Content of Anti-Dumping Investigation

On June 22, 2026, the Ministry of Commerce and Industry of India issued a notice stating that, in response to an application filed by the Indian enterprise JSW JFE Electrical Steel Nashik Private Limited, it initiated an anti-dumping investigation on cold rolled grain-oriented electrical steel (CRGO) and amorphous metal (AM) originating in or imported from China, Japan, South Korea, and Russia.

This case primarily involves products under India HS codes 72251100, 72261100, and 72269930, as well as some products under HS codes 72251920, 72251990, 72261920, 72269910, 72261990, 72269910, 72269920, and 72269990.

The dumping investigation period for this case was from April 1, 2025, to March 31, 2026 (12 months), and the injury investigation period covered April 1, 2022, to March 31, 2023; April 1, 2023, to March 31, 2024; April 1, 2024, to March 31, 2025; and April 1, 2025, to March 31, 2026.

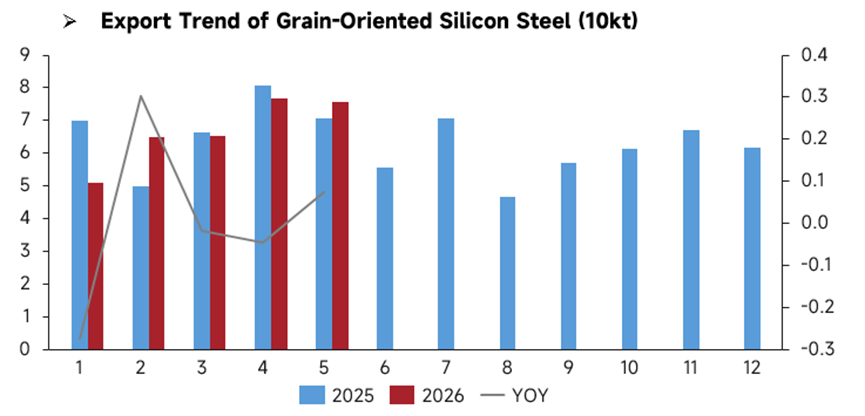

China's Grain-Oriented Silicon Steel Export Situation

Source: General Administration of Customs

Comparing grain-oriented silicon steel exports in the first five months, monthly exports in 2025 fluctuated more sharply, with a notable pullback in February and hitting a period high in April. In the first five months of 2026, monthly exports rose steadily month by month, showing a more stable trend. Total exports from January to May 2026 were similar to those in the same period of 2025, and outside China demand remained relatively stable.

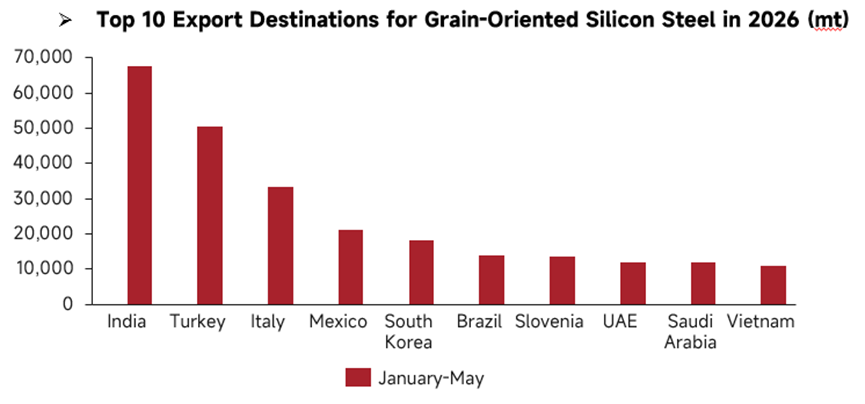

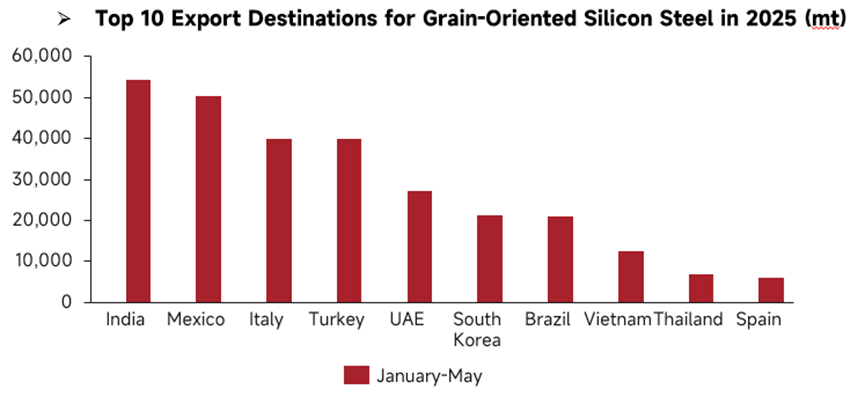

Data Source: General Administration of Customs of China

Among the top ten destinations for China’s grain-oriented silicon steel exports in the first five months of 2025 and 2026, India retained its position as the largest export market for two consecutive years, with notably strong growth. Exports to India were approximately 54,400 mt in the first five months of 2025, rising to 67,600 mt in the same period of 2026, a significant increase. Turkey’s ranking moved up considerably, while Mexico’s ranking declined. Slovenia and Saudi Arabia newly entered the top ten, while Thailand and Spain dropped out of the list. Exports to traditional markets such as Italy, Mexico, South Korea, Brazil, the UAE, and Vietnam generally pulled back YoY. Only India and Turkey achieved YoY increases, making India the sole major overseas demand center with substantial volume growth.

China exports large quantities of grain-oriented silicon steel to India, while India’s domestic grain-oriented silicon steel producers struggle to compete, prompting India to initiate an anti-dumping investigation.

Timeline Estimate for the Implementation of India’s Anti-Dumping Duties

India’s anti-dumping investigations follow a clear timeline. A preliminary determination is issued 5 to 6 months after the case is initiated, and provisional duties are imposed. For complex cases like the current grain-oriented silicon steel investigation involving multiple countries, the final determination report may take up to 18 months. After the final determination recommendation is submitted to the Ministry of Finance, an additional 3-month approval period is required. The entire process, from initiation to the imposition of definitive duties, is expected to take approximately one and a half to two years. The definitive fixed duties, once imposed, remain valid for five years. Before expiry, domestic producers may request a sunset review, which also takes 12 to 18 months, during which the existing duties remain in effect.

Relevant grain-oriented silicon steel export enterprises may negotiate price undertakings within a window of 3 to 8 months after case initiation, thereby avoiding both provisional and definitive duties.

Potential Impact of India’s Anti-Dumping Investigation on China

From Case Filing to Preliminary Ruling:

When the case filing news emerged, Indian importers would proactively adopt a wait-and-see attitude, suspend new long-term contracts, and turn to supply from Japan and South Korea, causing a contraction in orders from China to India. Relevant Chinese enterprises would also bear high litigation costs and increase compliance expenses for various documents. Small and medium-sized producers without the ability to respond to the investigation would exit the Indian market directly, while top-tier players would incur significant costs in responding.

After the preliminary ruling is issued in five to six months, provisional anti-dumping duties (for up to six months) would be directly imposed, significantly raising export costs and reducing shipments to India. Return cargo flows would pressure domestic spot prices of grain-oriented silicon steel, eroding steel mill profits. The willingness to conduct maintenance and control production would rise, sector sentiment would come under pressure, and the valuations of listed GO silicon steel enterprises would weaken.

Downstream power equipment, such as transformers and reactors exported from China to India, would also face obstacles. Bidding costs for complete equipment sets would rise, leading to the loss of orders for power grids, PV inverters, and other Indian projects. Involution in China’s domestic demand market would intensify, with low-end transformer producers cutting prices to compete for orders, simultaneously squeezing profits.

Medium to Long-Term (1-2 Years):

After the final ruling in 18 months and approval by the finance ministry, a fixed hefty tariff for five years would be implemented, representing a medium- to long-term structural shock. China would be forced to adjust its GO silicon steel capacity structure, develop alternative overseas markets, advance overseas plant construction, comprehensively reduce dependence on the single Indian market, and focus on expanding incremental grid markets in the Middle East, Southeast Asia, and Latin America, diversifying the export structure. Top-tier steel mills would go global by establishing silicon steel slitting bases and joint-venture steel mills in Southeast Asia, while transformer enterprises would simultaneously build plants outside China to circumvent finished-product tariff barriers.

International

India Market

In the short term, Indian importers are turning to sources from Japan, South Korea, and Russia, driving up procurement costs. Insufficient local capacity for low-grade silicon steel has caused raw material shortages for transformer manufacturers. Downstream power manufacturing associations are protesting the cost increases, infrastructure project quotations are rising, the power grid expansion pace is slowing, and high tariffs are raising costs across India's entire industry chain, weakening the competitiveness of its new energy and power grid infrastructure compared with Southeast Asia. In the long term, policies will continue to support local grain-oriented silicon steel projects such as JSW-JFE, with local capacity expanding significantly within five years and low-end silicon steel achieving self-supply.

Global Trade Market

Enterprises from Japan, South Korea, and Russia are seizing China's original share in the Indian market, forming supply substitution. China is shifting toward the Middle East, Southeast Asia, and Latin America, creating differentiated competitive tracks. Transformer and silicon steel processing stages are relocating to Vietnam, Indonesia, and Malaysia, forming a Southeast Asian power equipment manufacturing cluster. Third-country deep processing and origin-based tariff avoidance will become a long-term conventional trade pattern.

![[China Iron Ore Brief] Iron ore concentrate prices in the Tangshan area will likely keep consolidating.](https://imgqn.smm.cn/usercenter/FFFrV20251217171719.jpg)