SMM March 2 Update:

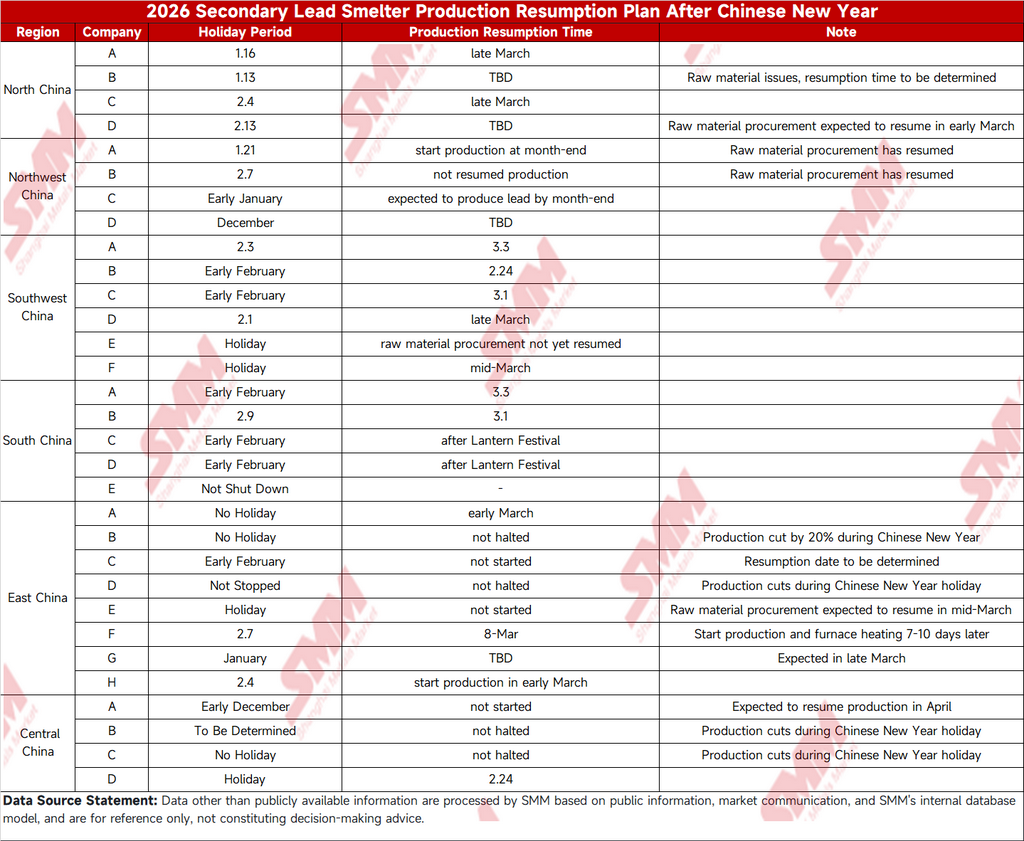

After the 2026 Chinese New Year, the overall resumption progress of domestic secondary lead smelters was slow, with the pace of production resumptions lagging significantly behind the same period in previous years. According to SMM survey data, most enterprises in core production areas such as North China, Northwest China, and Southwest China scheduled their resumption times for mid-to-late March, with some even postponing until April. Tight raw material supply, weak demand, and cost pressure collectively constrained the resumption process.

From an enterprise perspective, companies like 1, 3 in North China, and 9, 12 in Southwest China, set their resumption times for late March. Company 7 in Northwest China is expected to produce lead by the end of March, while companies 2, 4, 8, and others have yet to determine their resumption times due to raw material issues. Some enterprises in East China and Central China, although not completely shut down, adopted production cuts during the holiday, with companies 21, 23, 29, and others maintaining low-load operations. Overall, less than 30% of the smelters had clearly resumed production by the end of February, with most still in a wait-and-see mode.

The key factors constraining resumption are mainly threefold:

1. Weak Demand: Export orders for lead-acid batteries fell short of expectations, and domestic consumption recovery was sluggish. Downstream battery enterprises were not actively resuming operations, leading to low purchase willingness for lead ingots and high finished product inventories at smelters, resulting in insufficient production motivation.

2. Raw Material Constraints: Most waste lead-acid battery recyclers and stores only resumed operations after the Lantern Festival, leading to limited scrap battery supply. Coupled with the significant digestion of raw material inventories during the holiday, the current raw material supply is tight, limiting the willingness of enterprises to resume production.

3. Cost Pressure: In some regions, lower temperatures led to higher energy costs. Additionally, the weak trend in lead prices compressed profit margins, further reducing the enthusiasm for resumption.

Looking ahead, as downstream battery enterprises gradually resume operations and the scrap battery recycling market recovers in mid-to-late March, the pace of resumption for secondary lead smelters is expected to accelerate. However, before a significant improvement in demand, the overall operating rate of the industry will remain low, and the rebound in production may fall short of expectations.

![Overseas Geopolitical Risks Escalate LME Lead Overall Center of Operation Shifts Downward [SMM Lead Morning Brief]](https://imgqn.smm.cn/usercenter/guTSZ20251217171722.jpg)

![Lead Ingot Destocking Boosts Lead Prices While Geopolitical Risks Persist [SMM Lead Morning Meeting Summary]](https://imgqn.smm.cn/usercenter/xVUpr20251217171722.jpg)

![[Analysis: With the End of Chinese New Year, How Will Primary Lead Enterprises' Production Fare in March?]](https://imgqn.smm.cn/usercenter/hrxHx20251217171721.jpeg)