I. Post-Holiday Inventory Continues to Build Up, with YoY Increase Reaching a Five-Year High

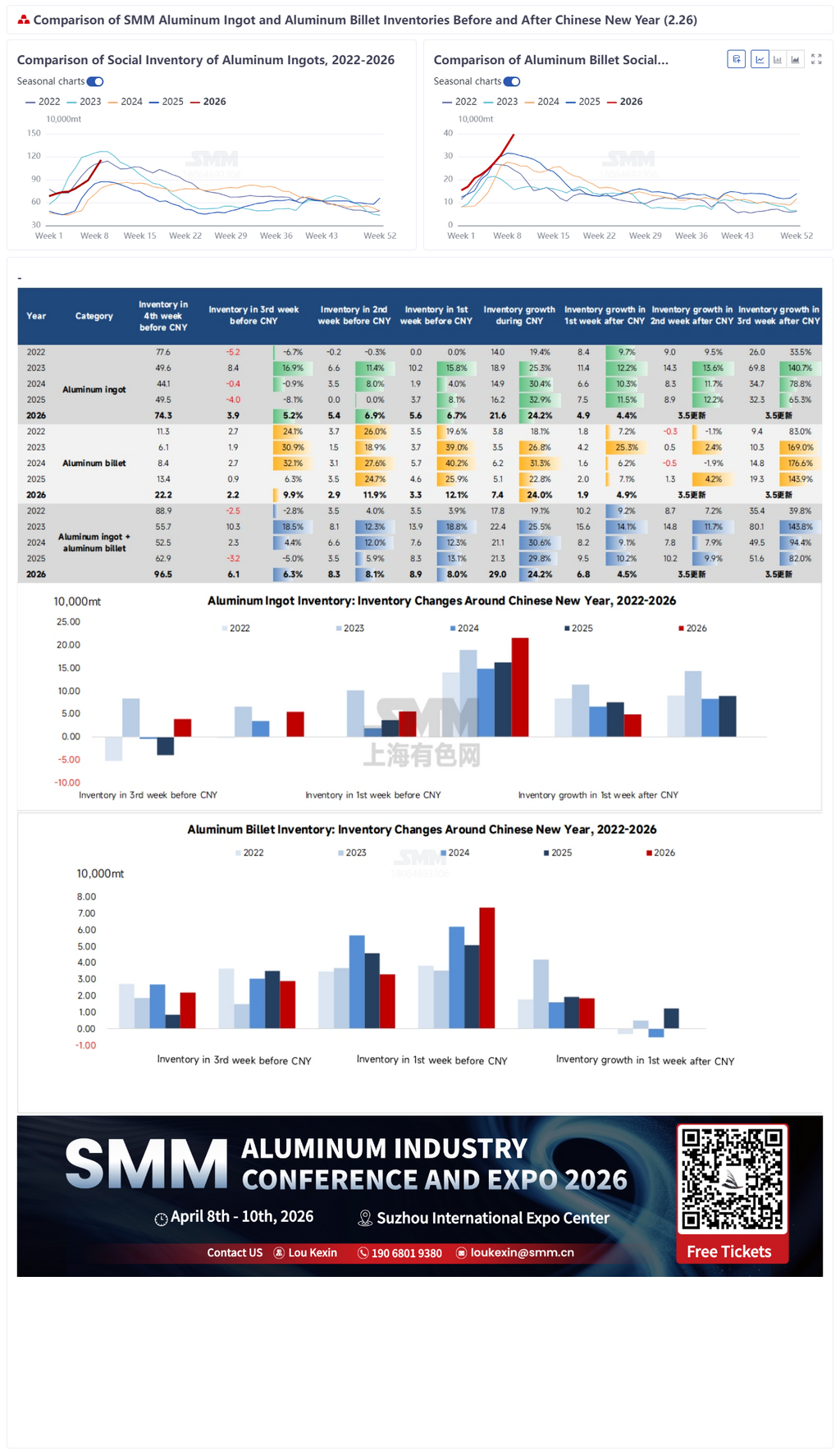

According to SMM, as of Thursday, the inventory of aluminum ingots in major domestic consumption areas stood at 1.157 million mt, an increase of 49,000 mt from the first day of resumption (February 24) and a cumulative increase of 265,000 mt from before the holiday (February 12), clearly indicating a buildup trend. Compared to the same period during the Chinese New Year, the inventory increase in 2026 reached 216,000 mt, setting a new high over the past five years, reflecting the significant supply-demand imbalance during the holiday.

However, it should be noted that due to the relatively high pre-holiday inventory base, the overall inventory increase during the holiday was 24.2%, and the inventory level in the first week after the holiday (1.157 million mt) was slightly lower than the previously expected 1.2 million mt, somewhat alleviating short-term inventory pressure. Nevertheless, the overall inventory level remains high. Considering historical inventory trends, the turning point for destocking appeared earlier after the 2025 Chinese New Year, but this year, due to severe supply pressure and a slower pace of demand recovery, the inventory buildup cycle is expected to extend further.

II. Mainstream Consumption Areas Face Urgent Storage Capacity Shortages, Widespread Backlogs at Rail Stations

Affected by multiple factors such as the concentrated arrival of goods before and after Chinese New Year, delayed logistics, and insufficient manpower, storage capacities in major domestic consumption areas have remained tight, with a significant reduction in warehousing efficiency. This has led to a large accumulation of aluminum ingots at railway stations, becoming the most prominent pain point in the current market.

According to SMM's latest survey, varying degrees of aluminum ingot backlogs at rail stations are observed across major consumption areas: Wuxi has about 80,000 mt, Gongyi around 20,000 mt, and Foshan over 10,000 mt; if aluminum billets are included, the total backlog in Foshan reaches approximately 50,000 mt, with particularly evident pressure.

To alleviate storage capacity pressures, warehouses have actively taken measures, including urging clients to pick up goods, reallocating existing storage, and seeking temporary storage sites. However, constrained by a lack of manpower, the relief effects are limited. Aluminum ingots without temporary storage can only be temporarily piled up at the stations, awaiting gradual warehousing.

Notably, station backlogs incur corresponding demurrage fees, with varying standards across different regions: Foshan generally offers a 7-day exemption period, with charges starting from the 8th day; in Gongyi, due to the occupation of storage space by aluminum coils and containers, the cost pressure from backlogs is more pronounced. It is reported that in Gongyi, charges begin from the day the goods arrive, with the first 6 days charged at 10 yuan per container per day, and from the 7th day, the fee increases to 60 yuan per container per day. Normally, a set of flatbed railway cars (carriages) carries about 55-60 mt, typically loaded with two 20-foot standard containers (each carrying about 28 mt). This means the demurrage fees for a single set of carriages will significantly increase with the duration of stay, further adding to the cost pressure for relevant parties, consistent with the floating pricing principle of domestic railway cargo storage fees.

Currently, some warehouses have increased their storage capacity by activating new storage areas, and the backlogged goods are expected to be gradually warehoused. However, overall, the tight storage situation is unlikely to fundamentally change in the short term, and the overall backlog condition is expected to persist until the end of March.

III. Supply-Side Support Continues, Inventory Peak Expected in Mid-to-Late March

Supply side, the continued high level of aluminum casting production will further drive inventory growth. According to SMM calculations, the MoM increase in domestic aluminum casting production in February was about 170,000 mt, largely in line with market expectations at the beginning of the month, reflecting that aluminum enterprises did not experience significant production halts during the Chinese New Year, with continuous release of aluminum ingot supply.

Entering March, the plans for on-site conversion of liquid aluminum at domestic aluminum smelters show a divergent trend: on one hand, due to the fluctuation of aluminum prices at highs and the relatively high finished product inventories, some enterprises indicate that the proportion of liquid aluminum will see a limited rebound; on the other hand, some enterprises expect their casting volumes to return to normal levels. Comprehensive calculations suggest that the national proportion of liquid aluminum in March is expected to rise by 9.1 percentage points compared to February, and also show a significant increase from January. However, the overall proportion of liquid aluminum remains relatively low. Coupled with the industry capacity approaching policy ceilings and limited increases in direct supply of liquid aluminum, the total casting volume in March is still expected to exceed 1 million mt, continuously supporting inventory growth.

Based on the current inventory trends and supply-side expectations, SMM expects the peak aluminum ingot inventory in Wuxi to be around 550,000 mt, in Foshan about 350,000 mt, and in Gongyi around 300,000 mt; the national peak inventory of aluminum ingots is expected to remain at 1.35-1.4 million mt, likely to appear in mid-to-late March. This peak level is notably higher than the same period in 2025, reflecting the unique post-holiday inventory pressure this year.

IV. Outlook: Inventory Turning Point Depends on the Pace of Downstream Demand Recovery

The core issue with the current stockpiling of aluminum ingots domestically lies in the mismatch between the continuous release from the supply side and the lagging recovery of downstream demand. As post-holiday resumption progresses, the gradual increase in operating rates at downstream enterprises will drive an increase in warehouse withdrawals of aluminum ingots. However, the specific timing for the inventory turning point still needs to be closely monitored based on the intensity of resumption at downstream enterprises, the actual recovery of end-use demand, as well as the pace of in-transit cargoes release and the interrelated changes in aluminum billet inventory.

If the resumption progress at downstream enterprises exceeds expectations and terminal orders continue to materialize, it will effectively alleviate inventory pressure and expedite the arrival of the inventory turning point; conversely, if the demand recovery falls short of expectations, the situation of high inventory levels may persist, thereby exerting downward pressure on aluminum prices. SMM will continue to track inventory, operating, and demand data, providing timely updates on market analysis.

![US-Iran Joint Military Escalation May Pose Multiple Shocks to Global Primary Aluminum Supply Chain [SMM Analysis]](https://imgqn.smm.cn/usercenter/zjiqN20251217171650.jpg)

![US-Iran Joint Military Escalation May Pose Multiple Shocks to Global Primary Aluminum Supply Chain [SMM Analysis]](https://imgqn.smm.cn/usercenter/GEsWk20251217171650.jpg)

![Post-Holiday Guangdong-Shanghai Price Spread Shows Initial Signs of Recovery [SMM Analysis]](https://imgqn.smm.cn/production/admin/votes/imagesqsDLb20240416161800.jpeg)