Affected by copper prices fluctuations, the operating rate of China's copper cathode rod industry pulled back slightly in recent weeks, though overall performance was better than earlier expectations. Meanwhile, social inventory and enterprise finished product inventories showed diverging trends.

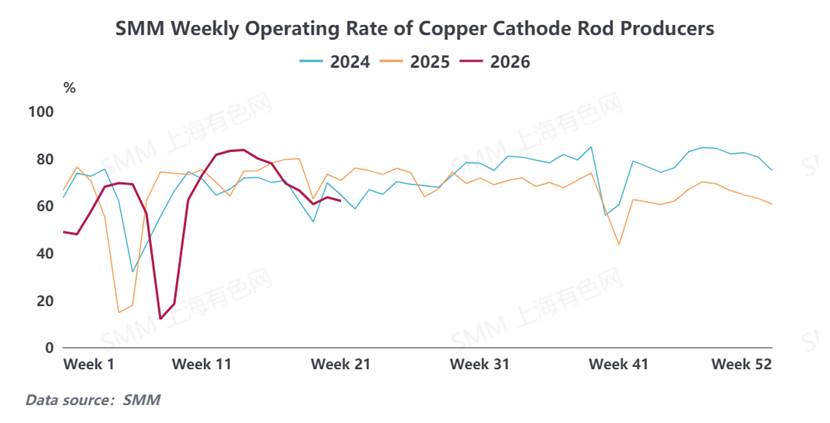

I. Operating Rate Pulled Back WoW, Actual Performance Better Than Expected

Last week (May 15–May 21), the operating rate of major copper cathode rod enterprises in China came in at 61.97%, down 1.54 percentage points WoW, but 1.12 percentage points above prior expectations, and down 8.67 percentage points YoY.

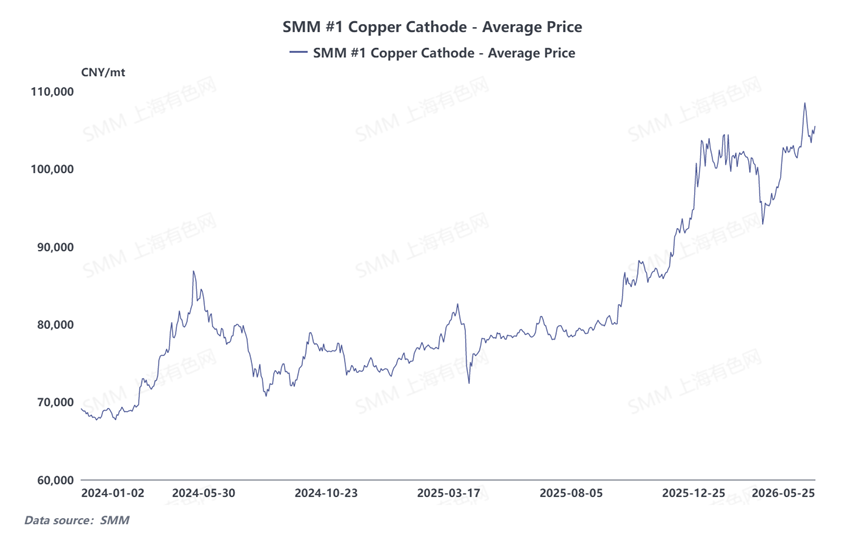

Copper prices rose first and then fell this week. The price rise phase notably suppressed downstream purchasing sentiment, with enterprises receiving fewer new orders and a slowdown in the cargo pick-up pace, leading to continuous accumulation of finished product inventories. Some enterprises proactively cut production to ease inventory pressure. As copper prices gradually pulled back, downstream enterprises began to progressively place orders and pick up goods, accelerating the pace of order delivery, which provided some support to operating rates and resulted in actual operating performance exceeding earlier enterprise expectations.

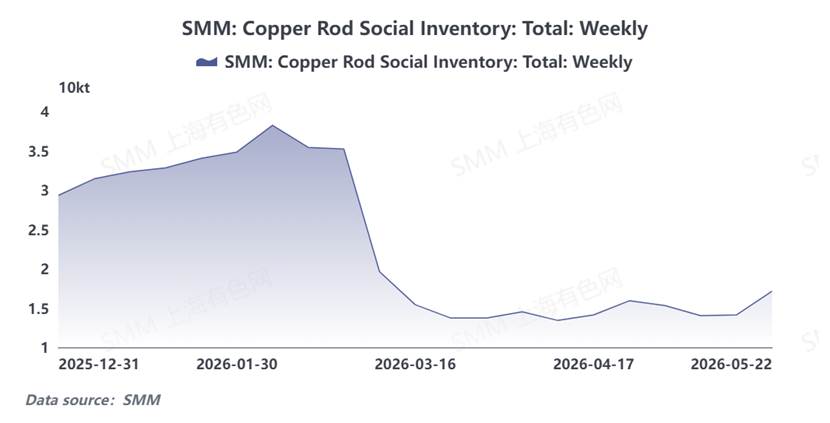

II. Divergence in Inventory Trends: Social Inventory Continued to Build Up While Enterprise Finished Product Inventory Shifted from Buildup to Slight Destocking

(i) Social Inventory Continued to Build Up but Remained at a Medium-to-Low Level Overall

From the perspective of social inventory, according to SMM weekly data on copper rod social inventory, for the week of May 22, 2026, China's total copper rod social inventory stood at 17,100 mt, having built up for two consecutive weeks. This represented a rebound from the mid-April low of 13,400 mt, but remained at a medium-to-low level overall. Inventory pressure was relatively high at the beginning of the year, with social inventory reaching as high as 38,000 mt at the end of January. In March, copper prices pulled back significantly, driving downstream demand release and a rapid decline in inventory to 14,000 mt. The overall destocking trend was notable in Q1. Entering Q2, copper prices gradually stabilized, market demand operated steadily, and inventory fluctuations narrowed accordingly.

(2) Enterprise raw material inventory fluctuations were limited, and finished product inventories saw destocking this week

Enterprise inventory side, copper cathode rod enterprises continued the purchasing as needed model for raw material procurement, flexibly adjusting according to production pace. Overall raw material inventory fluctuations were relatively small, pulling back slightly WoW. More notably, on the finished product inventories side, downstream demand recovered after copper prices pulled back, and pickup volume increased. Meanwhile, enterprises proactively cut production and prioritized digesting finished products. Last week, finished product inventories declined 3.16% WoW, and the results of production cuts and destocking became evident.

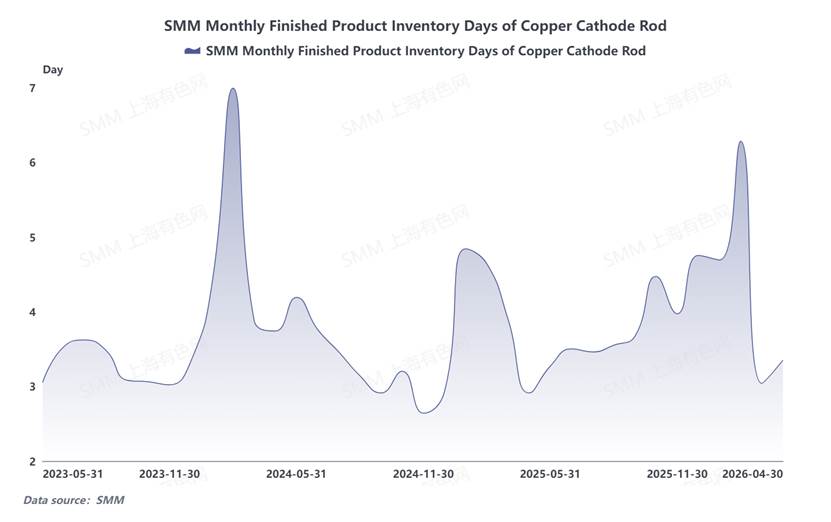

III. Monthly Days of Finished Product Inventories Continued to Rise

From a longer time horizon, SMM copper cathode rod monthly days of finished product inventories hit a cyclical peak in February. In March, copper prices pulled back sharply, new orders surged in the market, downstream cargo pick-up enthusiasm improved, and warehouse withdrawals consistently exceeded warehouse inflows, causing finished product inventories to quickly pull back to low levels. In April, copper prices fluctuated upward, downstream procurement sentiment turned cautious, the pace of cargo pick-up slowed down, and inventory buildup occurred again. Entering May, overall industry operating rates remained weak, downstream buyers only made just-in-time procurement, and cargo pick-up intensity continued to weaken. Days of finished product inventories are expected to continue rising this month.

IV. Market Outlook: Operating Rates in the Doldrums, Expected to Gradually Stabilize in the Short Term

SMM expects that the overall operating rates of copper cathode rod enterprises will maintain a fluctuating and weak trend going forward. Currently, enterprises have insufficient orders on hand, and the progress of finished product destocking has fallen short of expectations, with operating rates clearly under pressure. However, new orders have gradually materialized during the copper price pullback phase, alleviating enterprises' willingness to cut production to some extent. Meanwhile, capacity previously under maintenance has successively resumed production, also providing support for industry operating rates. Overall, copper cathode rod operating rates are expected to gradually stabilize. However, continued attention should be paid to the direction of copper prices. If copper prices continue to fluctuate at highs and suppress downstream purchasing demand, there remains a risk that operating rates may fall short of expectations.

![[Market Insight]: US–China Copper Scrap Trade Faces Structural Shift Amid Potential Export Restrictions](https://imgqn.smm.cn/usercenter/vcsIC20251217171710.jpg)