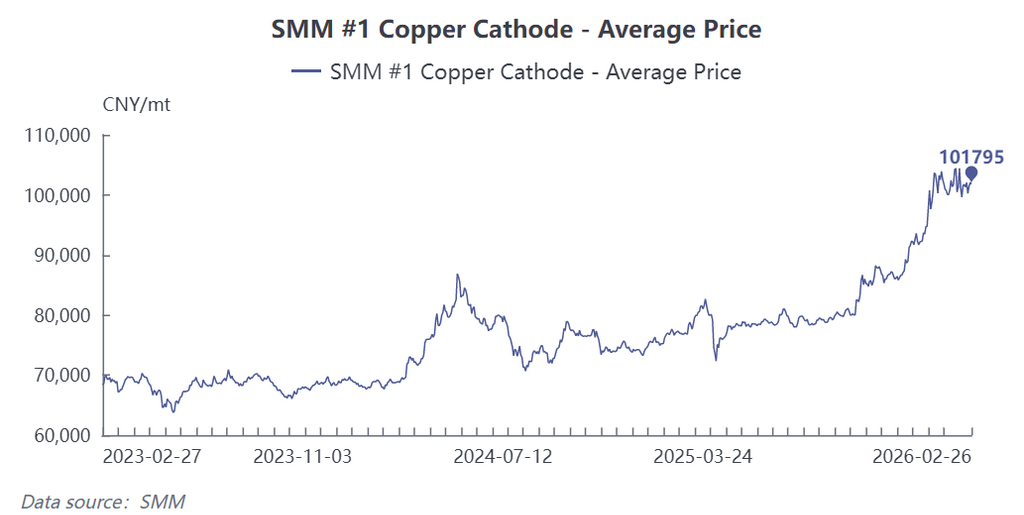

With the official end of the 2026 Chinese New Year holiday, various domestic industries have gradually entered the stage of resuming work and production. However, since the beginning of the year, copper cathode prices have continued to fluctuate at highs, putting significant pressure on downstream processing enterprises. As of February 26, the SMM #1 copper cathode average spot price was reported at 101,750 yuan/mt, with persistently high copper prices significantly impacting brass bar producers through cost transmission and squeezing.

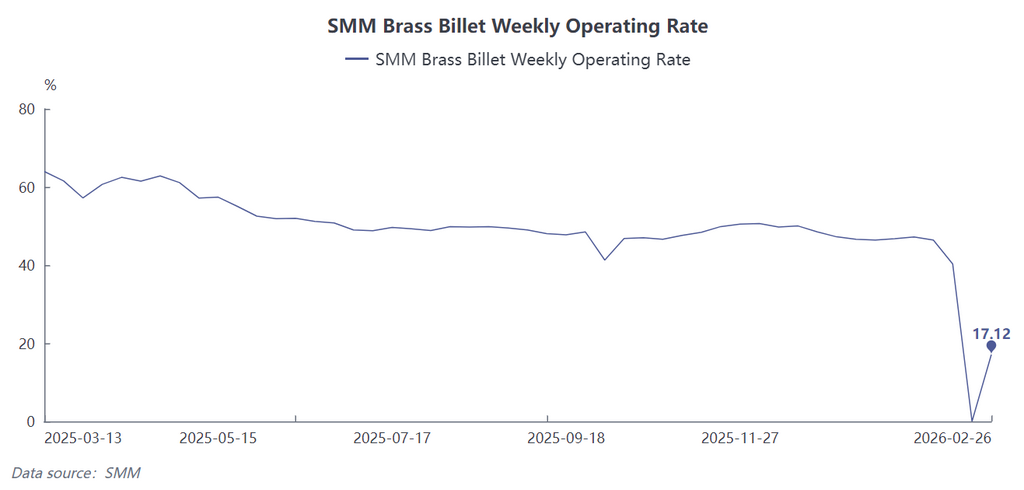

According to SMM, although brass bar enterprises have resumed work, the overall pace is noticeably slower than in previous years. For the week ending January 26 (2.2-2.26), the weekly operating rate for the domestic brass bar industry was only 17.12%, still at a low level. SMM expects the operating rate to slightly recover to 41.18% next week (2.27-3.5), but it will not yet return to pre-holiday normal production levels.

By enterprise type, currently, only some large and medium-sized brass bar enterprises have started production, while many small and medium-sized enterprises remain either fully or partially shut down, with full resumption expected only after the Lantern Festival, reflecting a cautious attitude toward the current market environment.

In terms of raw material procurement, influenced by the continuous high copper prices, the willingness of brass bar enterprises to stockpile is generally low. Most enterprises stated that they are mainly consuming pre-holiday inventories, with very limited new purchases. High raw material costs coupled with weak end-use demand further suppresses production enthusiasm.

From the perspective of end-use demand, the resumption of work and production by downstream enterprises is also slow, with new orders being relatively few. Neither traditional sectors such as construction, hardware, and sanitary ware, nor industries like machinery manufacturing and electrical equipment, show any significant signs of restocking or rushing to meet deadlines. The market as a whole exhibits a characteristic of "high prices, low transactions."

Customs data shows that the total imports of brass bar in 2025 were 26,500 mt in physical content, a YoY decline of 7.35%, indicating a general slowdown in market demand over the past year. Entering 2026, enterprises generally hold a cautious outlook for the year, with some admitting that the situation is "not optimistic."

Overall, the current brass bar market is in a phase of "high costs, low demand, and weak expectations." In the short term, as small and medium-sized enterprises gradually resume work after the Lantern Festival, the operating rate is expected to slowly rebound. However, until copper prices pull back significantly and end-use demand recovers substantially, the industry's overall recovery will still face considerable pressure. Future market trends will require close monitoring of copper price movements and the pace of downstream demand recovery.

![Downstream procurement volume continues to increase, inventory growth slows down, stimulating spot premiums to continuously rise [SMM South China Spot Copper]](https://imgqn.smm.cn/usercenter/TlzAr20251217171709.jpg)