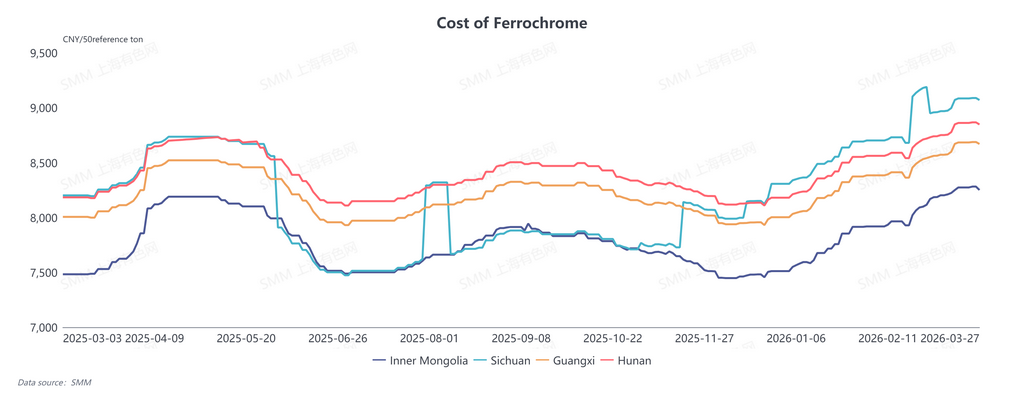

As of March 31, retail prices of ferrochrome remained stable. Quotes in Inner Mongolia stood at 8,600–8,700 yuan per 50% basic ton, while those in Sichuan were 8,650–8,800 yuan per 50% basic ton, up 100 yuan month-on-month. The price gap between northern and southern regions narrowed, yet the spread between retail and long-term contract prices remained notable. Faced with upward cost pressure from high chromium ore prices, most ferrochrome producers have planned maintenance and output cuts recently. The supply-demand relationship of ferrochrome is expected to gradually adjust to a tight balance in the outlook.

1. Costs Keep Rising, Leading to Price Inversion

At present, the spot cost of ferrochrome in Inner Mongolia has reached 8,320 yuan per 50% basic ton, and the average cost in southern China hit 8,876 yuan per 50% basic ton, rising 3.75% month-on-month. On one hand, continuous gains in raw material chromium ore prices have driven up costs; on the other hand, frequent adjustments to power policies have intensified electricity cost pressure.

Chromium Ore

Post-holiday futures and spot prices of chromium ore have kept climbing. Geopolitical conflicts in the Middle East pushed up fuel prices and ocean freight rates, with some shipping companies imposing war surcharges, significantly raising landed costs of chromium ore, while overseas futures quotes trended steadily upward. South African fine ore was quoted at 318 USD/ton, and Turkish fine ore exceeded 400 USD/ton. Meanwhile, low-priced inventories from earlier periods have been cleared. Amid high receiving costs, domestic traders hold a strong attitude of supporting and probing price increases, keeping spot chromium ore prices at high levels.

Electricity

Policy adjustments have lifted electricity costs for ferrochrome producers. In southern China (e.g., Guizhou), electricity prices rose by 0.08–0.12 yuan per kWh, pushing up costs by nearly 400 yuan; in northern China (Inner Mongolia), settlement electricity prices increased by 0.02 yuan per kWh, lifting costs by nearly 100 yuan. Shrinking profit margins have put ferrochrome enterprises in a cost-price inversion dilemma.

2. High Downstream Scheduling but Limited Demand Release

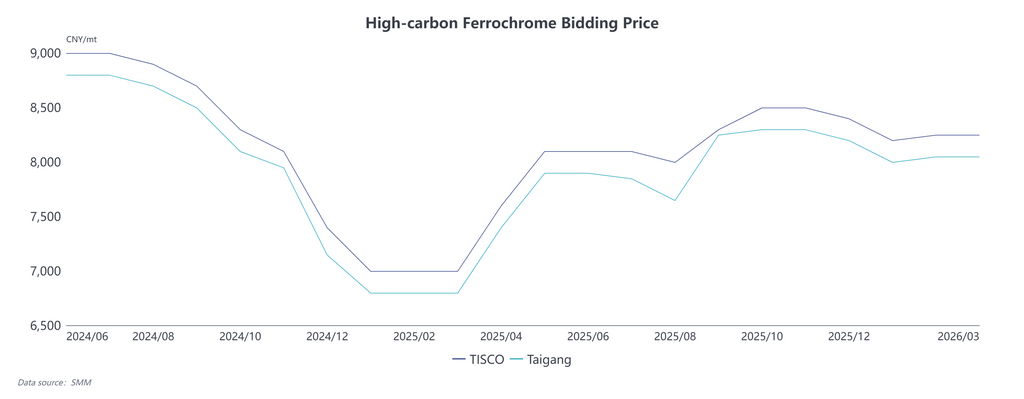

According to SMM statistics, stainless steel output in March 2026 surged 44.65% month-on-month, generating ferrochrome demand of approximately 617,500 metal tons. Although production scheduling rebounded to historical highs, purchasing activity by downstream steel mills was muted, as most consumed pre-holiday raw material inventories, resulting in thin inquiry and transaction sentiment in the ferrochrome market. Meanwhile, major steel mills set their March steel tender prices flat at 9,245 yuan per 50% basic ton month-on-month, falling short of bullish expectations amid the traditional peak consumption season of "Golden March, Silver April". Market participants lacked confidence, leading to overall weak performance during the month.

3. Industry Maintenance Plans to Tighten Future Supply

On March 20, Tsingshan and TISCO announced their April 2026 tender purchase prices for high-carbon ferrochrome at 8,395 yuan and 8,195 yuan per 50% basic ton respectively, up 150 yuan from March but below earlier bullish market forecasts. The wide spread between retail and long-term contract prices dampened market confidence. Coupled with heavy losses from soaring costs, the industry held meetings to discuss countermeasures. Some producers announced maintenance and output reduction plans, meaning China’s high-carbon ferrochrome output is likely to decline in April.

In overseas markets, negotiations over South Africa’s temporary electricity price policy have stalled. Major chromium producer Glencore stated that contract terms are unfeasible, leading to limited actual resumption of local ferrochrome production. China Customs data showed that China imported 265,100 tons of high-carbon ferrochrome in January–February 2026, down 51.6% year-on-year. It will take time for ferrochrome imports to return to average historical levels, so their impact on the domestic market will remain limited in the short term, with imports expected to stay low.

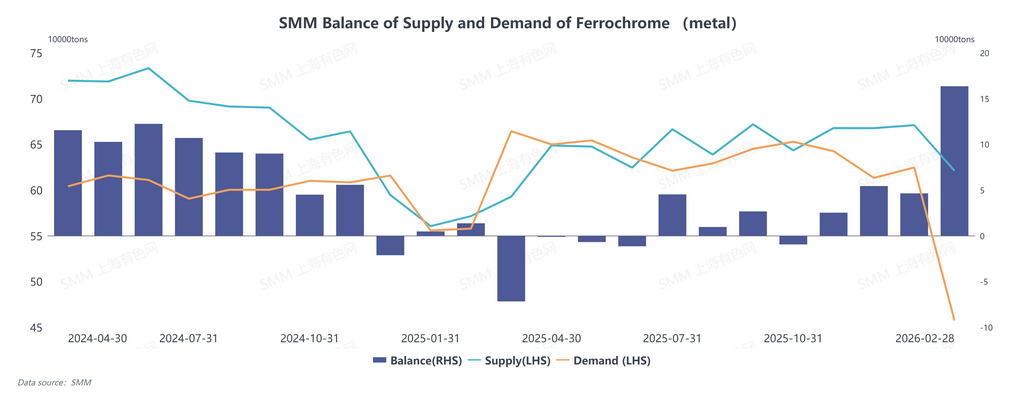

Overall, while downstream stainless steel maintains high production scheduling, ferrochrome supply is set to tighten. China’s ferrochrome supply-demand relationship is forecast to gradually shift from surplus around the Spring Festival to a tight balance.