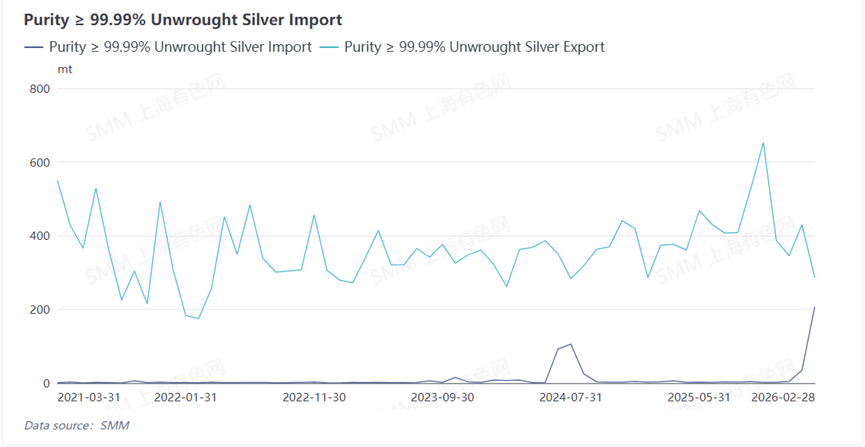

The latest customs data showed that in February 2026, China’s imports of unwrought silver ingots with a purity of no less than 99.99% reached 206.76 mt, up 499% MoM and surging 5,910% YoY to a multi-year high. The rare opening of the import window drove significant changes in the supply-demand pattern of the domestic silver ingot market.

I. Drivers Behind the Import Surge

The sharp increase in silver ingot imports in February resulted from the combined effect of multiple factors:

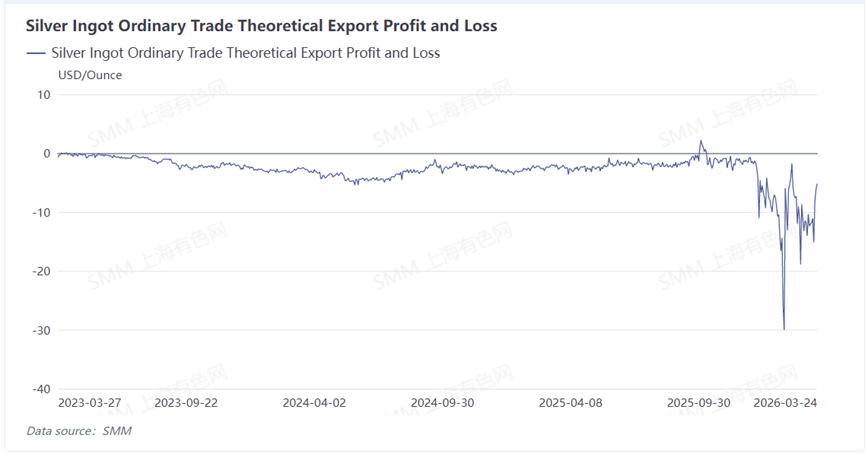

The arbitrage window created by the price spread opened. There were significant differences in rigid industrial demand for physical silver ingots and spot prices in and outside China, and the import window remained steadily open, creating favorable arbitrage conditions.

Reflows of silver ingots under processing trade. Spot silver ingots exported by domestic smelters under processing trade licenses were turned into inventory in the Hong Kong market and, instead of being shipped to Europe and the US, were directly re-imported by traders into the Shenzhen market.

Bottlenecks in crude silver processing capacity. Early imports mainly consisted of crude silver and silver-bearing raw materials, but idle domestic crude silver processing lines had limited capacity. Smelters prioritized their original production schedules, while new toll processing orders for crude silver were pushed back, delaying the entry of refined silver processed from imported crude silver until late February or even March.

II. Structural Changes in the Spot Market

The large inflow of imported silver ingots had a profound impact on China’s spot market. According to SMM data, silver T+D prices on the Shanghai Gold Exchange (SGE) saw wild swings in Q1 2026, with spot premiums fluctuating sharply as well:

| Time Average | Premium (yuan/kg) | Remarks |

| January | 304.25 | Remained at a low level |

| February | 2,018.21 | Peaked at 3,650 |

| March | 907.5 | Pulled back rapidly |

| Late March | <100 Narrowed sharply |

III. Outlook for the Import Trend in March-April

Imports remained high in March. According to SMM’s market survey, supported by the price spread between domestic and overseas markets and high spot premiums in China, the import window remained open. In early March, traders were still placing large forward orders for imported silver ingots, and March imports are expected to remain at a relatively high level.

Imports are expected to decline in April. The driving factors include:

Weaker support from industrial demand. Orders related to the PV export rush were nearing an end, and PV silver powder and silver paste producers focused on exports reduced their orders. In late March, rigid demand for raw material procurement from silver nitrate enterprises declined, and industrial consumption briefly entered the off-season. Narrowing premiums compressed profits. Investment and industrial demand cooled in tandem in the short term, high spot premiums in China came to an end, and import profits fell sharply. By late March, the market had shifted from "hard to secure any cargo" to "no buyers at all," with suppliers forced to cut premiums to sell off cargo, and spot premium quotes returning to rational levels.

The pace of processing trade exports adjusted. As imported silver ingots and silver-bearing raw materials continued to flow in, tight spot supply in China eased, and premiums pulled back. Smelters that had slowed exports from January to February and prioritized domestic supply had already prepared to execute processing trade manuals after the import window closes. Although current prices on the Shanghai Gold Exchange (SGE) still carry a premium over LBMA spot prices, some smelters remained cautiously on the sidelines, and adjustments to the export pace may be delayed until May.

IV. Outlook for the Market

SMM analysis suggests that the logic of interest rate cut cycles supporting precious metals prices has changed, and the short-term difficulty of ending the U.S.-Iran conflict may keep precious metals under pressure, with investment demand cooling significantly, while the spot market is expected to return to being driven by industrial demand in the short term. In addition, both the Shanghai Gold Exchange (SGE) and CME outside China have repeatedly raised margin requirements for silver contracts to guard against risks, and there are currently no expectations for cuts. Stronger regulatory measures have raised the threshold for speculative capital to enter the market, and silver price fluctuations are expected to become more stable.

![Silver Prices Rebounded and Rose, Downstream Buyers Remained Cautious and Wait-and-See, and Transactions Softened [SMM Daily Review]](https://imgqn.smm.cn/usercenter/JYbQQ20251217171736.jpg)