April 10, 2026:

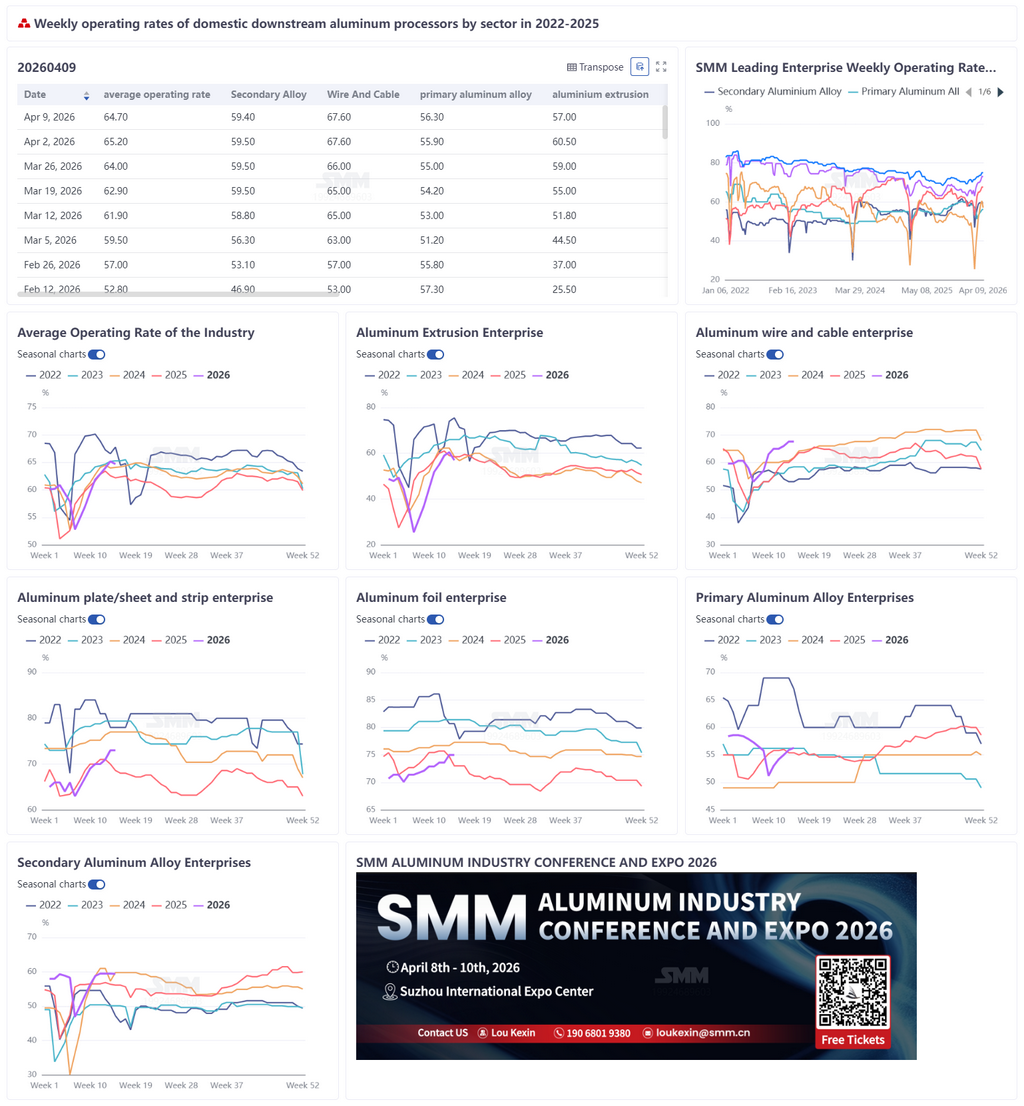

This week, the weekly operating rate of China's leading aluminum downstream processing enterprises pulled back 0.5 percentage points WoW to 64.7%. The industry continued its weak recovery pattern, with divergence among segments intensifying. The operating rate of primary aluminum alloy rose 0.4 percentage points to 56.3%, as inventory digestion drove production resumptions, but sluggish demand and cautious procurement constrained the pace. Operating rates of aluminum plate/sheet and strip and aluminum foil stayed high at 73% and 75% respectively, supported by can stock packaging, energy storage, and battery foil orders, though air-conditioner foil recovery was hindered by policy headwinds and a sluggish property market. The aluminum wire and cable operating rate held flat at 67.6%, underpinned by power grid infrastructure but constrained by high inventory and slower cargo pick-up. Aluminum extrusion pulled back 2 percentage points to 57%, with the construction segment suppressed by high aluminum prices and industrial materials dragged down by shrinking PV frame orders. Secondary aluminum edged down 0.1 percentage points to 59.3%, as insufficient consumption recovery prompted enterprises to cut production to manage inventory. Currently, core demand support came from energy storage and new energy segments, but elevated aluminum prices, peak-season demand falling short of expectations, and Middle East export disruptions constrained traditional sectors and export recovery. The aluminum processing industry exhibited characteristics of "slow recovery, underperforming in peak season." Short-term upside room for operating rates remained limited, and operations are expected to run steadily next week. Attention should be paid to the marginal impact of post-holiday orders, aluminum prices, and export policy changes on each segment.

Primary aluminum alloy: This week, the operating rate of primary aluminum alloy edged up 0.4 percentage points to 56.3%, with the industry overall continuing a slow recovery trend. In terms of supply, long-term contract delivery volumes remained stable and enterprise production was largely normal. Some enterprises resumed production after depleting a certain amount of inventory in the prior period, driving the operating rate to rebound. Demand side, downstream overall showed a stable but slow growth trend, though actual performance fell short of market expectations. Affected by geopolitical factors, aluminum prices continued to fluctuate at highs, and downstream procurement generally turned cautious. Overall, the industry was gradually recovering, but the pace remained slow. The primary aluminum alloy operating rate is expected to continue edging up slightly next week.

Aluminum plate/sheet and strip: This week, the operating rate of leading aluminum plate/sheet and strip enterprises registered 73%. At the enterprise operation level, the aluminum plate/sheet and strip market performed steadily during the week, with leading enterprises maintaining orderly production and no notable fluctuations in overall production pace. Domestic can stock packaging demand remained stable, providing fundamental support for operating rates. On NEV consumption, as consumers gradually adapted to the tax normalization for NEVs, the new energy market and related material orders are expected to gradually return to a positive growth trajectory. Energy storage end-users maintained relatively high operating rates, with some enterprises accelerating production schedules to ensure deliveries, bringing additional support for energy storage-related battery casings, brazing materials, and other aluminum plate/sheet and strip products. On the export side, although Iran and the US temporarily reached a two-week ceasefire agreement, the Strait of Hormuz was not substantively opened, and export orders remained in a wait-and-see state. In the short term, the operating rate of leading aluminum plate/sheet and strip enterprises is expected to continue running steadily at highs.

Aluminum wire and cable: This week, the weekly operating rate of China's aluminum wire and cable industry rose to 67.6%, flat WoW. Concentrated release of power grid orders supported capacity utilization rate at highs, but the inventory buffer formed by high-load production in March meant that in-plant finished goods could meet short-term cargo pick-up needs, and operating resilience was actually constrained by changes in terminal cargo pick-up pace. Currently, aluminum prices fluctuating at highs combined with heightened macro sentiment uncertainty led enterprises to turn cautious in procurement, primarily focusing on digesting inventories. In the short term, the operating rate may remain elevated underpinned by power grid infrastructure demand, with subsequent attention on the pace of inventory drawdown and order sustainability.

Aluminum extrusion: This week, the operating rate of China's aluminum extrusion industry was 57%, down 2 percentage points WoW. The construction extrusion segment was generally stable with weakening trend. Some enterprises in Shandong and Jiangsu reported that with aluminum prices staying high, downstream wait-and-see sentiment was strong, procurement pace slowed, and related enterprises' operating rates edged down. Industrial extrusion side, end-use demand in new energy and power sectors remained solid, but PV frame enterprises in Anhui and Shandong reported that due to the impact of demand being front-loaded in April, orders contracted and operating rates pulled back. Looking ahead, end-use demand is expected to maintain a recovering trend, but elevated prices combined with wild swings in aluminum prices suppressed downstream procurement enthusiasm. The aluminum extrusion operating rate is expected to remain generally stable with slight fall in the short term.

Aluminum foil: This week, the operating rate of leading aluminum foil enterprises registered 75%. At the enterprise operation level, as the traditional peak season deepened, leading enterprises had ample orders on hand, production pace was steady, and major downstream aluminum foil cargo pick-up accelerated, with overall production activity relatively high. Orders showed clear divergence: food packaging foil and battery aluminum foil demand remained in peak season, firmly supporting the base operating rate; single zero foil orders were sufficient with high output efficiency, and April production schedule expectations strengthened. Air-conditioner foil side, April household air conditioner domestic sales production schedules edged down slightly, affected by diminishing government subsidy policy effects, elevated raw material costs, and sluggish property completions, further dragging on the recovery pace of air-conditioner foil demand. Combined with depressed air-conditioner foil processing fees, some enterprises proactively scaled back this business and shifted toward the packaging segment. In the short term, supported by traditional peak-season packaging orders and driven by new energy battery demand, the aluminum foil operating rate is expected to run steadily.

Secondary aluminum: This week, the operating rate of leading secondary aluminum alloy enterprises edged down 0.1 percentage points WoW to 59.3%. Since April, end-use consumption recovery fell short of expectations, downstream procurement sentiment was cautious, and enterprises proactively adjusted production through phased production cuts, maintenance shutdowns, and other measures to ease inventory accumulation pressure. Cost and profit side, primary aluminum prices were in the doldrums, aluminum scrap prices were relatively resilient, and cost side downside room was limited. Meanwhile, weakening demand dragged finished product prices continuously lower, further compressing industry profit margins and significantly weakening support for high operating rates, with enterprises turning cautious in production mindset. Overall, insufficient short-term order release will continue to constrain production pace. The industry operating rate is expected to remain generally stable with slight fall, with the possibility of minor downward adjustments.