SMM, March 20:

Imports: According to data from the General Administration of Customs, China’s primary aluminum imports were about 189,000 mt in January, down 0.1% MoM and up 17.1% YoY; in February, China’s primary aluminum imports were about 202,000 mt, up 6.6% MoM and up 0.7% YoY. In January-February 2026, China’s cumulative primary aluminum imports totaled about 391,000 mt, up 8.0% YoY.

Exports: According to data from the General Administration of Customs, China’s primary aluminum exports were about 13,000 mt in January, down 64.6% MoM and up 56.6% YoY; in February, China’s primary aluminum exports were about 10,000 mt, down 24.6% MoM and up 187.9% YoY. In January-February, cumulative primary aluminum exports totaled about 23,000 mt, up about 94.8% YoY.

Net imports: According to data from the General Administration of Customs, China’s net primary aluminum imports were 176,000 mt in January, up 15.9% MoM and up 14.9% YoY; in February, China’s net primary aluminum imports were 192,000 mt, up 9.0% MoM and down 2.6% YoY. In January-February, China’s cumulative net primary aluminum imports were about 367,000 mt, up 5.0% YoY.

(The above import and export data are based on HS codes 76011090 and 76011010.)

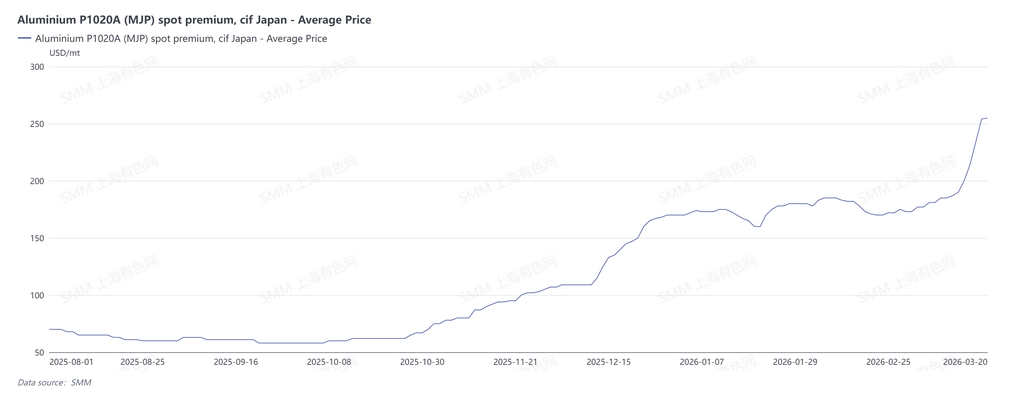

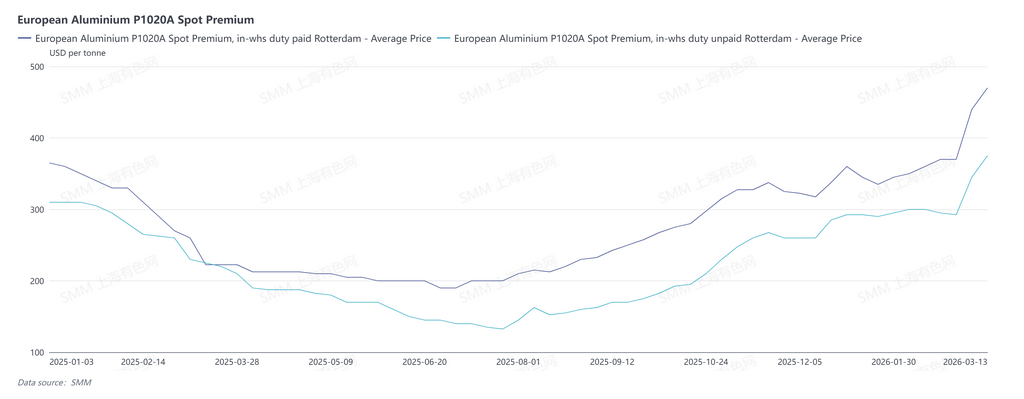

Although China’s net primary aluminum imports maintained positive growth in January-February 2026, expectations of a sharp rise in regional aluminum premiums outside China will challenge this situation. As of March 20, SMM’s Japan MJP spot premiums for aluminum ingot stood at $255/mt, up 45.7% from month-end February. Currently, some market participants were quoting Japan MJP CIF premiums for Q2 at around $350-353/mt, up about 80% from $195/mt in Q1; the US Midwest DDP aluminum premium stood at 105.25¢/lb, equivalent to $2,110/mt. As of March 13, Europe’s P1020A aluminum ingot duty-paid premiums stood at $470/mt, up about 27.0% from month-end February, while Europe’s P1020A aluminum ingot duty-unpaid premiums stood at $375/mt, up 27.2% from month-end February. The sharp rise in regional aluminum premiums outside China is expected to divert some aluminum originally planned to flow into China, and China’s net aluminum imports are expected to decline YoY in 2026. The reason for this phenomenon lies in expectations of a contraction in aluminum supply outside China caused by reduced aluminum supply in the Middle East. As of March 20, Qatar Aluminum announced that it would maintain a 60% operating rate, involving 260,000 mt of shut capacity; Bahrain Aluminum announced the shutdown of Lines 1-3, involving about 310,000 mt of capacity. In total, 570,000 mt of aluminum capacity in the Middle East has been affected. Iran is at the center of the conflict, and the stability of its production faces severe challenges.

In addition, some raw and auxiliary materials in the Middle East rely on imports, and the geopolitical conflict in the region has affected passage through the Strait of Hormuz, to some extent undermining raw material supply stability at certain aluminum plants. At present, aluminum plants in Saudi Arabia and Turkey have domestic upstream bauxite and alumina support and can achieve self-sufficiency, with room for exports; Bahrain Aluminum and Qatar Aluminum rely entirely on imported alumina, while the UAE has 2.5 million mt of alumina capacity, but its bauxite relies 100% on imports. Although Oman’s aluminum plants also depend on imported raw materials, their geographic location is outside the Strait of Hormuz, so the level of risk is relatively low. If transport routes remain closed and no new routes can be opened, aluminum production in the Middle East is expected to be significantly affected.

However, according to the latest foreign media reports, Bahrain Aluminum is exporting 40-60% of its aluminum ingots through Saudi Arabia’s Port of Jeddah, with an overland transport distance of 1,400 kilometers, and UAE’s Emirates Global Aluminium is attempting to import alumina raw materials through ports in Oman. If new transport routes are opened, the production reduction risk at aluminum plants in the Middle East is expected to decline markedly.

Going forward, continued attention should be paid to production developments at aluminum plants in the Middle East, transport route conditions, and trends in LME aluminum inventory.

![Inventory fluctuated downward as increased warehouse withdrawals accelerated destocking, and recovering consumption drove processing fees back above parity [SMM Aluminum Billet Weekly Review]](https://imgqn.smm.cn/usercenter/LfGaw20251217171654.jpg)

![Impact of Hormuz Blockade on China's Aluminum Wire and Cable Exports to the Middle East [SMM Analysis]](https://imgqn.smm.cn/usercenter/zlIyw20251217171654.jpg)