March 19, 2026:

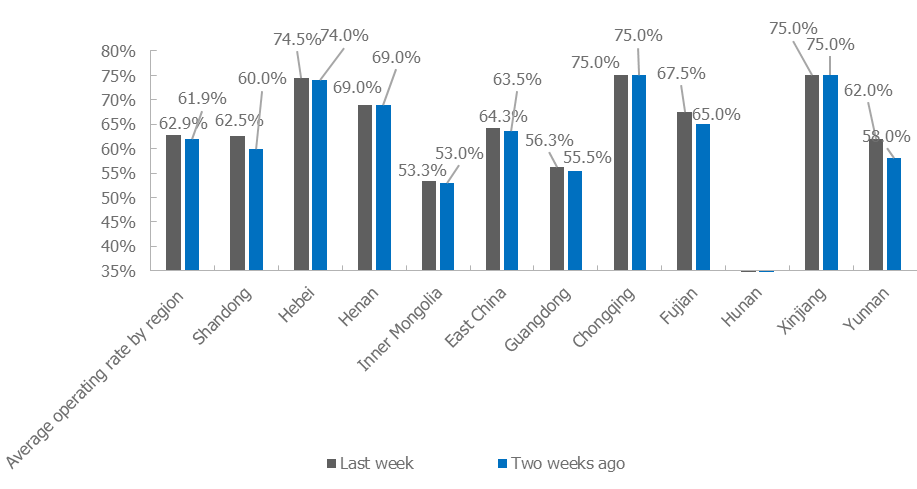

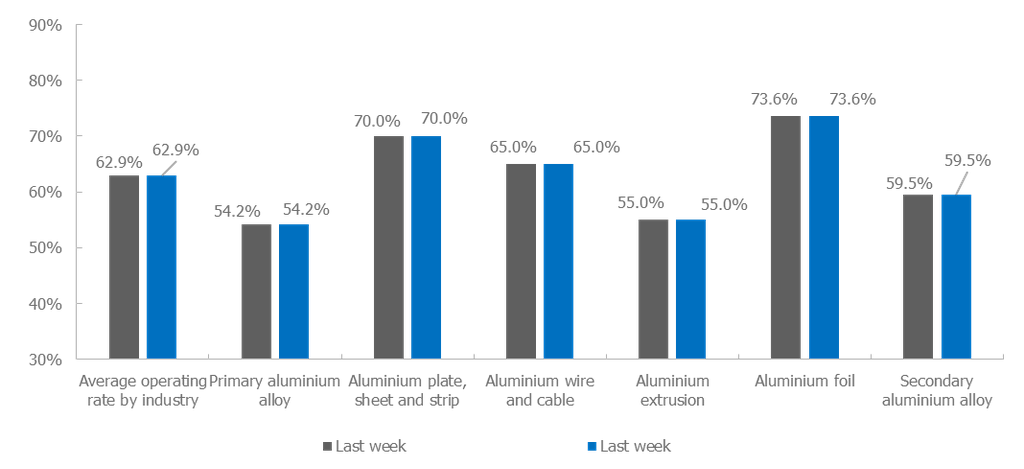

This week, the weekly operating rate of leading downstream aluminum processing enterprises in China edged up 1 percentage point WoW to 62.9%, with signs of the peak season slightly emerging and demand gradually being released. Specifically, the operating rates of leading enterprises in aluminum plate/sheet and strip and aluminum wire and cable were flat WoW this week. Auto orders recovered YoY less than expected and exports to the Middle East were suspended, constraining any further rise in the operating rate. Meanwhile, current demand for wire and cable was at peak-season levels, and expectations for April production schedules improved. However, previously elevated aluminum prices triggered downstream fear of high prices, making procurement strategies more cautious. The industry is expected to remain prosperous through Q2, with operating rates continuing to hold up well. In the primary aluminum alloy sector, the recovery in aluminum demand fundamentals drove a continued rebound in the operating rate, up 1.2 percentage points WoW to 54.2%. However, overall transactions in the spot order market showed mediocre performance, limiting enterprises' willingness to further raise operating rates. For extrusion, PV materials entered the final stage of the rush to export, while new orders in the automotive and power sectors increased significantly, keeping the operating rates of related enterprises at high levels. The operating rate of leading aluminum foil enterprises rose 0.7 percentage points WoW to 73.6%, as demand for multiple aluminum foil products continued to recover, with battery foil and packaging foil orders providing notable support, and operations are expected to remain stable. Seasonal recovery in downstream consumption of secondary aluminum lifted enterprise operating rates, but the overall increase remained mild, rebounding 0.8 percentage points WoW to 59.5%, and a slow recovery is expected to continue in the short term.

Primary aluminum alloy: This week, the operating rate in the primary aluminum alloy industry continued to recover, rising 1.2 percentage points WoW to 54.2%. The main driver behind the increase was the recovery in aluminum demand fundamentals. On one hand, raw material stockpiling by downstream processing enterprises had basically returned to pre-holiday levels, and production pace gradually normalized. On the other hand, demand in end-use consumption sectors was released successively, driving overall orders growth for primary aluminum alloy, especially with a notable increase in long-term contract pickup volume, which provided steady support for the operating rate. However, the increase in the operating rate remained relatively limited, mainly constrained by spot market trading sentiment. Aluminum prices were still at high levels, suppressing purchase willingness among some market entities. Apart from necessary long-term contract deliveries, overall transactions in the spot cargo market showed mediocre performance, limiting enterprises' enthusiasm for further raising operating rates. Looking ahead to next week, as downstream demand continues to recover, the operating rate of the primary aluminum alloy industry is expected to maintain a steady upward trend. Aluminum Plate/Sheet and Strip: This week, the operating rate of leading aluminum plate/sheet and strip enterprises held steady MoM at 70.0%. At the operating level, the aluminum plate/sheet and strip market remained stable during the week, with leading enterprises maintaining steady production. On the order side, domestic end-user demand for can stock packaging was stable, but auto sheets & plates orders fell 5-10% YoY due to a YoY decline in NEV production and sales and the phaseout of purchase tax incentives. In the short term, end-user NEV orders recovered less than expected and failed to effectively drive operating rates higher. End-user energy storage maintained a relatively high operating rate, and some enterprises accelerated production scheduling to ensure deliveries, providing additional support for aluminum plate/sheet and strip materials related to energy storage, such as battery casings and brazing materials. In the short term, the aluminum plate/sheet and strip market is expected to remain stable. Constrained by multiple factors, including aluminum price fluctuations, weaker-than-expected YoY recovery in auto orders, and the suspension of exports to the Middle East, operating rates are unlikely to climb further.

Aluminum Wire and Cable: This week, the weekly operating rate of China’s aluminum wire and cable industry held steady at 65%, flat MoM, and the trend of fluctuating at highs continued. Wire and cable enterprises reported that current demand was at peak-season levels, and expectations for April order scheduling improved. However, previously high aluminum prices triggered downstream fear of high prices, making procurement strategies more cautious, with purchases mainly based on rigid demand and limited willingness to stockpile proactively. On the order side, as of mid-March, the first batch of material tenders for power transmission, transformation, and UHV had been completed in January-February, while the second batch planned for early this year had not yet been announced. In addition to downstream backlog orders on hand, changes in the pace of power grid tenders during the year warrant close attention. Supported by expectations for the continued fulfillment of cargo pick-up for power grid orders, the prosperity of the aluminum wire and cable industry is expected to extend into Q2, with operating rates likely to hold up well.

Aluminum Extrusion: This week, the operating rate of China’s aluminum extrusion industry was 55%, up 3.2 percentage points MoM and down 5 percentage points YoY. Although the traditional peak season of “Golden March and Silver April” arrived and downstream demand gradually recovered, recent wild fluctuations in aluminum prices intensified wait-and-see sentiment among terminal clients, and overall peak-season performance was weaker than in the same period in previous years. By segment, construction extrusion remained subdued overall, but some extrusion plants in Shandong reported that orders for doors and windows made from circulation-grade materials sold to rural markets and Southeast Asia performed well recently, providing some support for the operating rates of related enterprises. For industrial extrusion, the rush to export in PV materials entered its final stage. Although actual production schedules at some module plants were slightly below expectations at the beginning of the month, leading to some reduction in production scheduling at certain small and medium-sized frame enterprises, leading enterprises in Anhui and Hebei still maintained full-capacity operations. Meanwhile, some enterprises in Anhui, Shandong, and other regions reported a notable increase in new orders from the automotive and electric power sectors recently, supporting high operating rates at related enterprises. Looking ahead, as some demand for PV extrusion was released in advance, subsequent operating rates are expected to pull back somewhat. However, supported by the gradual recovery in demand from other downstream sectors, the overall operating rate of the extrusion industry is expected to maintain a stable and improving trend. Aluminum Foil: This week, the operating rate of leading aluminum foil enterprises rose 0.7 percentage points MoM to 73.6%. At the operational level, with March already past the midpoint of the traditional peak season, demand for multiple aluminum foil products continued to recover. High operating rates in the energy storage industry boosted battery foil demand, and together with adjustments to the battery export tax rebate policy, further lifted short-term battery foil demand. However, the conflict in the Middle East disrupted air-conditioner exports to the region, affecting air-conditioner foil production schedules to some extent and restraining any further increase in the operating rate. Demand for food packaging foil and pharmaceutical foil remained in the peak consumption season, and leading enterprises had relatively ample orders on hand. As peak-season demand continues to be released, support from battery foil and packaging foil orders is becoming more evident, and the operating rate of leading aluminum foil enterprises is expected to remain stable.

Secondary Aluminum: This week, the operating rate of leading secondary aluminum enterprises rebounded 0.8 percentage points MoM to 59.5%. Seasonal recovery in downstream consumption boosted enterprise operating rates, but the overall increase in operating activity remained mild. Market feedback showed that downstream die-casting enterprises were not highly motivated to purchase during the week, with limited willingness to rush to buy amid continuous price rise, and no clear increase in restocking volume even after prices fell. Most buyers still focused on digesting inventories or just-in-time procurement. Limited demand release constrained the pace of shipments from secondary aluminum plants, thereby capping room for further recovery in operating rates. In addition, environmental protection-related controls tightened again in some northern regions, also suppressing local enterprise production to a certain extent. Overall, the current rebound in operating rates was mainly driven by seasonal demand recovery, but amid insufficient order follow-through and pressure from environmental protection and the cost side, short-term operating rates are expected to continue posting only a mild rebound. Going forward, close attention should be paid to whether downstream consumption can effectively scale up and to changes in regional policies.

[Data Source Statement: Except for publicly available information, all other data is derived by SMM based on public information, market communication, and SMM's internal database models, and is for reference only and does not constitute decision-making advice.]