February 27, 2026

The chrome ore market performed strongly in the first week after the Spring Festival. Although the March stainless steel tender prices announced by Tsingshan and TISCO on the alloy side were flat, falling slightly below previous bullish expectations, the ore sector was driven by both costs and supply, with futures and spot prices rising simultaneously. Traders hold an optimistic outlook on the future market, showing a clear attitude of supporting prices.

I. Price Review

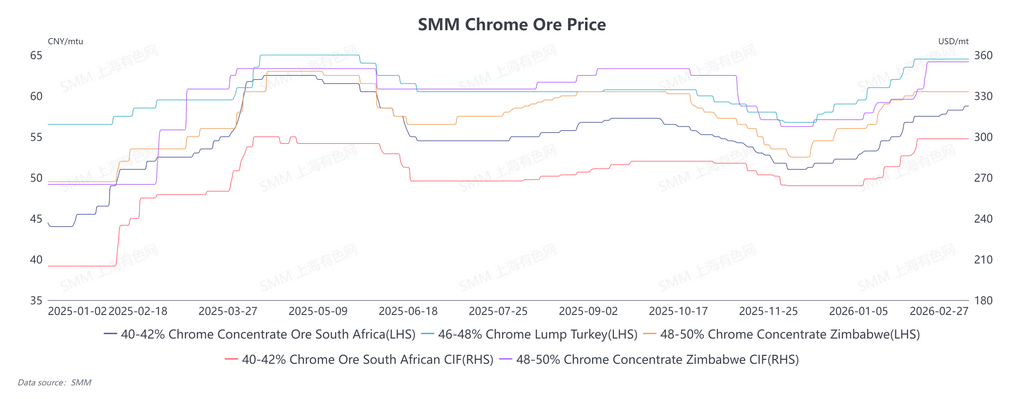

Spot Prices:

- 40-42% South African Chrome Concentrate at Tianjin Port: 58.5-59 yuan/tonne-degree, up 0.5 yuan week-on-week

- 40-42% South African Chrome Concentrate: 52.5-54 yuan/tonne-degree

- 48-50% Zimbabwe Chrome Concentrate: 60.5-61.5 yuan/tonne-degree, up 0.5 yuan week-on-week

- 40-42% Turkey Chrome lumpy Ore: 58-60 yuan/tonne-degree

- 46-48% Turkey Chrome Concentrate: 65.5-66.5 yuan/tonne-degree, up 0.5 yuan week-on-week

CIF Prices:

- 40-42% South Africa Chrome Concentrate: Latest quotation 300 USD/tonne, up 3 USD from pre-festival levels

- 48-50% Zimbabwe Chrome Concentrate: Flat at 350-360 USD/tonne

- 40-42% Turkey Chrome lumpy Ore: Flat at 305-310 USD/tonne

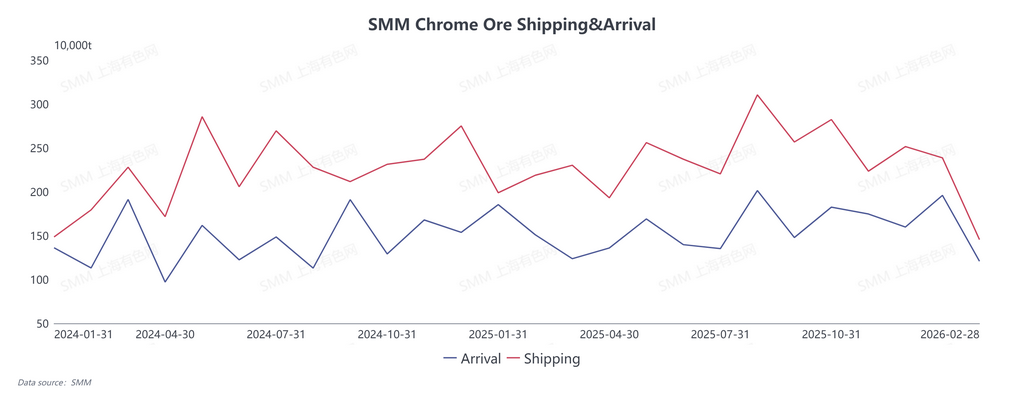

II. Reduced Shipment, Expected Tighter Supply

South Africa and Zimbabwe are in the rainy season, with flooding disrupting chrome ore mining and transportation, slowing shipments.According to SMM statistics, as of February 26, global chromite ore bulk shipment volume reached 2.1332 million tonnes, down 4.31% month-on-month.February’s expected arrivals at Chinese ports are 1.4653 million tonnes, down 8.26% month-on-month.

During the month, major South African chromite producer Glencore announced that 50% of production capacity at its Lion ferrochrome smelter has been successfully restarted.Benefiting from a 12-month temporary electricity tariff of 87.74 South African cents per kWh approved by the National Energy Regulator of South Africa (NERSA), the smelter is expected to resume full production by the end of March 2026.This is expected to boost local chromite ore consumption and may reduce exports; follow-up on South African customs export data is recommended.

On the Zimbabwean side, an immediate ban on the export of run-of-mine ore and lithium concentrate was announced, with strict customs review of export licenses.Coupled with previous port congestion at Beira, arrivals of chromite ore have decreased, intensifying expectations of supply contraction.

In addition, port inventories in China maintain a structural divergence: fine ore is in tight supply, and mainstream lumpy ore is partially out of stock, driving steady price increases.

III. High Demand, Strong Fundamental Support

Domestic ferrochrome producers maintained near-normal production during the Spring Festival.According to SMM data, China’s high-carbon ferrochrome output in February 2026 decreased slightly by 5.33% month-on-month, but rose 50.58% year-on-year.

Currently, downstream manufacturers are mainly consuming pre-festival raw material inventories.However, supported by the upcoming peak consumption season of “Golden March, Silver April” and the concentrated commissioning of new ferrochrome capacity, overall output is expected to remain high and rebound.Demand for Chrome ore procurement is set to be released, further supporting upward price movement.

IV. High Receiving Costs, Strong Price-Supporting Intention

Most Chrome ore arriving at ports currently was sourced at pre-festival high prices of 280-282 USD/tonne, resulting in high receiving costs for domestic traders and strong willingness to support prices.Meanwhile, overseas mine futures quotations continue to rise, with sufficient bullish market sentiment and an upward shift in the overall price center.Low-price Chrome ore is scarce in the market, providing rigid cost-side support for Chrome ore prices.

![Titanium Market Diverged After the Holiday, Titanium Dioxide Leads the Gains While Titanium Products Steadily Recover [SMM Titanium Weekly Review]](https://imgqn.smm.cn/usercenter/wUnEn20251217171722.jpeg)