The following combines SMM data and market dynamics to provide a detailed review of April's electrolyte and battery cell market performance, compare with cathode and anode trends, summarize the current landscape, and look ahead at future trends.

I. Sodium-Ion Battery Electrolyte: Steady Shipments Demonstrate Resilience, Capacity Gap Becomes Potential Constraint

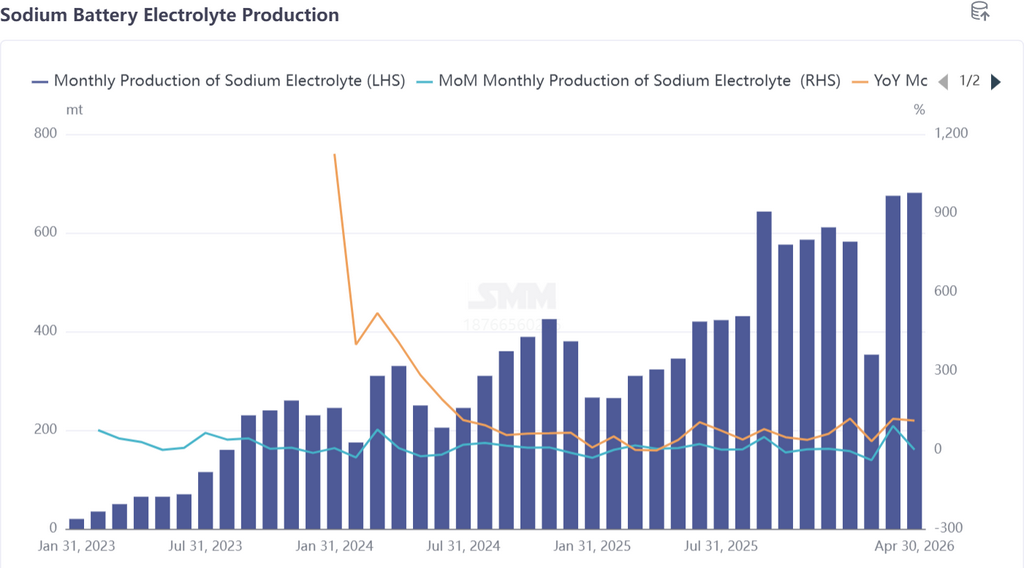

According to SMM data, sodium-ion battery electrolyte production in April was up 1% MoM and up 111% YoY, with the overall market operating steadily without wild swings.

The current sodium-ion battery electrolyte market remains dominated by top-tier players, with core enterprises sustaining shipments and stabilizing supply, fully ensuring supply chain stability for downstream battery cell enterprises, serving as the core pillar of the industry's steady operation.

However, at the same time, downstream battery cell manufacturers, driven by cost control needs, continued to pressure electrolyte procurement prices, further squeezing the profit margins of electrolyte enterprises, with the industry presenting a trend of "stable volume under price pressure."

In stark contrast to the accelerating capacity release of cathode and anode materials, the current supply capability of sodium-ion battery electrolyte still has notable shortcomings. SMM analysis suggests that based on the current production scale of sodium-ion battery cells and medium and long-term expansion plans, a supply-demand gap already exists for sodium-ion battery electrolyte, and this gap is likely to widen further as battery cell capacity expands.The core reason is that current sodium-ion battery electrolyte capacity relies heavily on surplus capacity from existing lithium battery electrolyte production, with most electrolyte enterprises paying insufficient attention to the sodium-ion battery segment and failing to deploy dedicated capacity, resulting in supporting capacity unable to match future battery cell expansion demand. From an industry development perspective, electrolyte is gradually becoming another significant bottleneck constraining the scaled advancement of the sodium-ion battery industry, following hard carbon anode materials. Looking ahead to May, as downstream battery cell capacity is released and demand increases, sodium-ion battery electrolyte production is expected to grow in tandem.

According to SMM's forecast, sodium-ion battery electrolyte production in May is expected to increase 12% MoM and surge 120% YoY. However, the capacity gap issue is unlikely to be fundamentally resolved in the short term, and prices are expected to remain stable.

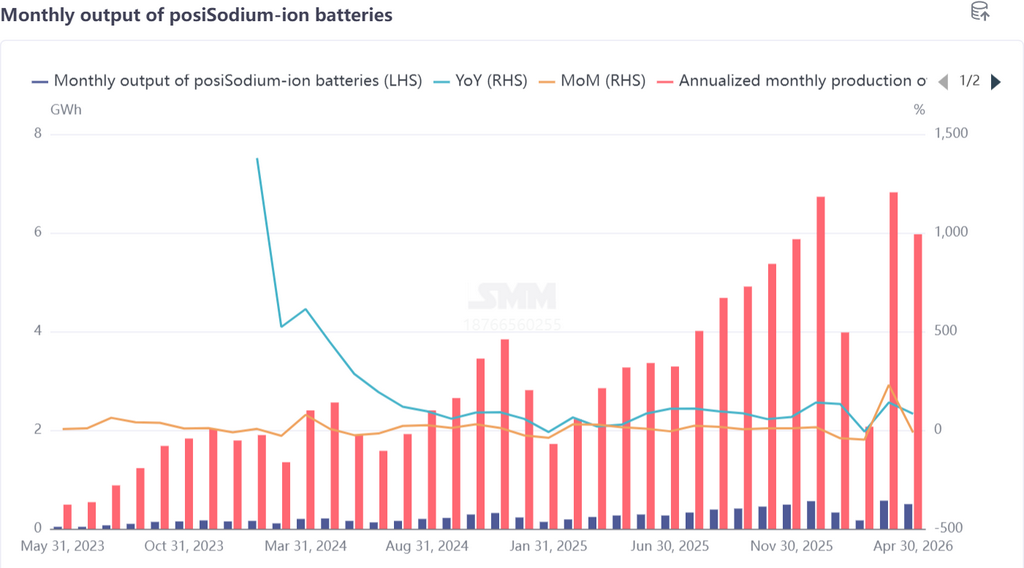

II. Battery Cells and End-Users: Consolidating for a Breakthrough, with Volume Ramp-up Expected in Q2

In April, the sodium-ion battery cell market exhibited a trend of "short-term adjustment with long-term positive outlook." According to SMM data, sodium-ion battery cell production in the month declined 12% MoM while rising 83% YoY.

The slight MoM decline in production was not due to weak demand, but rather the result of enterprises reallocating and adjusting their existing capacity and orders — most enterprises, in preparation for new capacity commissioning in Q2 and subsequent energy storage project deliveries, used April as a consolidation period to optimize production processes, align material supply, and prepare for subsequent volume ramp-up.

April Sodium-Ion Battery Electrolyte & Battery Cell Market Review: Steady Momentum Building Ahead of Breakout, Bottlenecks and Opportunities Coexist

From the accelerating capacity of cathode and anode materials and recovering demand, to the steady momentum building in electrolyte and battery cells, the sodium-ion battery industry chain in April exhibited distinct characteristics of "upstream-downstream coordination with differentiated performance." According to SMM data, compared with the rapid growth of cathode and anode materials, the electrolyte and battery cell markets maintained high YoY growth but were affected in the short term by factors such as cost control,capacity alignment, and the pace of end-use demand release, presenting an operational landscape of "stability with adjustments." As the core supporting and end-user delivery segments of the sodium-ion battery industry chain, the development of both directly relates to the industry's commercialization progress. The following combines SMM data and market dynamics to provide a detailed review of April's electrolyte and battery cell market performance, compare with cathode and anode trends, summarize the current landscape, and look ahead at future trends.