suffered notable setbacks in Q1 amid multiple headwinds including seismic activities, declining ore grades and flooding disasters.

Q2 Performance

Mine disruptions remained relatively mild overseas in Q2 to date. The Garpenberg Zinc Mine kicked off production recovery in Q2. Meanwhile, China Nonferrous Metals Industry Group’s Darry Mining Indonesia secured the Feasibility Certificate for Environmental Impact Assessment (SKKL) issued by the Ministry of Environment and Forestry of the Republic of Indonesia, granting approval for lead-zinc mining activities at Silima Pungga-Pungga Subdistrict, Darry Regency, North Sumatra Province.

Full-Year Global Supply Forecast

On the growth side, the Romina Zinc Mine is scheduled to launch production this year, the Gamsberg Mine will continue capacity ramp-up, while the Aljustrel and Endeavor Mines resumed operations in Q1. However, substantial supply losses will offset new incremental output. The Antamina Mine is expected to cut annual zinc concentrate production by over 200,000 contained metal tons year-on-year. Several mining zones under Glencore’s Mount Isa complex will cease operations. Teck’s Red Dog Mine revised down its full-year zinc concentrate production guidance by roughly 60,000 contained metal tons year-on-year, and Boliden’s Garpenberg Mine faces operational constraints stemming from earthquakes. Taken together, overseas zinc concentrate output is poised to fall year-on-year in 2026.

III. Constrained by Sluggish Overseas Mine Output: China’s Zinc Concentrate Imports Unlikely to Rise in 2026

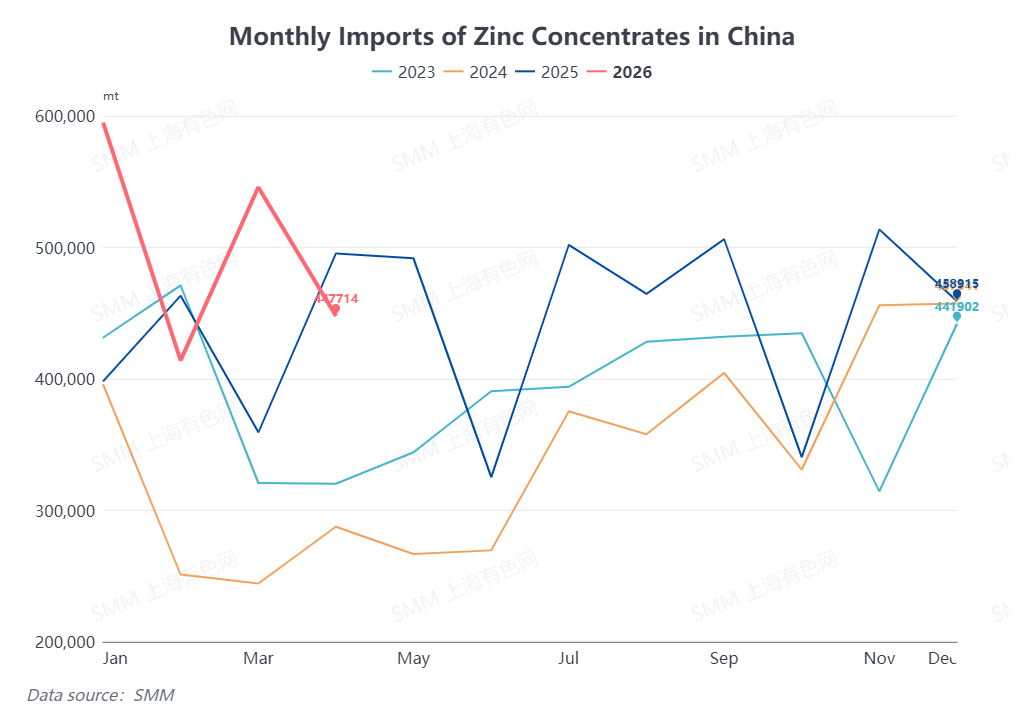

Customs General Administration data reveal China’s cumulative zinc concentrate imports hit 2.0021 million physical metric tons from January to April 2026, rising 17% year-on-year. The growth was mainly driven by climbing domestic sulfuric acid prices, which lifted profit margins for domestic smelters and sustained robust demand for imported zinc concentrate without large-scale production curtailments at domestic smelters in H1. That said, lingering logistical bottlenecks will continue to weigh on China’s zinc concentrate import volumes in Q2.

Looking ahead to H2, new domestic mine capacity releases are expected to partially offset smelter feedstock demand. Coupled with the projected year-on-year drop in global zinc concentrate output outside China, China’s zinc concentrate import volumes are unlikely to achieve year-on-year growth in the second half of the year.

Conclusion

The global zinc concentrate market is projected to stay in a tight supply-demand balance throughout 2026. Domestic and overseas zinc concentrate TCs kept sliding in H1 and both hit historic lows. Although new mine and smelter capacities will continue expanding worldwide in H2, supply-demand fundamentals are unlikely to see material improvement. The rebound potential for domestic and overseas zinc concentrate TCs will remain limited, with treatment charges set to stay persistently low for the rest of the year.

(The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided in this article is for reference only. This article does not constitute direct advice for investment research and decision-making. Customers should make cautious decisions and should not replace their independent judgment with this information. Any decisions made by customers are not related to SMM.)