I. Core Takeaways and Policy Review

In Q1 2026, China’s aluminum semis exports showed a clear pattern of product differentiation amid the combined impact of three factors: the long-term effects of the export tax rebate cancellation policy introduced in December 2024, diverging demand structures in markets outside China, and the sudden outbreak of geopolitical conflict in the Strait of Hormuz. Aluminum wire and cable exports led strongly in YoY growth, aluminum plate/sheet and strip maintained high YoY growth but are expected to come under pressure later, aluminum foil edged down slightly YoY and was notably affected by geopolitical shocks in the short term, while aluminum extrusion broke away from traditional seasonal fluctuations and remained stable.

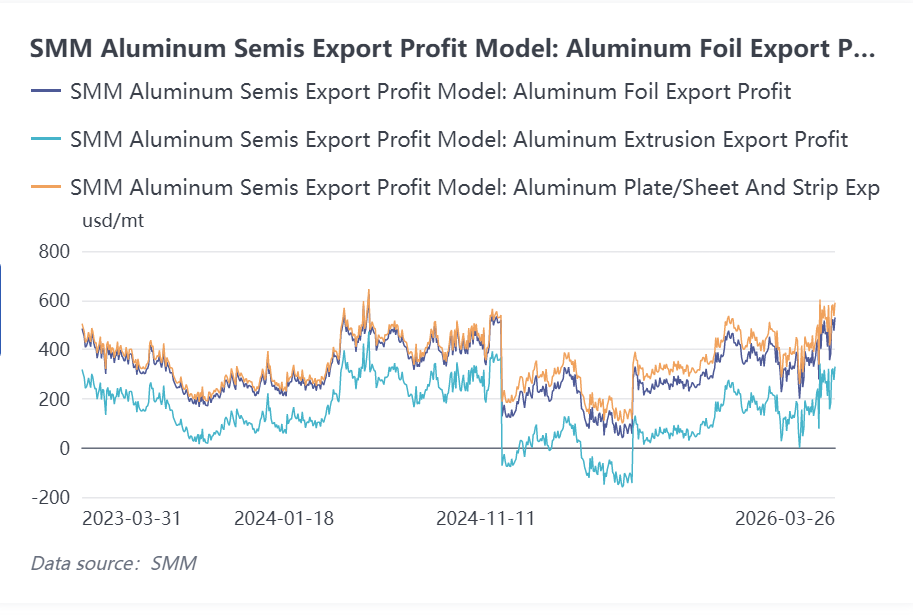

Looking back at (Breaking! China Cancels Export Tax Rebates for Aluminum Semis, Brief Analysis of the Impact on the Outlook [SMM Analysis]_In-Depth Analysis_Aluminum_SMM), on November 15, 2024, the Ministry of Finance issued the Announcement on Adjusting the Export Tax Rebate Policy. Before this announcement took effect, most aluminum semis export products in China were eligible for a 13% export tax rebate. For many years, supported by policy incentives and the product advantages of China’s aluminum semis, China’s aluminum semis had maintained a competitive edge in markets outside China with good quality and low prices. This policy had far-reaching implications for China’s export landscape. SMM believed that the impact of the policy announcement at the time included the following: in the short term, the cancellation of export tax rebates for aluminum semis may, to some extent, increase export costs for export enterprises and dampen the export enthusiasm of China’s aluminum processing enterprises. Over the medium and long-term, as China is a major global exporter of aluminum semis, there is a certain supply-demand gap for aluminum semis outside China. In the absence of corresponding supply increases outside China, the phased decline in China’s aluminum semis exports and the increase in export costs could both push up aluminum prices outside China, widen the price spread between China and outside China, and, without considering exchange rates, lead to a rebound in export profits for China’s aluminum semis, allowing them to regain relevant advantages and thereby repair China’s medium and long-term aluminum semis exports. In addition, growth in aluminum production outside China remained limited, so China’s aluminum semis still had good opportunities in markets outside China, and the tax cost would also be passed on to the buyer market outside China. Of course, the cancellation of export tax rebates for aluminum semis did not involve products such as high value-added aluminum products, and it would also encourage China’s aluminum export enterprises to shift toward exporting high value-added products.

After a year and a half of market validation, SMM’s judgment at the time and for the future regarding the aluminum semis export market was basically accurate. Based on SMM’s monitored aluminum semis export profit data in recent years, from 2022 to November 2024, aluminum semis export profits generally remained in positive territory. Benefiting from the 13 export tax rebate policy, the industry maintained strong earnings stability, especially in the year following the cancellation of the aluminum semis export tax rebate, when export profits generally stayed in the high range of $400-600/mt. After the rebate was canceled in December 2024, profits plunged almost vertically, and during the painful adjustment period most enterprises fell into losses. Throughout 2025, profits gradually fluctuated and recovered, especially since H2, as aluminum prices in the domestic and overseas market fluctuated higher step by step. By Q1 2026, aluminum semis export profits had recovered to the high level seen before the aluminum semis export tax rebate was canceled at the end of 2024.

II. Core Export Performance and Subsequent Expectations for Various Aluminum Semis Segments in January-February 2026

Profitability across product categories showed clear divergence, highly consistent with export performance. As the key export window of Q1, January-February 2026 saw notably differentiated export trends among China’s four core aluminum semis categories—aluminum wire and cable, aluminum plate/sheet and strip, aluminum foil, and aluminum extrusion. These trends were influenced by the base of the same period last year, the policy digestion cycle, and the pace of profit recovery, while also reflecting in advance the potential impact of geopolitical risks on maritime shipping. The specific data, characteristics, and profit linkage analysis are as follows:

(I) Aluminum Wire and Cable: Strong High Growth and Expected to Maintain Positive Growth, with Overseas Power Grid Demand as the Core Driver

Customs data showed that China’s aluminum wire and cable exports totaled 53,280 mt in January-February 2026, up 37% YoY from January-February last year, with total export value reaching $169 million. By export destination, the steady release of China’s aluminum wire and cable exports in January-February 2026 mainly benefited from the concentrated advancement of global new energy projects and power grid infrastructure construction. Among key export destinations, demand support was particularly evident. Tanzania in Africa was the largest export destination for aluminum wire and cable in January-February, with total exports of 7,445.8 mt, accounting for 14.0% of total exports. Its National Energy Transition Plan and Rural Electrification for All Plan entered a concentrated construction phase in early 2026, and surging demand for rural power grid upgrades and supporting lines for new energy projects became the core force boosting exports. In addition, exports to Saudi Arabia in the Middle East reached 6,983.3 mt, accounting for 13.1%, but as the war in the Middle East further escalates, subsequent shipping disruptions may affect future exports to the country. Australia ranked third, with total exports of 5,106.2 mt in January-February, accounting for 9.6%, as the accelerated construction of supporting power transmission lines for local PV and wind power projects further amplified aluminum wire and cable imports.

Overall, China’s aluminum wire and cable exports got off to a solid start in January-February 2026, and the export scale of 53,000 mt laid a good foundation for full-year growth. In markets outside China, continued release of demand for new energy and power grid construction in Africa, the Middle East, and Oceania became the core driver boosting exports. On the China supply side, the industrial clustering effect in leading provinces was significant, providing strong support for stable export volumes. Looking ahead to full-year 2026, aluminum wire and cable exports are expected to maintain positive growth, as increased investment in power infrastructure by overseas countries will provide sustained demand support for China’s aluminum wire and cable exports. However, as geopolitical risks intensify, changes in global shipping routes, raw material price fluctuations, and adjustments in trade policies may bring potential risks. In the short term, more attention should be paid to changes in demand dynamics both outside China and in China.

(II) Aluminum Plate/Sheet and Strip: Base Effect Plus Short-Term Demand Support, but May Face Dual Pressure Later

China’s aluminum plate/sheet and strip exports totaled 509,300 mt in January-February 2026, surging 16.65% YoY. Among them, January exports were 278,500 mt, up 16% YoY, and February exports were 230,800 mt, up 17% YoY. Monthly growth was balanced, and the category remained the largest among aluminum semis exports. By trade mode, exports under processing trade with imported materials were 76,000 mt, accounting for 14.9%; exports under processing trade with supplied materials were 9,600 mt, accounting for 1.9%; and Ordinary Trade remained the core export mode. By country, Mexico was the largest export destination, with 66,300 mt and a 13.0% share, followed by the US with 50,000 mt and a 9.8% share. Vietnam, South Korea, and Indonesia ranked third to fifth, and the top five countries together accounted for nearly 40%. This round of high growth mainly benefited from the low base effect. During the same period in 2025, affected by the implementation of the export tax rebate cancellation policy, overseas clients front-loaded demand, and exports stayed at a low level amid the transition period for negotiations under the new pricing system. At the same time, overseas manufacturing restocking and recovering demand for industrial sheets & plates such as PV jointly supported stronger aluminum plate/sheet and strip exports.

On the other hand, with the escalation of the Iran-Israel conflict and the deterioration of the security situation in the Strait of Hormuz, the regional trade chain has now been effectively disrupted. According to the SMM survey, orders involving the Middle East have now been fully suspended, and even some in-transit cargoes are facing return or port detention because insurers refuse to cover war risks. The complete halt of these orders will directly and sharply impact exports in March and Q2, with an effect far exceeding seasonal fluctuations. Although industrialization in emerging markets such as Southeast Asia is still advancing, the incremental demand there will be difficult to offset in the short term the loss of the Middle East market and the contraction of traditional markets. Aluminum plate/sheet and strip exports in March are expected to face the risk of pulling back under pressure, and the industry will enter a critical period of proactive destocking and market structure adjustment.

(III) Aluminum Foil: Slight YoY Decline, with Geopolitical Conflict Suppressing Export Expectations in Advance

China’s aluminum foil exports totaled 214,800 mt in January-February 2026, down slightly 0.74% YoY, with overall performance relatively weak. Among them, January exports were 121,100 mt, up 2% YoY, while February exports were 93,700 mt, down 4% YoY. The post-holiday off-season combined with expectations of geopolitical risks turned growth negative. By trade mode, exports under processing trade with imported materials were 39,000 mt, accounting for 18.2%, while exports under processing trade with supplied materials were 13,000 mt, accounting for 6.0%. The share of processing trade was slightly higher than that of the aluminum plate/sheet and strip category.

Entering March, the outbreak of the Iran-Israel conflict and the sharp deterioration of the situation in the Strait of Hormuz have become the most direct shock affecting exports in March and beyond. According to the SMM survey, all of China’s aluminum plate/sheet, strip and foil orders involving the Middle East have been suspended, and some in-transit orders have been returned or held up at ports. The core issue lies in insurers’ refusal to cover war risks, making it impossible for traders to fulfill contracts. Given the UAE’s role as a Middle East trade hub, with a 6.8% export share in January-February, orders for aluminum foil shipped to the Middle East or transshipped through the Middle East are expected to directly drag down total exports for March. On the other hand, Southeast Asian markets such as Thailand and Indonesia, supported by rapidly advancing industrialization and consumption upgrading, continue to be the core growth engine for China’s aluminum foil exports. January-February data showed that exports to Thailand and Indonesia together accounted for nearly 20%, and this trend is expected to continue in March and throughout the year, partially offsetting the risk from the loss of the Middle East market. Overall, China’s aluminum foil exports will face a severe test in March. Trade disruption triggered by geopolitical conflict in the Middle East is the most prominent short-term negative variable, and total aluminum foil exports in March are expected to decline 5%-8% YoY.

(IV) Aluminum Extrusion: Seasonal Weakness Eased, with Exports Running Smoothly and Orderly

Aluminum extrusion exports in January-February 2026 broke away from traditional seasonal fluctuations and remained generally stable. January exports were 81,000 mt, up 1.4% MoM and down 5.3% YoY; February exports were 64,000 mt, down 20.4% MoM but surging 62% YoY. There was no sharp decline seen in previous years during the Chinese New Year period, mainly because medium and large enterprises in Fujian, Guangdong, and other regions rushed to fulfill foreign trade orders before the holiday, supporting regional monthly exports.

By province, Guangdong was the core export province, accounting for more than 42% in both January and February, followed by Shandong, Fujian, and Hainan. Small and medium-sized enterprises in Fujian and Shandong relied on traders to export construction materials, and orders performed well. Export destinations were mainly in Southeast Asia and Oceania. The main destinations in January were Vietnam and Malaysia, while in February they shifted to Malaysia, Israel, and the Philippines, showing flexible regional distribution. In terms of trade mode, the shares of processing trade with imported materials and processing trade with supplied materials remained stable at around 15%. Enterprises accelerated overseas expansion, and some adopted a model of “domestic semi-finished products exports + overseas deep processing,” setting up production lines in Morocco and Thailand to hedge against domestic policy and overseas trade risks.

Overall, export conditions for China’s aluminum extrusion enterprises gradually stabilized. Some small and medium-sized enterprises in Shandong and Fujian exported construction materials through traders, and current orders were generally good. A large enterprise in South China reported that its battery and automotive material production lines in Morocco adopted a model of “domestic primary product exports + overseas deep processing,” while overseas extrusion lines were still under planning and construction. Enterprises in Shandong also reported that orders for fencing products exported to European and US markets remained stable, and some enterprises were accelerating construction of production sites in Thailand, initially also operating under a model of domestic semi-finished products exports and reprocessing at overseas plants. Looking ahead, the current geopolitical situation in the Middle East is becoming increasingly tense, and some enterprises reported that logistics and transportation channels were blocked, affecting shipment efficiency to some extent. At present, no substantial increase in export orders has been observed. Only one enterprise in Anhui reported that since March, orders for PV extrusion exported to the Indian market have increased compared with the previous period. On balance, aluminum extrusion exports are expected to maintain a generally stable trend in the later period.

III. Overall Outlook for Aluminum Semis Exports in 2026

Overall, aluminum semis export margins are currently rising steadily and have recovered to the high levels seen before the cancellation of aluminum semis export tax rebates at the end of 2024. The short-term impact brought by the tax rebate cancellation policy has largely been absorbed, which is undoubtedly favorable to aluminum semis export performance throughout 2026. Although anti-dumping and other "double remedy" policies against China’s aluminum semis continue to emerge outside China, the adaptability of relevant enterprises in China has clearly strengthened, and the growth in aluminum semis production outside China remains limited. China’s core position in the global aluminum semis market has not been shaken; only the export structure continues to improve, with the share of high value-added products continuing to rise and low-end product exports gradually contracting. In 2026, China’s aluminum semis exports are still expected to have good opportunities outside China. Although the impact of geopolitical conflicts is severe, both "risks" and "opportunities" coexist. If geopolitical conflicts in the Middle East continue to escalate, disruptions to shipping through the Strait of Hormuz will cause a sustained and severe impact on the maritime transport system along Middle East routes, but supply gaps in the global market may also emerge at any time. The industry can offset risks by optimizing order structures and shifting efforts toward emerging markets such as Africa and Southeast Asia.

![Tight Supply Outside China Continues, China’s Inventory Remains Under Pressure [SMM Analysis]](https://imgqn.smm.cn/usercenter/zlIyw20251217171654.jpg)