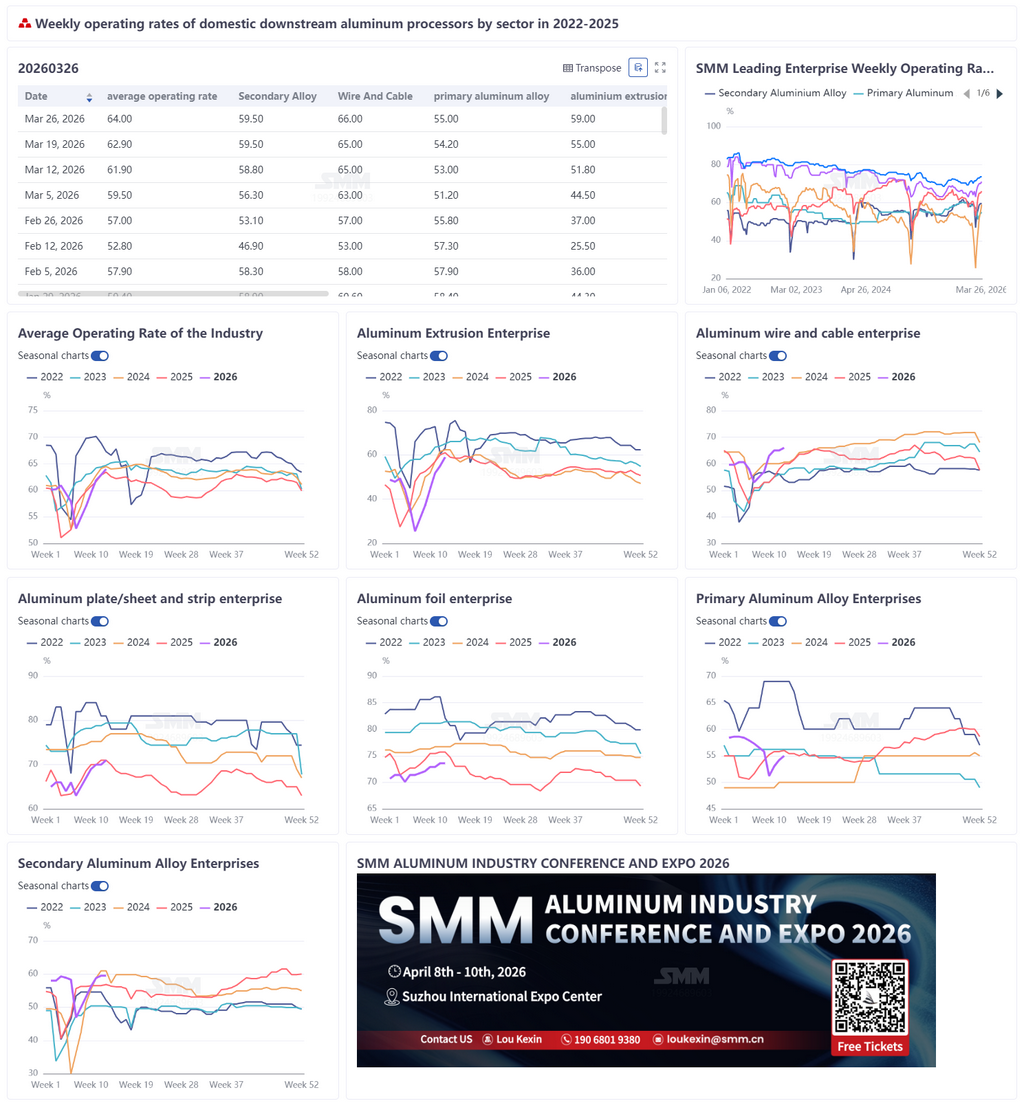

March 27, 2026:

This week, the weekly operating rate of leading downstream aluminum processing enterprises in China rebounded 1.1 percentage points MoM to 64%. Operating rates across segments showed differentiated recovery, and consumption gradually returned to the peak-season pace, but the overall level still lagged behind the same period last year, with the strength of demand recovery intertwined with disruptions from the macro environment. The operating rate of aluminum wire and cable rose 1 percentage point MoM to 66%, improving steadily, as robust stockpiling demand for power grid construction was reinforced by the accelerated implementation of UHV and power transmission and transformation projects; the operating rate of aluminum plate/sheet and strip rose to 71%, with energy storage demand underpinning market stability. Automotive sheet orders improved MoM but remained weak YoY, while a fivefold surge in Middle East export freight rates capped incremental growth. In the short term, the market may maintain fluctuating trend, with limited recovery in consumption, and peak-season performance remained weaker than in the same period in previous years; the operating rate of aluminum foil held steady at 73.6%, as the traditional peak season resonated with short-term demand for battery foil. Food packaging foil and pharmaceutical foil supported the fundamentals, but battery foil production schedules slowed ahead of the tax rebate policy switch; the operating rate of aluminum extrusion increased 4 percentage points to 59%, as construction demand saw a mild recovery following the pullback in aluminum prices, while new energy and power-sector orders on the industrial side provided clear support. Newly commissioned production lines contributed incremental output, but wait-and-see sentiment among end-users persisted, the pace of peak-season recovery remained mild, and YoY consumption had yet to recover to last year’s level; the operating rate of secondary aluminum was flat at 59.5%, as peak-season orders fell short of expectations. Downstream margins remained under pressure, while hindered exports to the Middle East created a dual drag. Procurement stayed cautious, enterprises lacked motivation to resume production, and the slope of consumption recovery remained gentle, underperforming the same period last year; the operating rate of primary aluminum alloy rose to 55%, as production line resumptions lifted output, supported by mild end-use growth. However, transactions were hindered by aluminum price fluctuations, and weak downstream inquiries limited further gains, leaving peak-season consumption recovery relatively weak. Overall, most segments of the aluminum processing industry saw operating rates recover under the drive of work resumptions, but amid uncertainty over aluminum price trends and a slow demand recovery, consumption has returned to the peak-season pace while actual strength remained below the same period last year, and the sustainability of downstream orders still requires further confirmation.

Primary Aluminum Alloy: This week, the operating rate of the primary aluminum alloy industry edged up 0.8 percentage points to 55%, showing an overall trend of slow recovery. Producers were steadily raising operating levels in succession. After earlier inventory was digested to some extent, enterprises began increasing output to deliver long-term contract orders. End-use consumption maintained mild growth, providing some support for current production. However, a sharp rebound in the operating rate remained constrained, mainly due to recent wild swings in aluminum prices. Aluminum prices pulled back over the previous two days, and some downstream enterprises hoped to procure through futures-based pricing, but primary aluminum alloy enterprises resisted selling at low prices and were unwilling to concede margins on products with high production costs, resulting in hindered transactions. In addition, downstream trader inquiry activity was clearly weaker than before the Chinese New Year, further limiting room for improvement in the operating rate. The overall operating rate is expected to continue its slow recovery next week.

Aluminum Plate/Sheet and Strip: This week, the operating rate of leading aluminum plate/sheet and strip enterprises rose 1 percentage point MoM to 71%. At the operating level, the aluminum plate/sheet and strip market remained stable during the week, and leading enterprises maintained steady production; on the end-use consumption side, downstream demand from energy storage remained robust, and leading battery cell enterprises maintained high capacity utilization rates, mainly focused on securing supply under long-term agreements. Although spot order deliveries were relatively tight, they still supported demand for aluminum plate/sheet and strip materials used in energy-storage-related battery casings and brazing materials. Affected by the policy switch and the Chinese New Year, automotive sheet orders improved from early March on a MoM basis, but still appeared weak compared with the same period last year. On exports, COSCO Shipping resumed Middle East booking from March 25, but freight rates surged fivefold. Combined with the fact that Ramadan had just ended in the Middle East and sellers and buyers remained relatively cautious in trading, export recovery was slow. In the short term, the aluminum plate/sheet and strip market is expected to remain stable, but operating rates will be difficult to climb further due to constraints from aluminum price fluctuations, automotive orders, and Middle East exports.

Aluminum Wire and Cable: This week, the weekly operating rate of China’s aluminum wire and cable industry reached 66%, up 1 percentage point MoM, showing a steadily improving trend. The sector is currently in a critical period for stockpiling for power grid construction, and with UHV and power transmission and transformation projects accelerating, peak-season demand characteristics have become increasingly evident. Downstream purchasing enthusiasm remained high, cargo pick-up pace tightened, and aluminum rod raw materials needed to be booked 2-3 days in advance, with the tight supply pattern continuing. The pace of major project advancement accelerated this year, including the start of construction on the Mengxi-Beijing-Tianjin-Hebei ±800 kV UHV project and the resumption of the Datong-Huailai-Tianjin South 1,000 kV project, together with the intensive advancement of 500 kV and 200 kV power transmission and transformation projects, all of which significantly released demand for aluminum wire and cable. As power grid order tenders gradually become clearer and project execution deepens, the industry’s high prosperity is expected to continue, and the operating rate is expected to maintain an upward trend.

Aluminum Extrusion: This week, the operating rate of China’s aluminum extrusion industry was 59%, up 4 percentage points MoM and down 2 percentage points YoY. In construction extrusion, some enterprises in Shandong reported that falling aluminum prices had provided some boost to construction market demand, with downstream orders increasing MoM. In industrial extrusion, enterprises in Fujian, Hunan, and other regions reported solid recent demand from new energy sectors such as automobiles and batteries, driving up operating rates at related enterprises. Among them, a newly built production line at one enterprise in Fujian has already started operation, mainly producing battery end plates. In addition, some extrusion enterprises in Shandong said that orders related to power applications such as power pipelines and transformers performed well, supporting their operating rates. Looking ahead, the construction extrusion market is expected to continue its gradual recovery, though the pace is likely to remain mild; supported by sustained improvement in demand for industrial extrusion, especially in the new energy sector, the overall operating rate of the aluminum extrusion industry is expected to remain stable and improve.

Aluminum Foil: This week, the operating rate of leading aluminum foil enterprises held steady MoM at 73.6%. At the operating level, amid the traditional peak season in March, demand for multiple aluminum foil products recovered, leading enterprises had ample orders on hand, and production pace remained stable. On the order side, demand for food packaging foil and pharmaceutical foil remained in peak season, supporting the fundamentals of operating rates; driven by the tax rebate policy, demand increased, and the rush to export among small battery cells was notable. Battery foil demand was boosted in the short term by the installation rush and export rush in batteries, but as the April 1 policy implementation date approached, some battery foil plants had already slowed the production schedule for this portion of orders. On processing fees, amid the strong battery foil market, some double zero foil producers switched production lines to battery foil, and the processing fee for double zero packaging foil (ordinary pouch) has risen by about 800-1,000 yuan/mt so far this year. In the short term, supported by the traditional peak season and energy storage demand, the operating rate of aluminum foil is expected to remain steady.

Secondary Aluminum: This week, the operating rate of leading enterprises in the secondary aluminum industry held steady MoM at 59.5%. The recovery pace of demand in the peak season fell short of expectations, and new orders were insufficient. Some downstream enterprises still faced margin pressure and remained highly sensitive to raw material prices, with procurement mainly based on immediate needs and weak willingness to stockpile. Meanwhile, some die-casting enterprises exporting to the Middle East saw orders decline significantly due to hindered transportation, and temporarily suspended or cut production, dragging on shipments from upstream secondary aluminum plants. Overall, weaker-than-expected downstream demand recovery combined with wild swings in aluminum prices led to fewer new orders and low production enthusiasm among enterprises, leaving insufficient momentum for a rebound in operating rates. In the short term, the operating rate of leading enterprises is expected to remain largely stable, and close attention should be paid to the pace of downstream order release and changes in raw material circulation.