After the Chinese New Year holiday, the first fundamental indicator to watch post-holiday is undoubtedly inventory! SMM compiles the latest inventory data from three markets (LME, COMEX, SHFE) and the evolving logic for the future outlook.

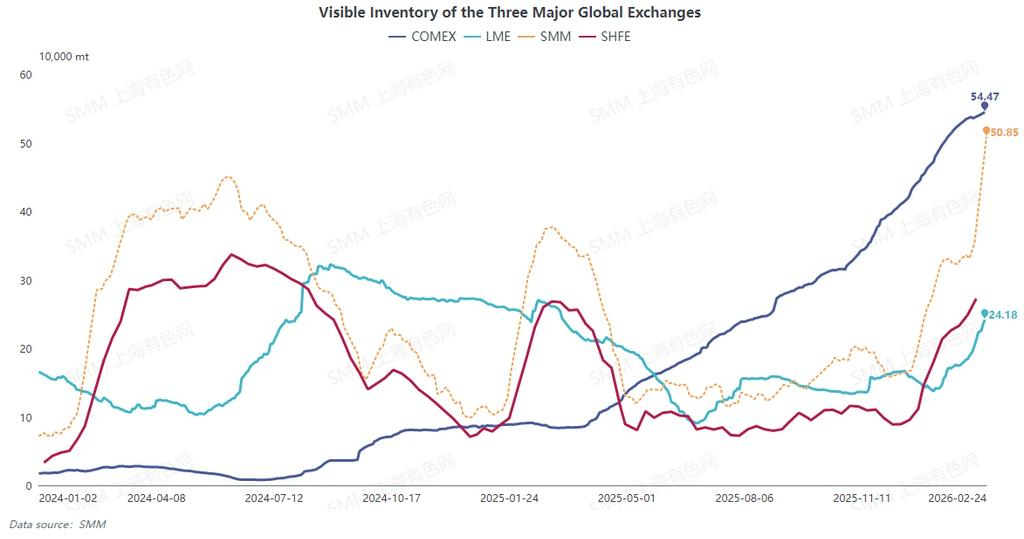

SMM compares inventories across the three major exchanges (since SHFE inventory data is only updated through February 13, SMM inventory serves as the representative for domestic copper cathode visible inventory). During the holiday period, inventories in all three markets continued to increase.

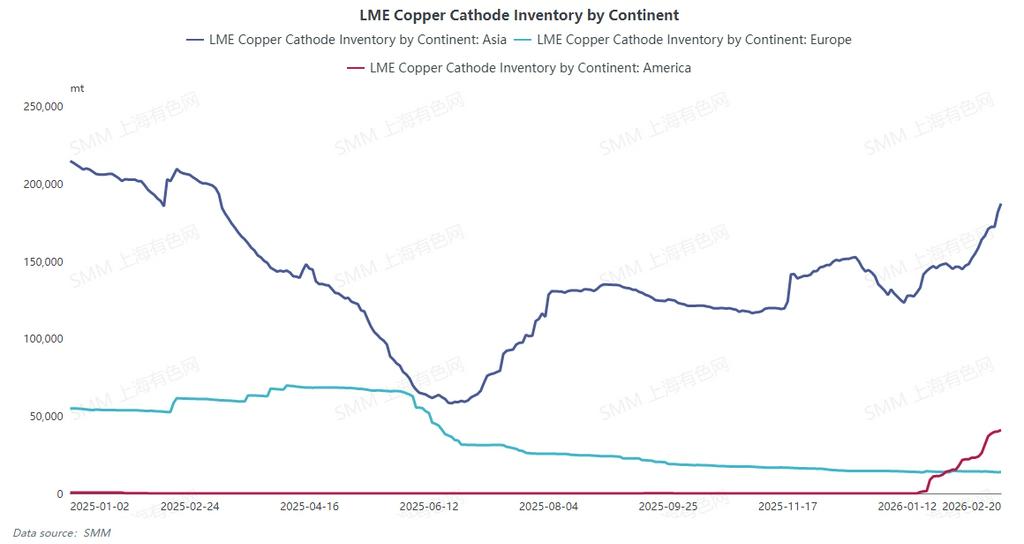

The rise in LME inventory was mainly driven by previously exported Chinese supplies, leading to increases primarily in Asian warehouses. Additionally, it is worth noting that due to a significant narrowing of the COMEX-LME price spread, some shipments originally bound for the US were diverted to LME warehouses in the Americas, causing a noticeable uptick in LME Americas warehouse levels after a prolonged period of calm.

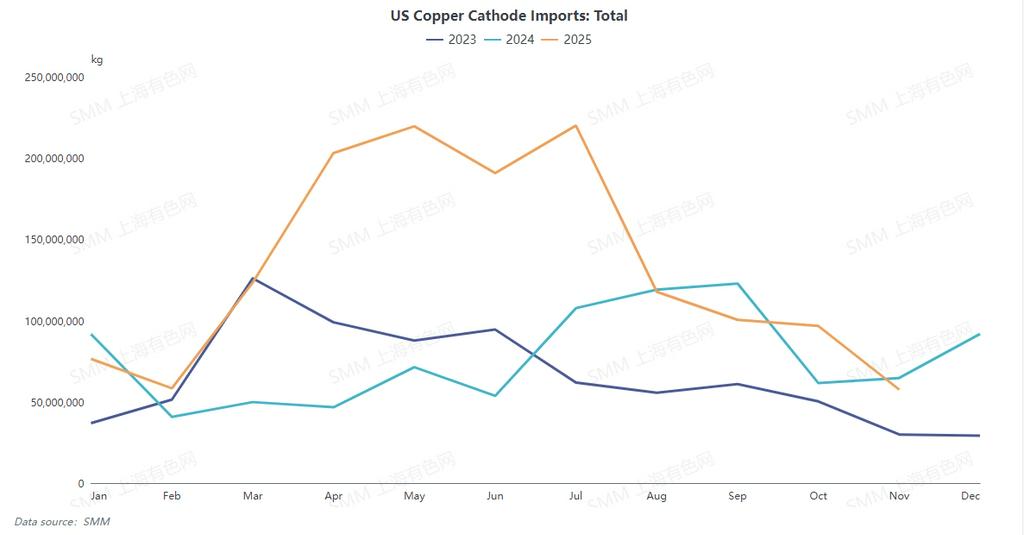

COMEX inventory continued to increase despite the narrowing—or even turning negative—C-L price spread. COMEX inventory has now risen for more than 540,000 mt, though the pace of growth has slowed compared to earlier periods, and US imports have shown a declining trend. According to SMM, March import offers from China have included supplies from Peru, Chile, Australia, among others. Previously, such supplies had entered the Chinese market in minimal quantities for several months, guided by the high C-L price spread.

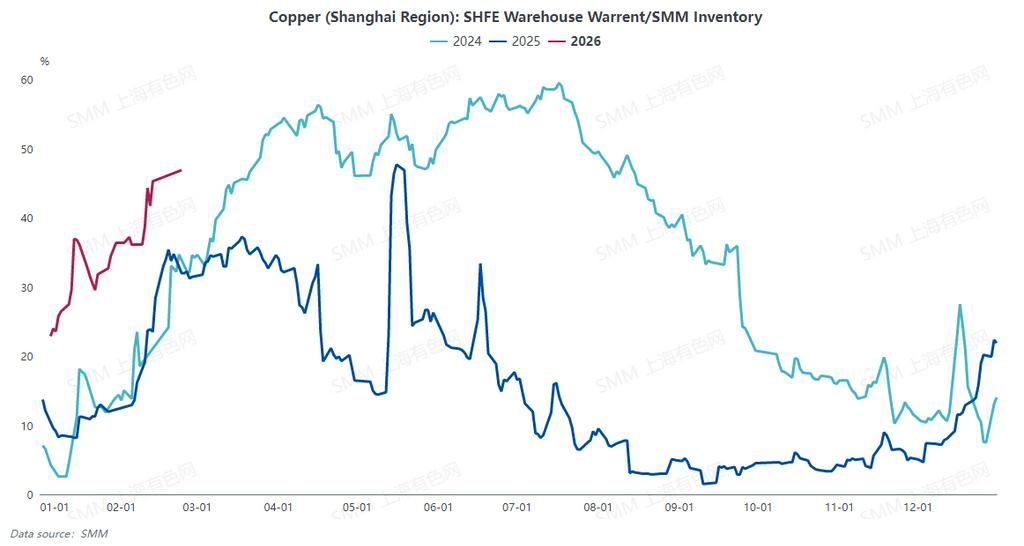

Based on SMM data, social inventory in mainstream domestic regions increased by over 150,000 mt during the holiday period, reaching 508,500 mt. SHFE data showed that copper futures warrants rose by 80,409 mt from pre-holiday levels to 277,089 mt as of February 24, indicating that most supplies were locked in the form of futures warrants.

With inventory increasing beyond expectations, how has the fundamental trading logic shifted?

The biggest uncertainty in the market remains whether Trump will impose tariffs on copper mid-year, but the market has long been prepared for either outcome. As long as copper prices do not surge sharply (referring to being driven to 110,000 by capital flows) and the C-L spread does not remain negative for an extended period, the market still prefers shipping copper to the US. According to SMM's market communication, most US dollar-denominated copper long-term contracts for 2026 are signed on a semi-annual basis, mainly due to pricing challenges for H2 shipments to the US. However, currently, high long-term contract premiums are difficult to accept. Most supplies from Japan, South Korea, Australia, etc., are still being accepted by Chinese buyers at semi-annual long-term contract premiums of 80-100 USD. Previously, the market bet on continuous interest rate cuts by the US Fed. Under the logic of optimistic supply continuously flowing into the US, driven by power, AI, and other demands in China, Southeast Asia, India, etc., copper prices steadily increased; domestic inventory was destocked as it was absorbed by the Southeast Asian region, potentially realizing "squeeze" expectations during the peak season of "Golden March, Silver April."

However, at present, the logic of accelerated copper flow to the US has changed. SHFE and LME inventories have increased more than expected, with visible inventory suppressing fundamentals, bringing copper prices back to a rational range. In the domestic market, since the first trading day after Chinese New Year was the last trading day for the SHFE 2602 contract, most smelters had already sent deliverable supplies to the delivery warehouses before the holiday, leading to an unexpected increase in futures warrants. Post-holiday, social inventory also showed a much higher inventory buildup compared to previous years.

Currently, the import loss of SHFE 2603 contract against LME is gradually narrowing, even showing import profits before the holiday. Imports are expected to increase in March, putting dual pressure from imports and domestic production on domestic inventory, with little chance of outflow in the short term. The continued increase in LME inventory adds further pressure to the entire Asian market, and the LME Contango structure is unlikely to change in the short term.

Therefore, the earlier market expectation that SHFE and LME would start destocking in March will be delayed. According to SMM communications, domestic smelters' concentrated maintenance in H1 is scheduled for March-May, with the impact likely to become apparent starting in April. If consumption holds up, the domestic market may begin significant destocking in late March or April. However, due to the high inventory base, it is unlikely that a high BACK and high premium will occur in May-June. The LME market structure may see an expansion of TOM-NEXT BACK near the DATE, but CASH-3M is not expected to show such a trend.

Trading in H2 still carries significant uncertainty, with macro and fundamental factors relatively unclear, requiring more information to validate the logic.