News Release, March 23, 2026

According to data from China Customs:

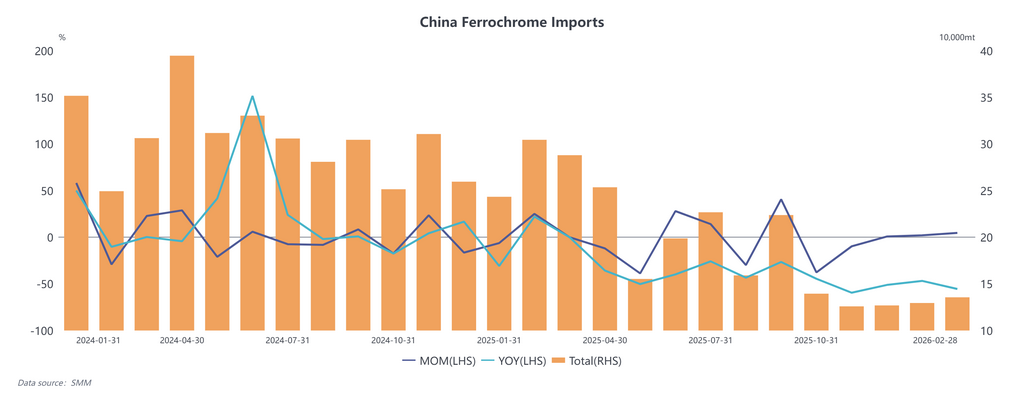

In January 2026, China imported a total of 129,500 metric tons of high-carbon ferrochrome, up 2.1% month-on-month and down 46.8% year-on-year. Of this volume, imports from South Africa stood at 300 metric tons, falling 74.7% month-on-month, while imports from Kazakhstan reached 86,900 metric tons, a decrease of 3.4% month-on-month.

In February 2026, China’s total imports of high-carbon ferrochrome amounted to 135,600 metric tons, rising 4.7% month-on-month and dropping 55.5% year-on-year. Imports from South Africa were 40,400 metric tons, and imports from Kazakhstan were 88,600 metric tons, down 17.7% month-on-month.

Combined for January–February 2026, China imported 265,100 metric tons of high-carbon ferrochrome in total, a year-on-year decline of 51.6%. Breakdown by origin: imports from South Africa were 40,700 metric tons, down 83.3% year-on-year; imports from Kazakhstan were 158,400 metric tons, down 19.7% year-on-year.

Eskom, South Africa’s power utility, has offered a temporary preferential electricity tariff of 87 South African cents per kilowatt-hour to major chrome producers including Glencore and Samancor, helping local ferrochrome smelters resume and scale up production. Eskom also stated that it is pushing ahead with a tariff policy of 62 South African cents per kilowatt-hour to revitalize the domestic ferrochrome sector. Nevertheless, South Africa’s production recovery remains limited. Glencore recently indicated that certain terms in ongoing negotiations are unacceptable, which may lead to intermittent delays in restarting its ferrochrome smelters. Meanwhile, Samancor is pressing ahead with workforce reductions. Overall, South African ferrochrome supply will stay subdued, keeping China’s ferrochrome imports at a relatively low level for the time being.

![[SMM Analysis] Magnesium Exports Surge in Early 2026, Geopolitical Turmoil Threatens Q2 Outlook](https://imgqn.smm.cn/usercenter/LYGyd20251217171725.jpg)

![Scrap Tungsten Market Saw a Slight Price Collapse, While Ore and Upstream Smelting Products Consolidated Sideways [SMM Tungsten Daily Review]](https://imgqn.smm.cn/usercenter/CIcRv20251217171725.jpg)