SMM News, March 27

This week, the tungsten market showed a divergent trend with mild corrections in domestic prices and a contrarian rise in overseas APT prices. Domestic tungsten concentrate and midstream product prices remained relatively firm, while scrap tungsten prices dropped sharply as profit-taking emerged. Supported by a tight supply-demand balance, overseas markets strengthened, further widening the price gap between domestic and international markets.

Tungsten Concentrate

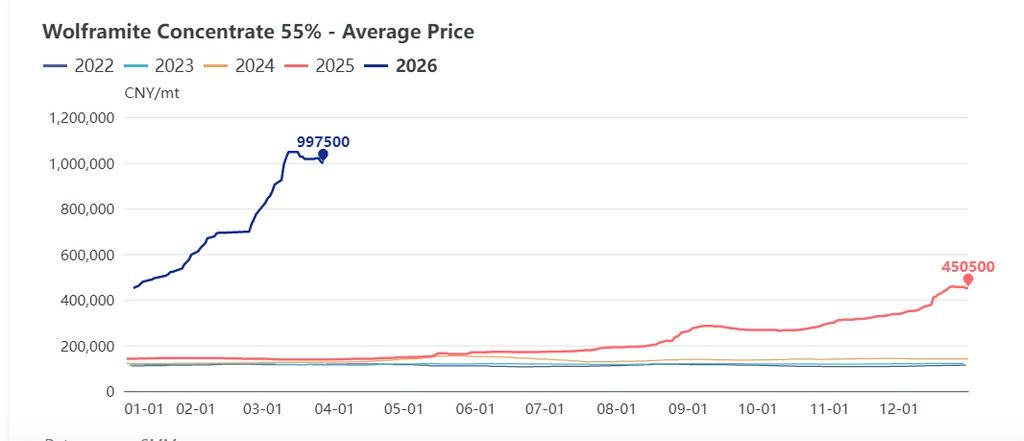

Prices of 65% wolframite concentrate edged down from 1.0205 million yuan per standard ton to 1.0025 million yuan per standard ton during the week. Mines in major producing regions such as Jiangxi and Hunan mostly shipped under long-term contracts. Quotes for high-grade ore remained firm with tight market circulation, while downstream buyers pressed hard on low-grade ore, widening the price gap between high and low-grade ores.

On March 25, an enterprise in Guangdong issued a tungsten long-term order at 1.005 million yuan per ton for 55% wolframite, 15,000 yuan per standard ton lower than other enterprises’ long-term prices on March 20, leading to diverging market sentiment. A mine in Yunnan postponed its auction shipment due to certain reasons, reviving market wait-and-see sentiment. Some spot deals were negotiated below 1 million yuan per standard ton, with thin overall trading volume.

Midstream APT & Powder

The midstream APT market was split. As of today, spot APT negotiation prices fell to 1.46–1.48 million yuan per ton. With long-term contract prices higher than spot prices, smelters mainly fulfilled long-term orders, and most circulating goods came from traders’ low-cost early inventories. Driven by a “buy on rally, sell on decline” mentality, downstream powder enterprises showed weak purchasing enthusiasm.

Powder prices fluctuated slightly, with enterprises mostly shipping against existing orders and few new orders placed. High costs of on-hand orders forced firms to prioritize contract fulfillment. End-users such as cemented carbide and cutting tool companies purchased cautiously with small, rigid orders, resulting in thin spot trading. Some firms cut prices slightly to recover cash flow.

In contrast, Rotterdam APT prices rose 5.66% contrarily to 2,800 USD/tu (approximately 1.71 million yuan in RMB). Including VAT, the domestic-international APT price gap widened to 447,000 yuan per ton, opening an arbitrage window for tungsten exports. Leading domestic smelters became more willing to accept export orders, but dual-use item regulations limited export growth. Strong overseas prices effectively underpin domestic markets.

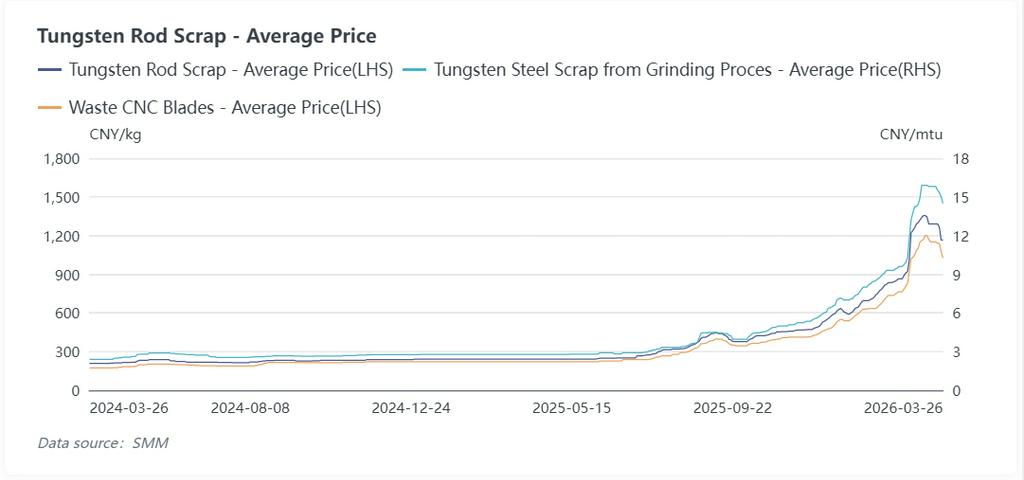

Scrap Tungsten

Scrap tungsten was the main driver of short-term market volatility this week. Scrap tungsten rods, for example, plummeted 11.24% to 1,145 yuan per kilogram. The core reason was concentrated profit-taking by traders who stocked up at low prices earlier, causing a short-term surge in supply and intensified buyer-seller bargaining.

Buyers generally pressed down procurement prices, with larger drops in prices paid by traders to individual suppliers. Some recyclers purchased scrap tungsten rods from individuals at only 950 yuan per kilogram, leading to chaotic industry quotes and unclear short-term trends. Sellers began to hold back stocks, while actual deals were mostly small trial volumes. Individual holders rushed to sell, triggering stampede-style price cuts in some regions and fueling market panic, which in turn dragged down overall tungsten market sentiment and pressured prices. Scrap tungsten smelters remained on the sidelines with low procurement enthusiasm.

Short-term & Long-term Outlook

In the short term, the tungsten market saw a rapid rally in January–February, with strong restocking by domestic end-users pushing up industry raw material inventories. This week, end-users focused on digesting existing stocks with no large-scale restocking.

Notably, some end-users — including cemented carbide tool makers, high-speed steel enterprises, machine tool and cutting processing firms — have issued price increase notices for tungsten-containing products this week, indicating that end-demand-driven logic remains intact. However, the recent correction in upstream prices has dampened downstream restocking appetite. The industry will continue to destock in the near term, with most end-users reporting inventories sufficient until mid-to-late April. The timing and strength of the next downstream restocking cycle will be key to short-term market trends.

Meanwhile, mines in Yunnan, Guangdong and Guangxi plan to hold tungsten concentrate auctions next week, which may improve concentrate supply. APT operating rates have recovered to around 75%, easing tight raw material supply. A short-term supply-demand mismatch, coupled with panic from concentrated profit-taking in the scrap tungsten market, jointly pressured tungsten prices downward this week.

For the long term, regular quota controls and environmental regulations remain in place, capping production expansion. A global tungsten supply-demand gap persists, and the tight supply of primary ore will not fundamentally change. On the demand side, robust growth is seen in high-end sectors — rigid demand from photovoltaics, military industry and semiconductors is gradually rising, offsetting weakness in traditional sectors and forming solid long-term price support.

A continued tight supply-demand balance overseas, together with export benefits from the widening domestic-international price gap, further strengthens the long-term supportive outlook.

Key Focus for Next Week

- Tungsten concentrate mine auctions

- Downstream restocking ahead of the Qingming Festival

- Trading performance in the scrap tungsten market

![Scrap Tungsten Market Saw a Slight Price Collapse, While Ore and Upstream Smelting Products Consolidated Sideways [SMM Tungsten Daily Review]](https://imgqn.smm.cn/usercenter/CIcRv20251217171725.jpg)

![[SMM Analysis] China’s Tungsten Exports Fall in January-February 2026, While Ore Imports Skyrocket](https://imgqn.smm.cn/production/admin/news/cn/thumb/gsyYF20180628085444.jpeg?imageView2/1/w/176/h/110/q/100)

![Strong Wait-and-See Sentiment; the Tungsten Market Awaited Transaction Stabilization [SMM Tungsten Daily Review]](https://imgqn.smm.cn/usercenter/HBsPu20251217171723.jpeg)