SMM, February 28 news:

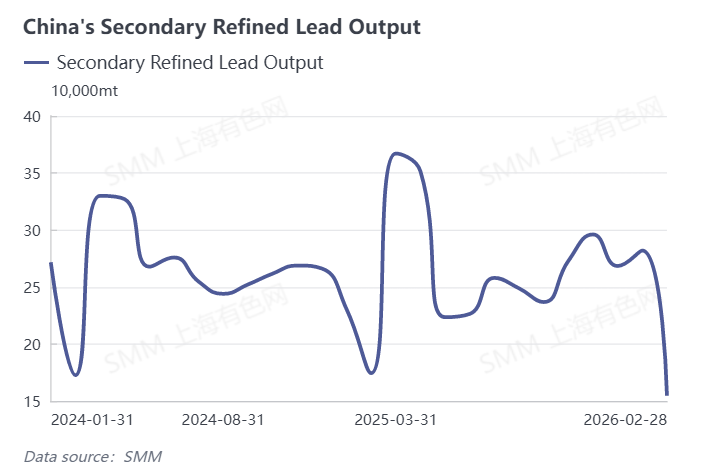

In February 2026, China's secondary lead market was squeezed by three factors—the holiday effect, high costs, and weak demand—leading to a significant pullback in production as expected, with industry operations characterized by "weak supply and demand and profit margins under pressure." Data showed that secondary lead production in February 2026 fell as expected by 140,000 mt, plunging 40.38% MoM and dropping 2.19% YoY; secondary refined lead output decreased 45.18% MoM and declined 11.36% YoY.

In terms of the causes of production cuts, the primary factors were fewer calendar days in the month combined with the impact of the Chinese New Year holiday, which led to widespread shutdowns or production cuts at mainstream secondary lead smelters across the country. Worker departures for the holiday pushed operating rates to low levels, with particularly sharp declines in core production areas such as Jiangsu and Henan due to delayed worker returns and logistics constraints.

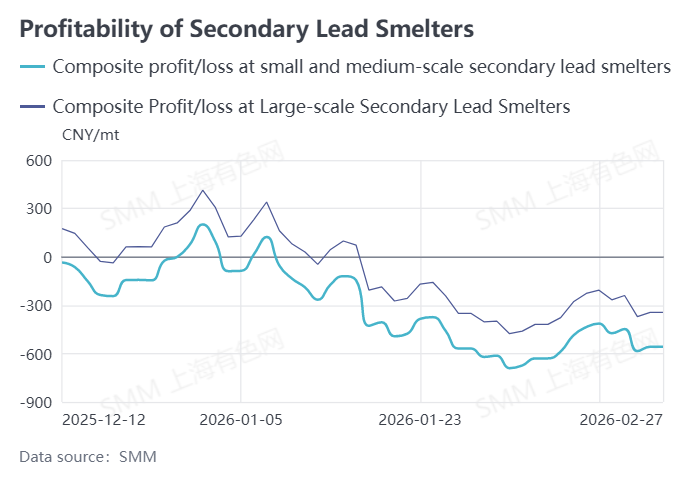

Pressure on the cost side further exacerbated the scale of production cuts: before the holiday, scrap battery prices remained high due to recyclers' reluctance to sell, pushing up secondary lead smelting costs, while lead prices continued to trend weakly during the same period, causing widespread losses among secondary lead enterprises.

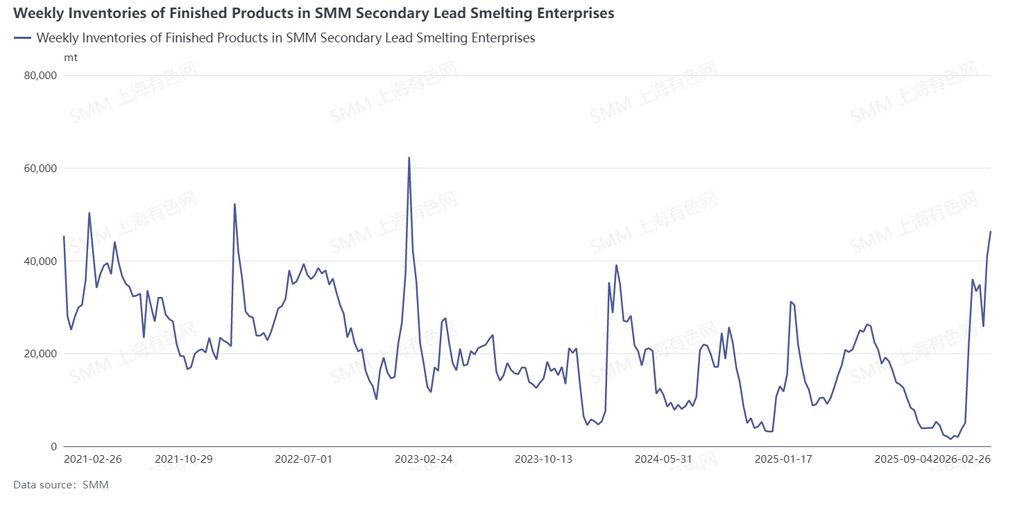

Theoretical comprehensive profit/loss margins for large-scale producers were in negative territory, with small and medium-sized enterprises facing even more severe losses. Weakness on the demand side created a dual suppression: downstream battery producers entered the holiday early, causing lead ingot purchase willingness to hit rock bottom, while smelters' finished product inventories continued to accumulate, further dampening production enthusiasm among enterprises and ultimately leading to a sharp contraction in secondary lead output in February.

Looking ahead to March, China's secondary lead market is expected to see a clear corrective rebound, with production forecast to increase by about 70,000 mt compared to February. The core driver of this trend is the comprehensive resumption of work and production across the industry chain after the holiday. With workers returning in concentration after the Lantern Festival, secondary lead smelters will enter a period of concentrated production resumptions, and some enterprises have indicated that they can resume operating at full capacity by mid-March.

Gradual recovery in downstream demand will provide solid support for the production rebound: battery producers are resuming work successively, pre-holiday accumulated lead ingot inventories are entering a digestion cycle, and purchase willingness is expected to continue improving. Meanwhile, some secondary lead enterprises need to ramp up production to fulfill long-term contract delivery obligations, further driving up operating rates.

On the raw material side, the scrap battery recycling market is gradually recovering after the holiday, and smelters' raw material inventories are expected to be replenished, easing supply constraints. Although enterprises still face certain profit pressures, with the combined effects of demand recovery, order support, and inventory digestion, production enthusiasm in the secondary lead industry is expected to improve significantly. Output in March is likely to achieve a substantive rebound, and industry operations will gradually return to normal.

![Weekly Brief Review of the Lead Concentrate Market (February 23, 2026–February 27, 2026) [SMM Lead Concentrate Weekly Review]](https://imgqn.smm.cn/usercenter/hrxHx20251217171721.jpeg)

![Downstream enterprises primarily focused on digesting pre-holiday inventory after the holiday, with trading activity in the spot market remaining subdued. [SMM Weekly Review of the Refined Lead Spot Market]](https://imgqn.smm.cn/usercenter/lIHfM20251217171721.jpeg)

![SMM Weekly Operating Rate of Primary Lead Smelters (February 20, 2026–February 26, 2026) [SMM Weekly Review of Primary Lead Operating Rates]](https://imgqn.smm.cn/usercenter/msNEk20251217171722.jpg)