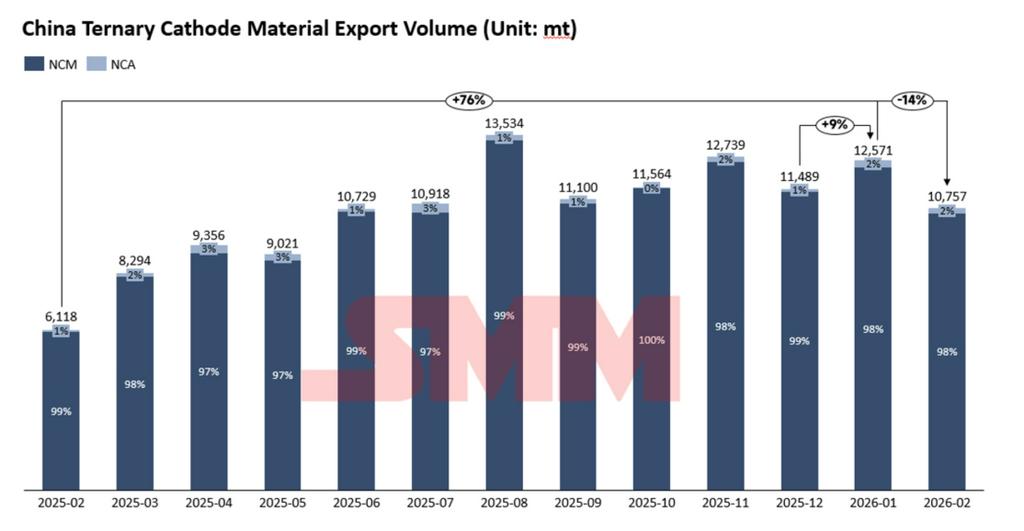

In February 2026, China's ternary cathode material exports (NCM and NCA combined) totaled 10,800 metric tons, representing a 14% MoM decline but a 76% YoY increase. Among these, NCM exports accounted for 10,600 metric tons, comprising 98% of the total.

By destination, South Korea remained the largest importer of NCM, with imports reaching 5,147 metric tons in February. Poland and Japan ranked second and third, with imports of 1,490 metric tons and 1,457 metric tons respectively. Additionally, Germany, Malaysia, and Hungary recorded significant YoY increases in import volumes.

In terms of overall export volumes, exports from January to February 2026 remained at historically high levels, similar to the volumes seen in the second half of 2025. The traditional seasonal pattern for overseas ternary cathode demand is typically weaker in the early part of the year and stronger toward year-end. The ability to maintain high export levels in the first quarter of this year is primarily attributed to the impending cancellation of China's 13% VAT rebate on ternary cathode material exports, effective April 1. In anticipation of this policy change, most overseas customers placed orders in advance, bringing forward some demand. Export volumes in the second quarter are expected to decline notably.

It is worth noting that the overall overseas ternary cathode demand outlook for 2026 remains subdued. The U.S. market has been sluggish since the fourth quarter of last year, prompting many overseas manufacturers to place their hopes on the European market. On one hand, several European countries remain committed to the long-term trend of electrification, with many having resumed or extended new energy vehicle subsidy programs. On the other hand, certain policy adjustments may impact EV sales of some automakers in the near term.

For instance, Norway has begun imposing VAT on certain high-priced EVs, marking the end of the universal subsidy era. The UK and France have implemented strict distinctions among automakers eligible for subsidies, favoring domestically produced brands, which has negatively impacted short-term sales of non-European brands exported to these markets. Additionally, the recently proposed IAA presents significant challenges for non-EU suppliers targeting the European market.

While these policy fluctuations may temporarily affect the European sales of some Chinese, Japanese, and Korean automakers, they also encourage these manufacturers to accelerate the development of their production footprints in Europe, thereby facilitating long-term market positioning.