As of March 24, anatase titanium dioxide was quoted at 12,600-13,200 yuan/mt, with an average price of 12,900 yuan/mt, flat from the previous day; rutile titanium dioxide was quoted at 13,800-14,500 yuan/mt, with an average price of 14,150 yuan/mt, up 150 yuan from the previous day; chloride-process titanium dioxide was quoted at 14,600-17,200 yuan/mt, with an average price of 15,900 yuan/mt, up 300 yuan from the previous day.

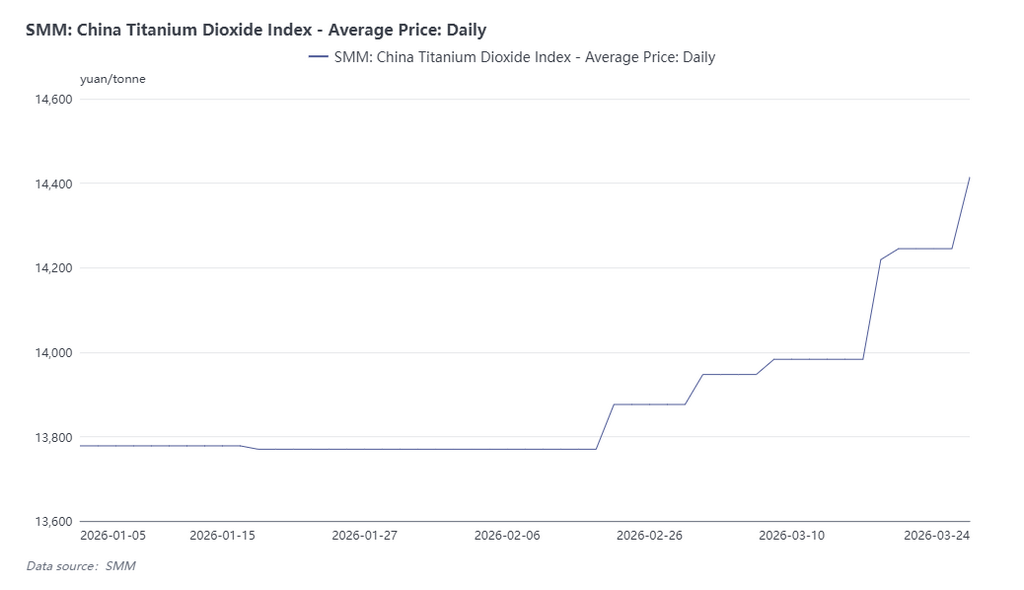

The SMM China titanium dioxide index stood at 14,414 yuan/mt, up 169 yuan/mt from the previous day and up 4.6% from the beginning of 2026.

Since March, titanium dioxide enterprises have issued two consecutive rounds of price hike notices. Starting from March 16, a number of mainstream enterprises successively released their second price adjustment notices within the month, uniformly raising the selling prices of all product grades, including an increase of 500 yuan/mt in the base price for domestic sales and $100/mt in export prices. Subsequently, factory order quotations were generally raised in line with the notices, some enterprises had suspended taking new orders, and market inventory remained low.

Core Logic Behind Titanium Dioxide Price Increases: Resonance Between Cost Pressure and Geopolitical Shocks

The core logic behind the overall price increase was that the titanium dioxide industry saw widespread losses in 2025 due to margin compression from costs. For sulphate-process titanium dioxide, the core cost pressure came from sulphuric acid, with about 2.5-3 mt of sulphuric acid consumed to produce 1 mt of titanium dioxide, implying huge demand. As of March 20, the SMM China smelting acid index stood at 1,079.5 yuan/mt, up 19.49% from the beginning of the year.

The recent escalation of geopolitical conflict in the Middle East severely disrupted the global energy and chemical supply chain. The Middle East accounts for 40% of global sulphur production and 50% of seaborne trade volume, and shipping disruptions in the Strait of Hormuz led to an acute global sulphur supply shortage. China relies on imports for more than 50% of its sulphur supply, of which about 56% comes from the Middle East. Surging sulphur prices have already pushed some sulphur-based sulphuric acid producers into losses, while pyrite ore prices also rose in tandem, further strengthening cost support.

Since March, acid plants in multiple regions have successively shut down for maintenance, and the industry's operating load has declined markedly. Meanwhile, March and April mark the key period for fertilizer preparation for spring plowing, significantly increasing sulphuric acid demand. Overall, sulphuric acid prices after March were still more likely to rise than fall.

For both chloride-process and sulphate-process titanium dioxide enterprises, natural gas was also a key cost item. Producing 1 mt of titanium dioxide requires about 400-500 m³ of natural gas. Geopolitical conflict intensified uncertainty over energy supply, pushing up natural gas prices and further increasing enterprise cost pressure. At the same time, affected by the conflict, international ocean freight rates continued to rise, and export transportation costs also climbed accordingly, creating dual pressure on titanium dioxide foreign trade.

Titanium Dioxide Exports Get Off to a Good Start, Low Inventory Supports March Price Rise

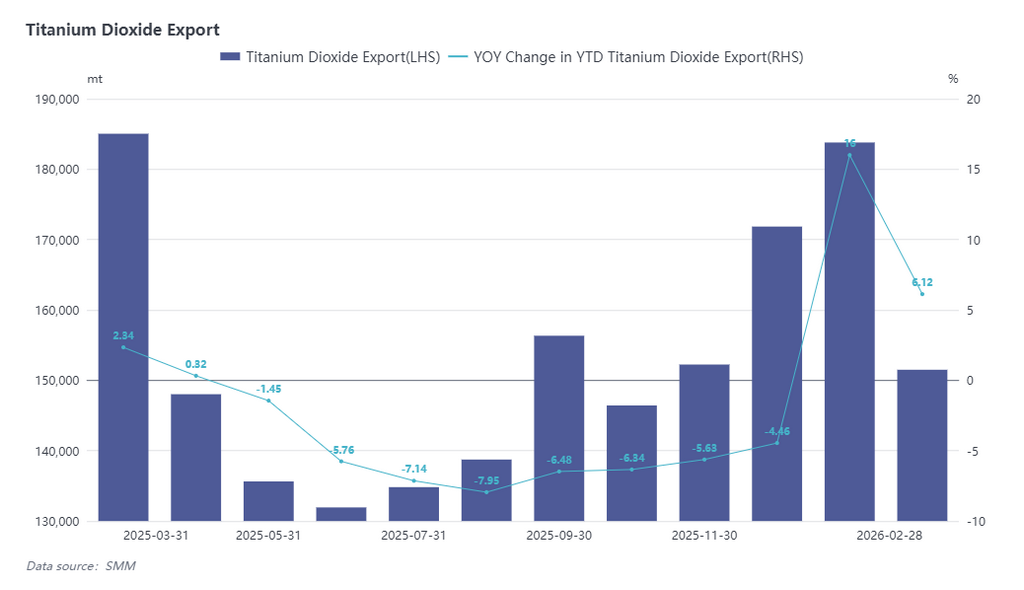

According to the latest customs data, China’s titanium dioxide exports reached 183,800 mt in January 2026, up 12.88% YoY and up 12.88% MoM, hitting a recent high. Exports in February were 151,500 mt, and cumulative exports in January-February were up 6.12% YoY. Overall, titanium dioxide exports got off to a good start in 2026, driving enterprise inventory down 7.2% before Chinese New Year and keeping overall inventory at a low level.

From the production side, since H2 2025, titanium dioxide enterprises had entered a mode of scaling back and cutting output. February production was 310,000 mt, down 5.78% MoM, with the industry's operating rate at only 70%. After work resumed in March, rigid-demand restocking in the domestic trade market started, coupled with concentrated shipments of earlier backlog orders in foreign trade, and overall market inventory remained at a relatively low level. Supported by continued firmness on the cost side, titanium dioxide prices in March maintained an upward trend.

Looking ahead, producers currently have a strong willingness to raise prices, but after the traditional peak demand season in March, whether prices can continue to rise remains uncertain. Geopolitical factors continue to disrupt shipping capacity and oil prices on the Middle East and Europe routes, putting export costs under pressure. In terms of supply and demand fundamentals, the titanium dioxide market still shows an oversupply pattern, with no clear improvement in actual demand and even signs of slight weakness. Overcapacity on the supply side will still require time to be absorbed and phased out. On the cost side, sulphuric acid prices are expected to continue supporting titanium dioxide prices, but the subsequent price trend will still depend on the downstream market's actual acceptance of the price increase letters.