Market Overview

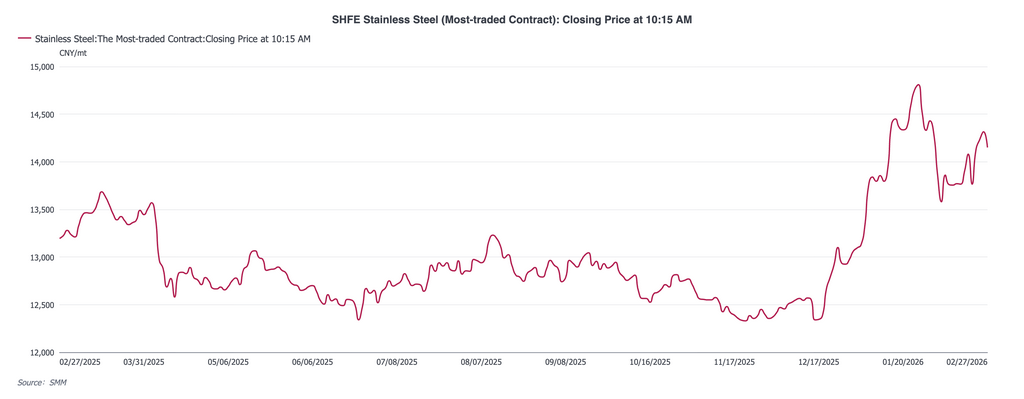

According to SMM data, during the first trading week following the Lunar New Year holiday (February 24 – February 27, 2026), the dominant stainless steel contract (SS2604) opened high and maintained a strong trend, driven by significantly rising raw material costs.

By the close on February 27, the contract price had climbed to 14,150 CNY/mt ($2,065.69/mt), an increase of 385 CNY/mt ($56.20/mt) or +2.80% compared to the pre-holiday closing price of 13,765 CNY/mt ($2,009.49/mt).

In the early post-holiday period, the market's upward logic was primarily dominated by rising costs on the supply side. However, as the price center shifted upward rapidly, the substantial accumulation of social inventory during the holiday formed a tangible suppression on the upside potential. Consequently, futures prices maintained a fluctuating struggle within the 14,100–14,200 CNY ($2,058.39–$2,072.99) range.

Macroeconomic Analysis

From a macro perspective, the market is navigating an interplay between reasonably ample domestic liquidity and uncertainties regarding overseas trade policies.

- Domestic: On February 25, the central bank conducted a 600 billion CNY ($87.59 billion) one-year Medium-term Lending Facility (MLF) operation. This continued to maintain ample liquidity in the banking system, providing macro support for the traditional "Golden March and Silver April" peak consumption season and stabilizing market expectations.

- Overseas: The U.S. Trade Representative stated they would continue to advance the Section 301 investigation regarding the Phase One trade agreement, with proposals to raise "global import tariff" rates from 10% to 15% or higher. Potential tariff changes have intensified uncertainty in the external macro environment, which may have a negative impact on future export expectations for stainless steel and related end-products.

Fundamentals: Inventory & Demand

Fundamentally, the post-holiday market faces the reality of a massive inventory buildup while end-user demand is still in a recovery phase.

- Inventory: Latest SMM data shows that, due to the long Spring Festival holiday, social inventory significantly increased to 1.0161 million tons this week. This is an increase of 121,600 tons compared to the pre-holiday level of 894,500 tons, breaching the one-million-ton mark.

- Spot Transactions: The market is currently in a gradual restart phase. Downstream processing factories have not yet fully resumed work, and current spot circulation is mostly concentrated on resource allocation between traders. The end-market's actual ability to digest current high-priced resources remains to be verified after enterprises fully resume work next week.

- Sentiment: In the short term, high inventory levels pose significant pressure on prices. However, supported by expectations for the "Golden March and Silver April" peak season, holders' sentiment remains temporarily stable, with no large-scale sell-offs observed.

Cost Analysis

The significant strengthening of the cost side was the core driver for the high market opening this week. Driven by news of tighter Indonesian nickel ore quotas and fluctuating rises in nickel prices post-holiday, there is a strong willingness to support prices on the raw material side.

- High-grade Nickel Pig Iron (NPI): As of February 27, quotes were raised significantly, rising by 33.5 CNY ($4.89) in a single week to 1,085 CNY/nickel point ($158.39/nickel point).

- High Carbon Ferrochrome: Prices remained temporarily stable at 8,550 CNY/50 basis tons ($1,248.18/50 basis tons).

The expectation of tight ore supply materialized quickly after the holiday, substantially raising the immediate production costs for steel mills. The upward shift in the cost center effectively limited the room for market correction and forced a passive, steady rise in the center of spot transaction prices.

Outlook & Strategy

Overall, the stainless steel market in the first week after the holiday presented a tug-of-war pattern: "Strong Expectations & High Costs" vs. "Weak Reality & High Inventory."

While the sharp rise in NPI prices established a tone for a strong fluctuating market, the social inventory exceeding one million tons—coupled with end-user demand that has yet to kick in—constrained further upside potential.

Looking ahead to next week, the market trading logic will gradually shift from "sentiment-driven" to "fundamental verification."

- Short-term: Futures prices are expected to maintain a strong fluctuation at high levels.

- Medium-to-long-term: The trend will depend on the actual realization of demand during the "Golden March and Silver April" peak season after downstream sectors fully resume work.

Industrial clients are advised to closely monitor the inventory inflection point (destocking) and actual spot transaction conditions next week. Carefully assess the risks of chasing highs and reasonably utilize hedging tools to manage exposure.

![[SMM Analysis] Nickel Prices Fluctuate Amid Indonesian Supply Disruptions and Market Sentiment Volatility](https://imgqn.smm.cn/usercenter/fzwTi20251217171733.jpg)

![[ SMM Analysis ] Nickel intermediate product market mostly adopts a wait-and-see attitude after the holiday, but affected by accident disturbances, the center of MHP nickel payables shifts upward.](https://imgqn.smm.cn/usercenter/CjEnN20251217171733.jpg)